Published April 22, 2024

Cash basis and accrual basis accounting methods both have advantages and disadvantages. Discover more about these two accounting methods and find which one is better for your business.

An accounting method is based on rules that your business must follow when reporting revenues and expenses. Whether you’re using financial accounting, managerial accounting, or another type of accounting, the rules for accounting methods remain the same.

Cash basis and accrual basis are the two main accounting methods. Cash and accrual basis accounting are similar, but vary in how they report revenue and expenses. Whether you use cash basis or accrual basis accounting, you will need to follow the rules that govern the method chosen.

New business owners or those new to accounting can struggle deciding which method to use for their business.

To further complicate the situation, once you choose, and file taxes using your chosen method, you will need to request approval from the IRS to change the accounting method that your business uses.

What is cash basis accounting?

Cash basis accounting recognizes revenue when cash is received and when expenses are paid. If you invoice a client, but they don’t pay you until next month, you recognize that revenue when it’s received, not when it’s billed.

Cash basis accounting is a good option for sole proprietors and very small businesses without employees.

First, cash basis accounting is much easier than its accrual basis counterpart, partially because cash basis accounting eliminates the need to track accounts payable or accounts receivable.

And it eliminates the need to create journal entries. Cash basis accounting is reminiscent of checkbook accounting, with business owners starting with an amount of money and adding or subtracting any changes to that balance.

What is the accrual accounting method?

The accrual accounting method is more complex than cash basis accounting, making it a much better fit for businesses with an experienced bookkeeper on staff.

Accounting professionals such as CPAs also recommend accrual accounting, since it provides a much more accurate picture of the health of your business.

Using the scenario above, if you perform services for your client and bill them today, the revenue from that service is recognized today, not when the money is received.

That’s because unlike cash basis accounting, accrual accounting recognizes both revenue and expenses when earned, not when received or paid.

Cash basis vs. accrual basis: What's the difference?

The main difference between cash basis accounting and accrual basis accounting is when revenues and expenses are recognized. While this may not seem like a major difference, the example shows how different these two methods can be, and how they can affect your business.

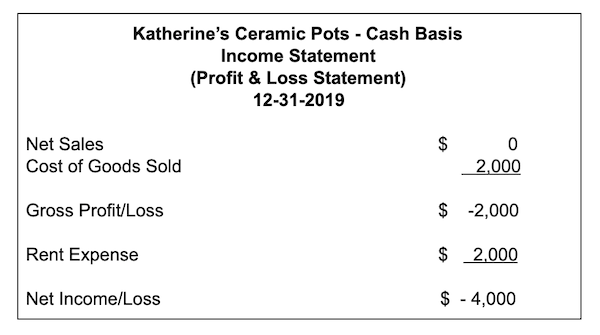

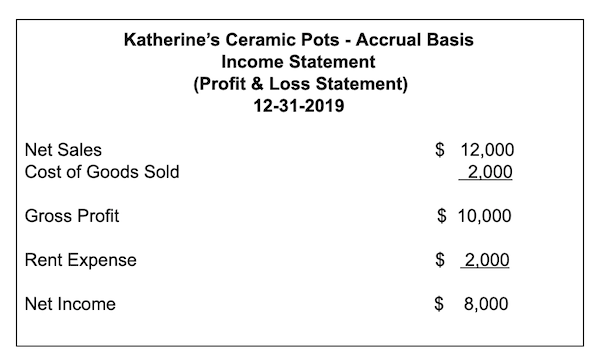

In December of 2019, you opened a cleaning service. You purchased $2,000 worth of cleaners and other cleaning tools. Your first month in business, you made $12,000 cleaning various offices.

However, your clients will not be paying you until January. Meanwhile, you also paid rent on your storefront for $2,000. Check out the two income (Profit & Loss) statements below to see how each accounting method affects your business.

Income Statement on cash basis for Katherine’s Ceramic Pots Image source: Author

If you look at the cash basis income statement, you’ll see that your business is showing a loss of $4,000, because you cannot recognize revenue until it is received.

So while you actually did not have a loss, your income statement shows that you did. You also had to recognize both the supplies expense and the rent expense in December because that’s when both were paid.

One plus for small businesses using the cash basis accounting method is that you will not need to pay taxes on any revenue until it’s received, which can help cash flow tremendously, particularly for businesses just starting out.

Income Statement on accrual basis for Katherine's Ceramic Pots Image source: Author

If you take a look at the accrual basis income statement, you’ll see that it more accurately reflects the activity that took place in the month of December. Even though you will not be paid for the office cleaning jobs you completed until January, you are still recognizing that you did perform those services.

Using accrual accounting provides a much more accurate summary of your business. The downside is that you will need to pay taxes on your net sales, prior to receiving a payment from your customers, which can be an issue for small businesses operating on limited cash flow.

How to choose the right option for your business

Your business size can be the determining factor in deciding which accounting method to use. Sole proprietors and freelancers almost always decide in favor of the cash basis because it’s simple and more accurately tracks cash flow.

Cash basis accounting can be particularly attractive to those just starting out or those with a limited accounting or bookkeeping background, as managing cash basis accounting is similar in scope to managing your checkbook.

If you’re not paying employees and don’t want to be tasked with tracking accounts payable and accounts receivable balances, the cash accounting method may be for you.

However, there are times, even for very small businesses, that accrual accounting is the better option. If you find your business growing, or you need to hire an employee or two, accrual accounting is a much better choice.

Using accrual accounting allows you to seek investors or apply for a bank loan, and it offers a much better option if you're in business to provide services.

Cash basis or accrual basis: which should you choose?

Keep in mind that the choice to use cash basis or accrual basis accounting will impact your business for the foreseeable future.

If you’re a small business owner, sole proprietor, or freelancer, cash basis accounting is probably your best option because it gives you the ability to better track cash flow, and you eliminate the need to track accounts payable or accounts receivable.

You also won’t have to worry about creating and posting journal entries, and you’ll only have to pay taxes on revenue that has already been received.

However, if you have plans to expand in the near future, want to bring investors into your business, or apply for bank financing, your best bet is to use the accrual accounting method.

It provides you and any outside parties with a much more accurate financial picture. Keep in mind that using the accrual method of accounting will require you to keep a closer eye on cash flow, which can be obscured when using accrual accounting.

Whether you’re using cash basis or accrual basis accounting, the best way to keep track of your revenues and expenses and eliminate the need to process closing entries manually is to use accounting software.

If you’re looking to make the move from spreadsheet accounting or are in the market for a new accounting software application, be sure to check out The Ascent’s accounting software reviews.

Our Small Business Expert

Mary Girsch-Bock studied accounting and business at UIC. After working as an accountant for many years in various industries, including healthcare and property management, she returned to her first love, writing. She specialized in accounting and business articles, with an emphasis on software reviews, which she wrote for more than 20 years. She continues to write for the first publication she ever wrote for, CPA Practice Advisor, while blogging for several software companies.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

The Motley Fool has a disclosure policy.