Published April 22, 2024

The cost principle states that any asset should be recorded at the purchase price. Learn why the cost principle is an important principle for your small business.

There are four basic financial reporting principles governed by generally accepted accounting principles (GAAP). These principles are designed to provide consistency and set standards throughout the financial reporting field. If you wish to be compliant with GAAP, the cost principle should be used.

The cost principle maintains that the cost of an asset must be recorded at historical cost, or its original cost and should not be recorded at fair market value. We’ll explain in greater detail just what the cost principle is and how it may impact your business.

Overview: What is the cost principle?

Even if you’re an accounting newbie, you know the importance of assets. Assets are anything of value that your business owns. Because they are so important to your business, it’s essential to record and report their value accurately and consistently, a relatively easy process if you’re using accounting software.

But whatever process you’re using to record your assets, the cost principle can help maintain consistent balance sheet reporting.

The cost principle, also known as the historical cost principle states that assets should be recorded at their original cost, rather than their current market value.

This is because, in many cases, the cost of an item is subjective and dependent on market conditions. For example, an asset you purchased a year ago may suddenly gain value for a variety of reasons. Maybe the manufacturer stopped making that particular item, or the item has become scarce.

Maybe it has become extraordinarily popular. Whatever the reason, the cost principle maintains that the asset value remains the same as its original, or purchase, cost regardless of later changes in market value.

The cost principle has little impact on current assets like your bank account; they are short-term assets with little opportunity to gain any value. However, assets such as equipment and machinery should be recorded at face value and remain on the balance sheet at their original cost.

Are there exceptions to the cost principle?

There are some exceptions to the cost principle, mainly regarding liquid assets such as debt or equity investments. Investments that will be converted to cash in the near future are shown on your balance sheet at their market value, rather than their historical cost.

The other exception is accounts receivable, which should be displayed on your balance sheet at their net realizable balance, which is the balance that you expect to receive when the accounts receivable balances are paid.

Examples of the cost principle

These examples may help you better understand the cost principle in action.

Cost principle: Example 1

Jim started his business in 2008, constructing a building to house his growing staff. The cost to construct the building was $300,000, but by 2020, the fair market value of the building had increased to $1.1 million. However, on Jim’s balance sheet, the cost of the building remains at $300,000.

Cost principle: Example 2

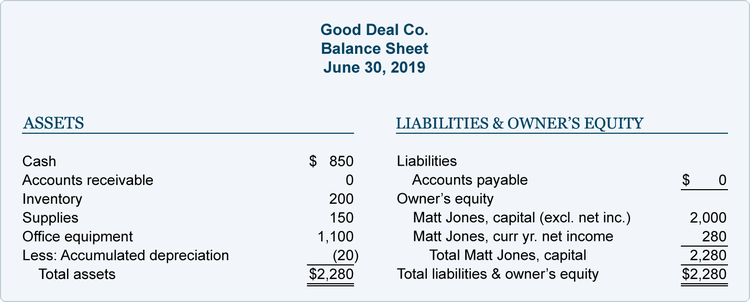

Laura purchased a piece of machinery for her small manufacturing plant in 2017 at a cost of $20,000. Today, Laura’s machinery is worth only $8,000, but it is still recorded on her balance sheet at the original cost, less the accumulated depreciation of $12,000 that has been recorded in the three years since its purchase.

The balance sheet displays the office equipment balance and the accumulated depreciation. Image source: Author

Source: AccountingCoach.com.

Cost principle: Example 3

Scott’s music production company purchases the copyright to a song from an up-and-coming artist. Scott should record the newly purchased asset at the cost he paid to purchase the copyright. Because copyright is an intangible asset, the copyright cost should be amortized, rather than depreciated.

Should you be using the cost principle?

If you currently use accrual accounting in your business and wish to be GAAP compliant, you should be using the cost principle. Since publicly owned companies are required to be GAAP compliant, they should be using the historical cost principle as well.

There are some benefits -- and a few drawbacks -- to using the cost principle, which we’ll examine next.

Benefit of using the cost principle

- Your balance sheet is consistent: Using historical cost principle ensures that your balance sheet is consistent from period to period. This is even more important when sharing that balance sheet with outside entities, such as investors and lenders.

- You can verify costs: One of the most important aspects of accounting is verification. For every transaction you make in your accounting software or your manual ledgers, there should be an originating document that verifies that entry. In other words, if there is ever a question about the assets on your books, you’ll have the original sales document with the cost of the asset available.

- There are no adjustments needed: As long as you consistently handle all your assets using the cost principle, costs will not change, always ensuring that your financial statements are accurate and not based on fluctuating fair values.

It’s important to understand the difference between the historical cost and fair value of your assets and when to use which figure. Image source: Author

Source: WallStreeMojo.com.

Drawbacks of using the cost principle

While it’s clear that using the cost principle has its advantages, there are also a few downsides as well. For instance, if your business has valuable logos or brands, they would not be reported on your balance sheet.

There is an exception for intangible assets purchased from another business. Issues can also arise when selling an asset, since it would likely be sold at fair market value, not historical cost.

Finally, the value of your company may be seriously undervalued based on the historical cost of assets, which can directly affect your credit rating, your ability to obtain a loan, or even your ability to sell the business.

FAQs

-

Let’s say you decide to purchase a computer monitor. You have a particular brand and size in mind, so you visit various stores looking for the monitor. During this process, you realize that the exact same monitor varies in pricing from store to store. So how do you determine its fair market value?

What the historical cost principle does is ensure that you record the asset you’ve purchased at its original cost, rather than what the market value. Fair market value will always change, the original cost of the asset will not.

-

Yes. Using the cost principle will record the asset cost at its original cost, but you will still have to depreciate the asset, as in most cases it will continue to lose value, or depreciate.

-

Any highly liquid assets you purchase should be recorded at fair market value rather than historical cost. Financial investments that your business makes should also be recorded at fair market value and adjusted after each accounting period to reflect the most current value.

The cost principle offers consistency

When it comes to accounting, small business owners, who often have no background in accounting, prefer simplicity and consistency. Using the cost principle offers both. Rather than recording the value of an asset based on fair market value, which can fluctuate widely, your assets will all be recorded at their actual cost.

This ensures that the asset value reported on your balance sheet is consistent from period to period, that there is a means to verify the cost of the asset, and that asset value is not manipulated.

While there are drawbacks to using the cost principle, in most cases those drawbacks are reserved for larger companies with multiple investments or volatile, short-term securities. If you're looking to make the accounting process easier for your small business, you can start by using historical cost principle accounting.

Our Small Business Expert

Mary Girsch-Bock studied accounting and business at UIC. After working as an accountant for many years in various industries, including healthcare and property management, she returned to her first love, writing. She specialized in accounting and business articles, with an emphasis on software reviews, which she wrote for more than 20 years. She continues to write for the first publication she ever wrote for, CPA Practice Advisor, while blogging for several software companies.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

The Motley Fool has a disclosure policy.