5 Steps for Filing S Corporation Taxes

Choosing a business structure requires a calculus that weighs tax and legal benefits with startup costs and time. It’s one of the most consequential decisions you’ll make when you first start your small business.

Many small business owners hesitate to elect S corporation taxation because it requires more upfront time to get going. But don’t demur S corp tax status: There are some great tax benefits you could be missing.

How do S corporation taxes work?

Don’t let the word “corporation” confuse you. S corporations don’t pay corporate income tax. Instead, S corporations enjoy pass-through taxation in which the company’s owners pay taxes on their portion of the company’s earnings based on their individual tax rates.

To get S corporation tax treatment, register your business as a C corporation or limited liability company (LLC). From there, file IRS Form 2553 to elect S corporation taxation.

Not all C corporations and LLCs can take advantage of the S corporation tax status. Check out all the eligibility requirements in The Ascent’s guide to S corporations.

3 tax benefits of filing as an S corporation

S corporation status offers a plethora of advantages over other business types. Chief among the perks are double taxation avoidance, shareholder-employee status, and limited liability.

1. No double taxation

C corporations, known as traditional corporations, pay income tax at the entity and shareholder levels. One of the hallmarks of S corporations is taxation only at the shareholder level.

Say a C corporation with one shareholder has taxable income of $100,000.

- Entity-level tax: The entity pays a 21% corporate income tax on a net income of $79,000 ($100,000 taxable income = $21,000 corporate income tax).

- Shareholder-level tax: The C corporation declares all $79,000 in cash dividends to its 100% shareholder. The shareholder pays income tax on the $79,000 dividend when he or she files personal tax Form 1040.

You can see from this example that cash dividends, called shareholder distributions, are essentially taxed twice. As the owner of a C corp, any income that makes it to your personal bank account gets taxed twice.

S corporations and other pass-through entities cut out the entity-level tax, passing all income tax liability to the owners, called shareholders. If an S corp has $100,000 in taxable income, all $100,000 gets taxed on the shareholders’ personal income tax returns.

It’s important to note that S corps don’t always triumph in the S corp vs. C corp battle. C corporation owners who prefer to reinvest earnings into the business can essentially eliminate the second layer of tax.

2. Shareholder-employee status

Many LLC owners, called members, elect S corp status so they can be classified as employees of their organization. Unlike other pass-through entity types, S corporation shareholders who actively participate in management can also be considered employees.

To the untrained ear, employee classification might seem insignificant. Others hear “payroll tax savings” ringing in their heads.

Pass-through entity owners are usually considered self-employed, meaning they pay the employee and employer portions of Federal Insurance Contributions Act (FICA) taxes, totaling 15.3% of gross wages.

Owners usually pay both halves of FICA on the entire portion of pass-through earnings, but that's not the case for S corporation shareholder-employees.

S corporation shareholder-employees must collect a salary, which is subject to FICA taxes. When there’s extra income to distribute, shareholder-employees can receive dividends, which aren’t subject to FICA taxes. Federal and state income taxes still apply on all earnings, but shareholder-employees stand to avoid 15.3% in taxes on dividends received.

For example, a shareholder-employee’s compensation package might include a $60,000 salary and another $15,000 in cash dividends. The $60,000 is subject to FICA, but the $15,000 isn’t.

The IRS pays special attention to S corporation shareholder-employees to deter abuse of that classification. You must pay yourself a reasonable salary before taking tax-advantaged dividends.

3. Limited liability

S corporations have two identities. They’re S corporations for tax purposes, but they started as either C corporations or LLCs, two structures that afford limited liability to owners.

Unless you personally guarantee a business debt, your personal liability generally doesn’t extend past your investment in the company. Of course, there are cases where a business transaction “pierces the corporate veil,” opening you up to more liability.

How to file taxes as an S corporation

Pass-through taxation doesn’t mean your business doesn’t pay taxes. Follow these five steps to filing taxes as an S corporation.

1. Prepare your financial statements

One of the first things your tax professional will ask for are financial statements. Even if you’re using tax software to do your business taxes, you’ll want completed financial statements before you get started.

Your profit and loss statement and balance sheet contain most of the information you need to complete your tax filings. You’ll want to keep your accounting software open during the process so you can examine your expenses more closely.

2. Issue Forms W-2

Before you file your business tax return, you should complete and issue Forms W-2 for all employees. Form W-2 reports employee compensation and how much the employer withheld in FICA taxes during the year.

With cover sheet Form W-3, the forms get sent to each employee, the Social Security Administration (SSA), and state and local governments.

Shareholders who participate in management will receive a Form W-2 because their compensation package must include a salary. Box one on Form W-2 should include any health insurance premiums the S corp paid on behalf of a shareholder.

W-2 compensation, even for shareholder-employees, is a business deduction. I’ll point out where to deduct shareholder salaries in the next step.

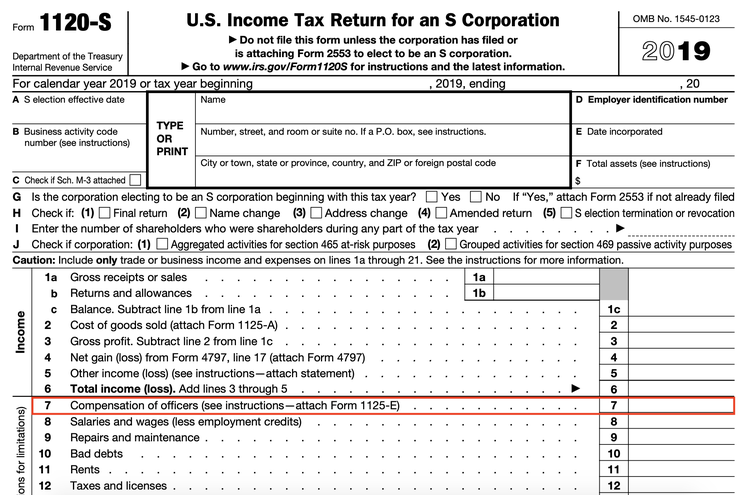

3. Prepare information return Form 1120-S

Although S corporations don’t pay entity-level tax, they still file business tax returns, called information returns.

S corporations use Form 1120-S to report income, losses, credits, and deductions. It loosely resembles the C corporation return, Form 1120, so make sure you download the correct one.

Here is where you find one of the disadvantages of electing S corporation status: Form 1120-S has many built-in schedules and can get confusing fast. Keep a tax professional on metaphorical speed dial while you complete the S corp tax return.

Shareholder salaries get reported on line seven of Form 1120-S. Image source: Author

Remember how S corp shareholders can be employees? Don’t forget to deduct their W-2 wages on Form 1120-S.

Shareholders’ W-2 earnings go on line seven, and other employees’ earnings go on line eight.

4. Distribute Schedules K-1

S corporations must fill out Schedule K and Schedule K-1. Yes, they’re different. You start with Schedule K, a built-in section of Form 1120-S, to summarize the S corporation’s income, deductions, and credits to be passed on to shareholders.

The S corp’s total earnings get divided up on Schedule K-1. S corporations furnish a Schedule K-1 to shareholders, telling them the portion of S corp earnings for which they’re responsible to pay taxes on their personal returns.

Most S corps allocate shareholder earnings by ownership interest percentage, but they can come to a different agreement.

5. File Form 1040

As an S corp shareholder, you pay income tax on two types of income -- your salary and your portion of S corp earnings. You’ll often hear these referred to as W-2 and K-1 income, respectively. Both get reported on your personal tax return.

Your W-2 income goes on line one of Form 1040. Then report your portion of S corp earnings on part two of Form 1040 Schedule E, a catch-all form for supplemental income, and Form 1040 Schedule 1, a summary of Schedule E and other adjustments to income.

S corp shareholders should not go it alone when filing their personal taxes. I always make sure I’m not alone when I dare to peek at Schedule E in case I faint. Get a tax preparer or tax software to walk you through the filing process.

S corp status can save some serious silver

The S corporation tax structure has a lot to offer small businesses with active owners. Before you file your small business taxes next year, consider electing S corp status.

Alert: our top-rated cash back card now has 0% intro APR until 2025

This credit card is not just good – it’s so exceptional that our experts use it personally. It features a lengthy 0% intro APR period, a cash back rate of up to 5%, and all somehow for no annual fee! Click here to read our full review for free and apply in just 2 minutes.

Our Research Expert

Ryan Lasker is an SMB accounting expert writing for The Ascent and The Motley Fool.

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

Related Articles

View All ArticlesBy: Ben Gran | Published on Jan. 26, 2024

By: Steven Porrello | Published on Feb. 28, 2024

By: Ben Gran | Published on Feb. 27, 2024

By: Maurie Backman | Published on Feb. 27, 2024

By: Chris Neiger | Published on March 2, 2024