Published April 22, 2024

The specific identification method of inventory control is useful for businesses with unique or high-priced products. Here's how to implement this method in your business.

We’ve covered several inventory management types, including, LIFO vs. FIFO and weighted average cost. We’ve also considered whether to use a perpetual or periodic inventory system.

Each of those methods are commonly used and easy to manage. The method that we’ll talk about today is not so easy to manage, though. It requires the specific tracking of every single unit purchased and sold.

Read on to learn why you may want to use this method when other methods, such as the first in, first out method, are much easier to implement.

Overview: What is the specific identification method?

The specific identification method is a way to calculate cost of goods sold and ending inventory by tracking every single unit of inventory and adjusting the balances when inventory is sold and when it is purchased.

This method is typically used by companies that sell high-ticket products or that want to very closely control inventory and track sales trends.

3 examples using the specific identification method

Let’s take a look at a few examples of the specific identification method and compare its results to those we’d achieve by using other methods.

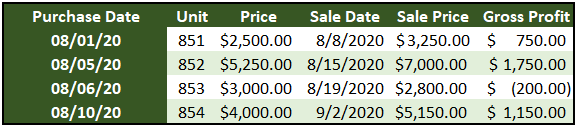

1. Jose’s Coches

Jose’s Coches buys totaled cars at auction and then resells them after making repairs. Take a look at Jose’s inventory turn and how cost of goods sold and gross profit are calculated.

Cost of goods sold is determined at the time of purchase using this method. Image source: Author

For Jose’s business, one of the more common methods of inventory management, such as weighted average cost, wouldn’t be applicable. The weighted average cost formula would use units 851, 852, and 853 to come up with an average cost for the sale of 851.

Because each item is unique and its cost has nothing to do with the others, specific identification should be used to calculate the cost and gross profit.

2. Iliana’s Island Washes

Next, let’s take a look at an example where using a common method would be feasible.

For Iliana’s car wash business, the importance of inventory management comes from tracking sales trends. She sells several different types of air fresheners that all cost about the same. Here is a typical day of sales and the purchases that built her inventory. Each unit sells for $5.

Brisket is the most popular selling air freshener right now. Image source: Author

Iliana’s air freshener sales happen in bunches. Once the cream of the crop, fresh-cut grass sold just three units on our example day. Brisket, on the other hand, is driving sales at the moment.

By keeping close track of which units are selling the most each day, Iliana is able to make smart orders and accurately show the cost of each scent. The first table in the graphic shows purchases made in the week leading up to our example day and the second table shows units sold on that day.

If she had used FIFO inventory to calculate COGS and gross profit for this day of sales, she would calculate the total units sold on the day, which was 66. To get to 66 units from the purchases record, she would take the 20 vanilla and linen units and 26 of the brisket.

This is a cost of goods sold of $83.90. With sales of $330, gross profit comes in at $246.10, just a bit above the total of $243.60 using specific identification.

3. Stock sales

The most common use of specific identification is probably not applicable to your business. When trading stocks, you can use this method for tax reporting. For example, let’s say you purchased shares of a stock at four different times over a number of years.

When you decide to sell some, you could choose whichever purchase had the highest price to lower your taxes now. Of course, you will eventually have to sell some shares using the lowest price, but you can do that at a time that works best for your tax and other financial goals.

3 benefits of using the specific identification method

Here are three benefits to using the specific identification method.

1. There’s no guesswork

The key benefit is that your cost of goods sold and ending inventory numbers will always be exactly correct, as long as you are confirming with an ending inventory count to catch theft or spoilage.

You don’t have to worry about matching the number of units from this sale to different purchases because each unit has a cost assigned to it.

2. You know exactly what’s selling

If you sell different versions of similar items, like the car wash business above, your inventory management software will give you up-to-date data on which items are selling the most. That will enable you to purchase new inventory that meets your current sales trends.

3. You can track heterogeneous inventory

The average cost and LIFO methods were designed for tracking homogenous goods (think 20,000 units of the same white shirt, or 150 rolls of the same size paper). If you sell heterogeneous items that can’t be counted together, specific identification is probably the best way to manage inventory.

3 disadvantages of using the specific identification method

Here are three disadvantages to using specific identification.

1. It can take a lot of work

You will need to institute some way to track each unit. If your inventory is unique enough, that could be as easy as checking a spreadsheet. If it isn’t unique, you may need to track it with barcodes or RFID chips.

2. It’s probably not necessary

Unless you only sell a few items a year and each one has a substantially different cost, you will likely be able to very closely approximate the specific identification numbers with one of the more commonly used methods.

3. You can manipulate net income

If you’re able to choose exactly which unit to sell, and thus use in the COGS calculation for each sale, it may become tempting to purposely choose the most expensive unit if you want to show lower net income (for taxes), or the least expensive unit if you want to show higher income (for the bank).

Sticking to a more commonly used method takes this temptation away.

Should your small business use the specific identification method?

The answer is likely no. However, specific identification is a great tool in certain limited situations. If it suits your business, you probably realized that the minute you started reading this article.

If you run an HVAC servicing business and sell used appliances every once in a while, you should probably use specific identification. If you make custom motorcycles that are unique, you should probably use specific identification. But if you run a convenience store, use FIFO or the average cost method.

Do know much about inventory

Don’t worry if you end up using a periodic inventory system and the gross profit method to complete your books every quarter. If that’s the right way to go for your business, it will get the job done.

If you need to use the specific identification method, make sure you’re tracking correctly and do an inventory count once a month to verify your numbers.

Our Small Business Expert

Mike Price has worked with small businesses in banking and accounting capacities for the past six years. He specializes in bookkeeping, projected financials and debt restructuring.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

The Motley Fool has a disclosure policy.