11 Common Types of Liabilities

Like assets, liabilities are part of doing business. While you probably know that liabilities represent debts that your business owes, you may not know that there are different types of liabilities. Take a few minutes and learn about the different types of liabilities and how they can affect your business.

Overview: What are liabilities?

As a small business owner, you need to properly account for assets and liabilities. If you recall, assets are anything that your business owns, while liabilities are anything that your company owes. Your accounts payable balance, taxes, mortgages, and business loans are all examples of things you owe, or liabilities.

The best way to track both assets and liabilities is by using accounting software, which will help categorize liabilities properly. However, even if you’re using a manual accounting system, you still need to record liabilities properly.

Types of liabilities on a balance sheet

There are two main categories of balance sheet liabilities: current, or short-term, liabilities and long-term liabilities.

- Short-term liabilities are any debts that will be paid within a year. Your utility bill would be considered a short-term liability.

- Long-term liabilities are debts that will not be paid within a year’s time. These can include notes payable and mortgages, although the portion that is due within the year should be classified as a short-term liability.

Though not used very often, there is a third category of liabilities that may be added to your balance sheet. Called contingent liabilities, this category is used to account for potential liabilities, such as lawsuits or equipment and product warranties.

Contingent liabilities are only recorded on your balance sheet if they are likely to occur.

Both short-term and long-term liabilities include several types of liabilities which you will need to become familiar with in order to record them properly.

Current liabilities

Type 1: Accounts payable

Accounts payable liability is probably the liability with which you’re most familiar. For smaller businesses, accounts payable may be the only liability displayed on the balance sheet.

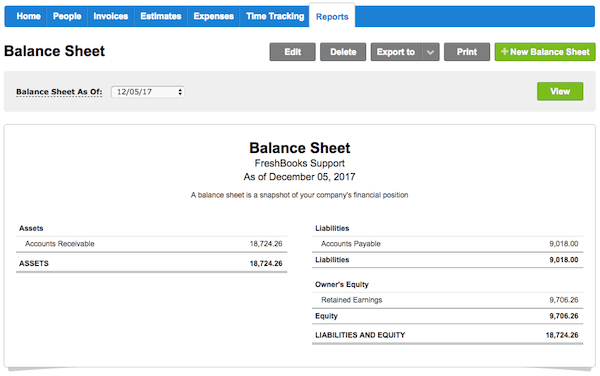

A simple balance sheet in FreshBooks displays a single liability: accounts payable. Image source: Author

Accounts payable represents money owed to vendors, utilities, and suppliers of goods or services that have been purchased on credit. Most accounts payable items need to be paid within 30 days, although in some cases it may be as little as 10 days, depending on the accounting terms offered by the vendor or supplier.

Type 2: Principle & interest payable

If you have a loan or mortgage, or any long-term liability that you’re making monthly payments on, you’ll likely owe monthly principal and interest for the current year as well. The balance of the principal or interest owed on the loan would be considered a long-term liability.

Type 3: Short-term loans

A short-term loan is a loan that is due and payable within a 12-month timeframe. Any loans that are due and payable longer than one year would be considered a long-term liability.

Type 4: Taxes payable

Both income taxes and sales taxes need to be properly accounted for. Depending on your payment schedule and your tax jurisdiction, taxes may need to be paid monthly, quarterly, or annually, but in all cases, they are likely due and payable within a year’s time.

Type 5: Accrued expenses

When using accrual accounting, you’ll likely run into times when you need to record accrued expenses. Accrued expenses are expenses that you’ve already incurred and need to account for in the current month, though they won’t be paid until the following month.

Accrued expenses typically include wages and salaries, rental payments, and utilities.

Type 6. Unearned revenue

Unearned revenue is money that has been received by a customer in advance of goods and services delivered.

When your customer pays you three months in advance, that money is considered unearned revenue and is classified as a current liability, where it will remain until the goods and/or services have been delivered to the customer.

Long-term liabilities

Type 1: Notes payable

Notes payable is similar to accounts payable; the difference is the presence of a written promise to pay. A formal loan agreement that has payment terms that extend beyond a year are considered notes payable.

Type 2: Mortgage payable

Any mortgage payable is recorded as a long-term liability, though the principal and interest due within the year is considered a current liability and is recorded as such.

Type 3: Bonds payable

Bonds are typically issued by public utilities, hospitals, and local governments.

The entities issuing the bonds formally agree to pay interest on any bonds issued, with interest typically paid every six months or annually, while also agreeing to pay the principal amount by a date specified in the formal agreement. Bonds payable are always considered long-term debt.

Type 4: Deferred tax liabilities

Deferred tax liability refers to any taxes that need to be paid by your business, but are not due within the next 12 months. If you know that you’ll be paying the tax within 12 months, it should be recorded as a current liability.

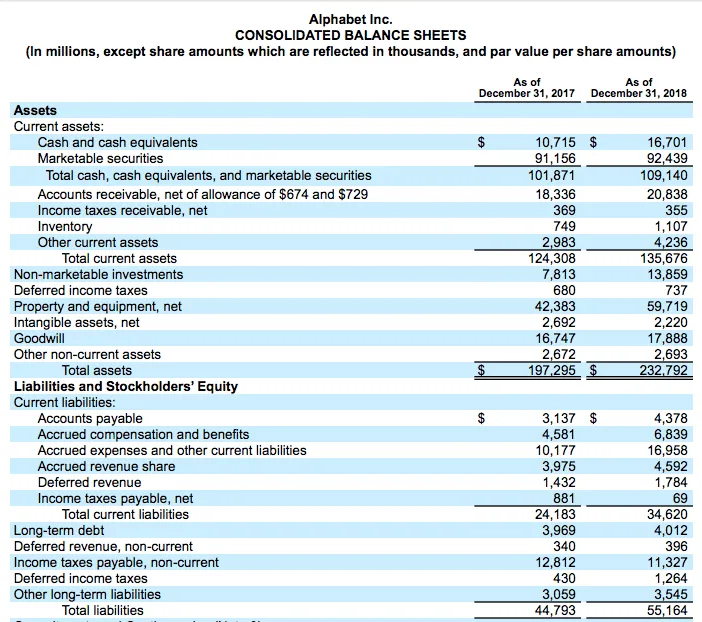

The consolidated balance sheet displays both short-term and long-term liabilities. Image source: Author

Type 5: Capital leases

Capital leases are a bit tricky. A capital lease refers to the leasing of equipment rather than purchasing the equipment for cash.

The amount of the capital lease is included on your balance sheet as a long-term asset, while that same amount will also need to be recorded as a long-term liability, reflecting the amount that is owed on the lease.

FAQs

-

While both reflect money owed to an outside source, current liabilities represent money owed that is due within the next 12 months. Long-term liabilities reflect money owed that is not due and payable within a 12-month time frame.

That’s why accounts payable is considered a current liability, while your mortgage would be considered a long-term liability.

-

If you’re a very small business, chances are that the only liability that appears on your balance sheet is your accounts payable balance.

While you certainly can just record these as a liability for your own reporting purposes, if you’re sharing your financial statements with outside agencies, investors, lenders, or other financial institutions, you will need to separate current and long-term liabilities properly.

-

It’s actually both. For example, if you have a 30-year mortgage on your office building, the amount due within the next 12 months should be recorded as a current liability, while the remainder of the balance owed should be recorded as a long-term liability.

Managing liabilities is part of being a business owner

If you own a business, you’re going to have liabilities. Even if it’s just the electric bill and rent for your office, they still need to be tracked and recorded.

As your business grows and you take on more debt, it becomes even more important to understand the difference between current and long-term liabilities in order to ensure that they’re recorded properly.

Alert: our top-rated cash back card now has 0% intro APR until 2025

This credit card is not just good – it’s so exceptional that our experts use it personally. It features a lengthy 0% intro APR period, a cash back rate of up to 5%, and all somehow for no annual fee! Click here to read our full review for free and apply in just 2 minutes.

Our Research Expert

Mary Girsch-Bock is the expert on accounting software and payroll software for The Ascent. She previously worked as an accountant.

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

Related Articles

View All ArticlesBy: Ben Gran | Published on Jan. 26, 2024

By: Steven Porrello | Published on Feb. 28, 2024

By: Ben Gran | Published on Feb. 27, 2024

By: Maurie Backman | Published on Feb. 27, 2024

By: Chris Neiger | Published on March 2, 2024