Published April 22, 2024

Unit contribution margin tells you about the profitability of a product. It’s helpful when pricing products and determining manufacturing volume.

Doctor Strange would be a great business owner. Before making a decision, he could see its implications for profits. I want to be his business partner. Absent a clairvoyant superpower, the rest of us rely on financial data to make business decisions. (It’s not as lame as I’m making it seem, I promise.)

Unit contribution margin is just one of many accounting analytics that helps manufacturing business owners make decisions.

Overview: What is unit contribution margin?

Businesses use unit contribution margin to measure the profitability of manufactured goods and to inform production volume decisions.

Before we look at unit contribution margin, let’s discuss regular old contribution margin.

Manufactured inventory product costs have two parts: fixed and variable. Fixed costs -- factory rent, insurance, property tax -- don’t change with your production volume. If your business makes tennis balls, your factory landlord doesn’t charge you different rates depending on whether you make five or 5 million tennis balls.

Variable costs -- direct materials, factory worker wages, shipping -- increase with your production, so the more tennis balls, the more variable costs, but the same fixed costs.

Contribution margin refers to the sales revenue left over when you subtract the variable costs of manufacturing inventory. In other words, contribution margin is manufacturing profit before taking into account fixed costs.

As the name suggests, unit contribution margin breaks down your contribution margin to a per-unit level, providing new insight. The formula explains it best:

Unit contribution margin = unit selling price – unit variable cost

You can express contribution margin or unit contribution margin as a ratio by dividing contribution margin by selling price.

You might ask: Why ignore fixed costs? Since fixed costs do not change based on the number of units your business manufactures, they shouldn’t influence many manufacturing decisions.

Manufacturing businesses look at their unit contribution margin to assess which products are most profitable and whether to take on special orders from customers. It also informs pricing decisions.

How to calculate the unit contribution margin

Imagine your company makes and sells stuffed animals. Below are the selling prices and variable costs associated with your top sellers last month.

Calculate the unit contribution for each product line to find the margin. Image source: Author

To find the unit contribution margin, subtract each stuffed animal’s selling price from its variable costs. Your unit contribution margins are $2 for the giraffe, $2 for the llama, and $3.75 for the dolphin.

Calculating the unit contribution margin isn’t the hard part. It’s what you do with the information that makes this metric so valuable.

Examples of the unit contribution margin

To make informed business decisions, you need financial data, smart advisers, and a gut feeling. Unit contribution margin should be one of the many financial data points you bring into the decision room.

Consider unit contribution margin in the following business discussions:

- Determining the break-even point

- Pricing your products

- Accepting special orders

- Dropping or adding product lines

- Creating your production budget

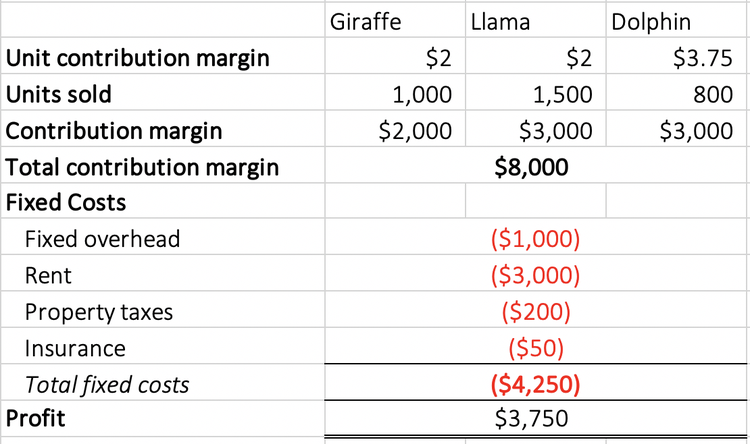

Let’s test-drive some of these scenarios with the stuffed animal manufacturing business. No business decisions should be made solely on one number, so let’s bring in more context on how the business did last month.

Bring in as much data as you can before making manufacturing decisions. Image source: Author

Here are the key takeaways:

- The dolphin has the highest unit contribution margin at $3.75.

- Your best seller was the llama at 1,500 units.

- Though the dolphin sold significantly fewer units, the llama and the dolphin have the same contribution margin at $3,000.

- Profit, also called product margin, is $3,750.

Scenario 1. Your business is considering dropping one of its stuffed animal lines to make room for a new line of unicorn stuffed animals.

At first glance, you might consider dropping the dolphin line, which sold the fewest units last month. Think twice, though, since the dolphin has the highest unit contribution margin.

Instead, it makes the most sense to drop the giraffe line. While it sells better than the dolphin, it brings in less profit due to a low unit contribution margin.

Scenario 2. A national toy company wants to pay you $12 per stuffed animal you manufacture to be exclusively sold in its stores. It will cost you $5 for materials, $1 for labor, and $3.50 for variable overhead, bringing your variable costs to $9.50. You need to decide whether to accept the special order.

Your unit contribution margin is $2.50 ($12 selling price - $9.50 variable costs), which is higher than the $2 unit contribution margin on your giraffe and llama. If your business has excess capacity -- extra space in your factory to produce a new stuffed animal -- then you should accept this order.

If you don’t have excess capacity, that’s when you need to bring fixed costs back into the discussion. If you need to rent more space to manufacture the special order, your profit starts to decline, and it becomes a less lucrative venture.

FAQs

-

Many businesses tinker with unit contribution margin to price their manufactured goods. Start with a goal unit contribution margin, calculate your variable costs, and back into your selling price from there.

The formula becomes:

Selling price = goal unit contribution margin + variable costs

Say you’d like to earn $100 on every piece of artwork you sell. Your variable costs -- paint, brushes, and canvases -- total $40. Your selling price should be $140 ($100 goal unit contribution margin + $40 variable costs).

-

When your raw materials cost changes frequently, so will your unit contribution margin. Companies with volatile variable costs need to keep an eye on their unit contribution margin and be ready to act.

For example, volatile dairy and meat prices can cause restaurants’ unit contribution margins to plunge to near-zero or negative levels. Fixed costs drag losses even lower.

Every time there’s a significant change in your variable costs, recalculate your unit contribution margin. From there, decide if you need to adjust your selling price or find new ways to reduce variable costs.

-

When you have a positive unit contribution margin but have suffered a net operating loss (NOL), your fixed costs are most to blame. However, reducing your variable costs can reverse your misfortune.

Businesses with a net operating loss should seek opportunities to increase sales revenue and trim all expenses, not just manufacturing costs.

The first place you should go is your accounting software to see where you can prune expenses. In years of NOL, you can take a net operating loss deduction on your business taxes.

-

Accounting ratios don’t offer any benefit unless they’re compared to other metrics. Look at both contribution margin and unit contribution margin before making manufacturing decisions. (What a cop-out answer!)

Going back to the stuffed animal business, the llama had a lower unit contribution margin than the dolphin, but they had the same contribution margin. Since the llama sold more units, the dolphin and llama are equally profitable to your business.

Let data lead the way

It’s a data-driven world, and you can make data tell any story you’d like. There are analytics you’ll grow to rely on before making business decisions. Unit contribution margin should be just one of many accounting formulas and ratios you look at before you arrive at the solution to a problem.

Our Small Business Expert

Ryan Lasker is an accounting writer with a penchant for breaking down complex topics and has work published in USA TODAY. He is a Certified Public Accountant (CPA) licensed in the District of Columbia, holds a Master of Accountancy, and specializes in small-business financial planning.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

The Motley Fool has a disclosure policy.