When oil prices started to tumble in mid-2014 any company affiliated with the industry got hit...hard. Oil prices have started to recover, but Royal Dutch Shell Plc (RDS.B) and Helmerich & Payne, Inc. (HP -0.12%) still sport high yields and depressed prices. There are reasons for this state of affairs, but the outlook for each is starting to look brighter. Now is the time to do a deep dive.

The big bet

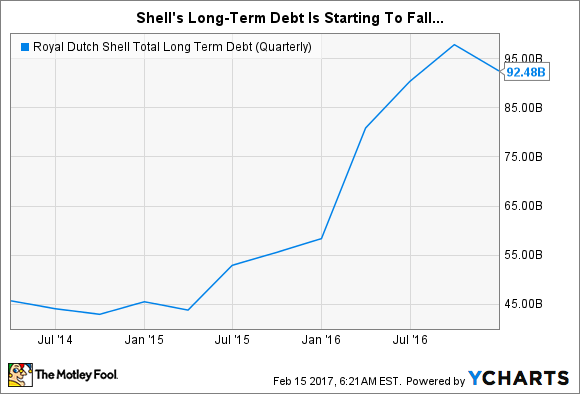

The problem Royal Dutch Shell faces today is debt. More specifically, it's got a lot of it. So much that investors are worried it won't be able to sustain its dividend and capital spending plans. Which is why it yields around 6.6% today. For reference, ExxonMobil (XOM -2.78%) yields around 3.6%. Shell is already offering shareholders a scrip dividend, which pays them in shares instead of stock so it can preserve cash. And it hasn't upped the dividend since the start of 2014.

Image source: Royal Dutch Shell Plc.

Lots of debt, weak earnings, no dividend hikes, scrip dividend...those are worrying signs. However, you have to step back and ask why. The easy answer is that oil prices have fallen from over $100 per barrel, putting pressure on the top and bottom lines. That's one piece of the puzzle, but the company's debt overhang is also related to its acquisition of BG Group, a gas focused energy company, during the downturn. That $50 billion deal pushed debt up to around 30% of the capital structure at the end of 2016, roughly 50% higher than it was the year before.

Here's the thing, Shell is well aware that it needs to reduce debt, and now that oil prices have moved off their lows, it's starting to sell non-core assets. The main goal of this effort is to solve the debt issue. Every asset sale makes the dividend that much more secure. However, the sales are also repositioning the company's portfolio with a heavier tilt toward natural gas. It's a fuel that many expect to be a key bridge between a renewable future and the carbon-heavy world of today.

RDS.B Total Long Term Debt (Quarterly) data by YCharts.

So, while Shell is out of favor today, it's starting to fix its debt problem and is positioning itself for what it sees as the energy sweet spot of the future. That's an out-of-favor stock you might want to put on your buy list.

Steady as she goes

Helmerich & Payne hails from the oil and gas drilling services side of the energy business. It's a highly cyclical industry, and the downturn hurt a lot. To give you an idea of just how bad, at the end of 2014, roughly 90% of Helmerich & Payne's oil rigs were working. At the end of fiscal 2016, only 25% were being used. It's little wonder that investors are leery of the stock, leaving it with an around 4% yield. Competitor Nabors Industries (NBR 1.26%), for reference, has a yield of 1.5%.

But Helmerich & Payne is used these ups and downs. It maintains a low level of debt (less than 10% of the capital structure), has a long-term focus on owning and operating industry-leading drill rigs, and has been protecting cash flow -- the real lifeblood of any business. Cash flow deserves a deeper dive because it's important to the safety of the dividend.

Helmerich & Payne builds big and expensive drill rigs. That leaves it with significant depreciation expenses, a non-cash charge that lowers GAAP earnings but has no impact on cash flow. When demand for rigs is high, Helmerich's rig building activity offsets the cash benefits of depreciation. However, in downturns, it generally stops building, which lets the depreciation benefit fall right into the company's bank account. In other words, the risk of a dividend cut at Helmerich & Payne right now is low. In fact, it upped the dividend in 2016 for the 44th consecutive year.

HP Total Depreciation and Amortization (TTM) data by YCharts.

However, the other piece of the puzzle, here, is that oil prices have improved enough that drilling activity has started to pick up again. At the end of the first quarter Helmerich & Payne's fleet utilization was up to 31%. With industry-leading technology, Helmerich & Payne's rigs are likely to get called back into action pretty quickly. If this is the start of the next upturn, you'll want to do a deep dive now before it's too late.

Ready to rebound

The stories behind Shell and Helmerich & Payne are very different. Shell made an aggressive and expensive bet during the downturn, and it's just now starting to work its way out from under the debt it took on. Helmerich & Payne, meanwhile, is running its playbook the same way it always has. But because the industry in which it operates is highly cyclical, investors are taking a show-me attitude. That's fair, but early indications are that Helmerich's business is picking up, along with oil prices. In both of these cases, though, the big story is the same: They are hated dividend stocks you might just want to buy now before everyone else figures out the opportunities that lie ahead.