Investors in Coach (TPR 1.68%) have been going through a lot of pain during the last several years. Shares of the handbags and accessories retailer made historical highs around $78 per share in March of 2012, and now they're trading in the neighborhood of $30 per unit.

Coach is a business in transition, and the company will report earnings for the first quarter of fiscal year 2016 on Tuesday, October 27, before official market hours. Will the coming earnings release from Coach provide reasons for hope, or will the stock continue languishing due to disappointing financial performance?

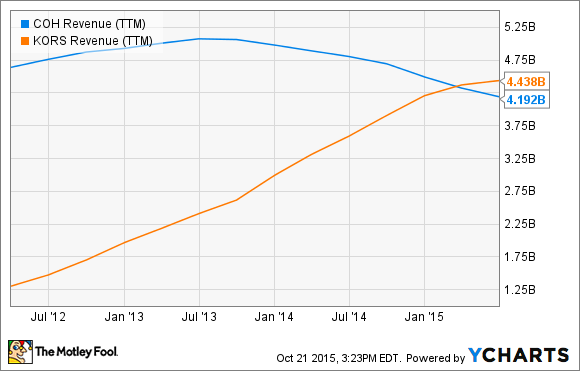

The problem

Coach used to be one of the hottest names in the affordable luxury handbags and accessories business, but management made a series of mistakes by expanding the company's presence too much, and making excessive use of discounts and pricing promotions to move inventory from the shelves. This eroded Coach's pricing power and brand differentiation over time, which ultimately ended up hurting sales and profits.

Making things worse, competitors such as Michael Kors (CPRI 2.10%) and Kate Spade (KATE) are doing much better than Coach, and stealing market share away from the company. The fashion industry is notoriously fickle and savagely competitive, and companies need to stay on the right side of consumer trends if they are going to protect their businesses from the competition. Nowadays, both Michael Kors and Kate Spade are much more in fashion than Coach.

Michael Kors was materially smaller than Coach a couple of years ago. However, things change rapidly in the fashion business, and Michael Kors has been firing on all cylinders, while Coach has been stagnant, and even declining. Not only is Michael Kors now bigger than Coach in terms of revenue, but everything indicates that there's no reversal in sight in the competitive dynamics between the two companies.

Coach suffered a 12% decline in revenue during the June quarter, with total sales coming in at $929 million. Michael Kors, on the other hand, announced a 7.3% increase in revenue during the quarter ending in June, reaching $986 million. On a constant-currency basis, Michael Kors did considerably better: global revenue jumped 13.4% versus the same quarter in the prior year.

COH Revenue (TTM) data by YCharts.

Kate Spade is much smaller than both Coach and Michael Kors, but the brand is truly on fire. Net sales, excluding wind-down operations, were $273 million during the quarter ending on July 4, an increase of 20.1% versus the same period in 2014.

Key areas to watch

During the last year, Coach has completely re-platformed its offering with the introduction of its new collection from Creative Director Stuart Vevers across different geographies, channels, and categories. This means that fiscal 2016 will be a crucial year for the company, as Coach will need to prove to both customers and investors that it can become a trendy name offering fashionable designs once again.

Management is expecting constant-currency sales for the Coach brand to increase in the low-single digits during fiscal 2016. If the company can show in the coming earnings release that sales are in fact stabilizing and starting to grow once again, it could be a big positive in terms of evaluating the chances for a sustained turnaround in the middle term.

Coach has recently acquired footwear company Stuart Weitzman in an effort to become a multi-brand business and capitalize on new growth opportunities. The company is expecting Stuart Weitzman brand sales in the area of $335 million during fiscal 2016, an increase of nearly 10% from fiscal year 2015. In addition, men's accessories and international markets, especially China, are important growth areas to monitor in the coming earnings release.

Coach is restructuring the store base, closing underperforming locations, and renovating its stores to strengthen the company's image among customers. Management said in the latest earnings conference call that its North America fully renovated retail stores are generating positive comparable-sales growth in aggregate, so investors may want to keep a close eye on Coach's store base restructuring initiative, and its impact on the company's performance.