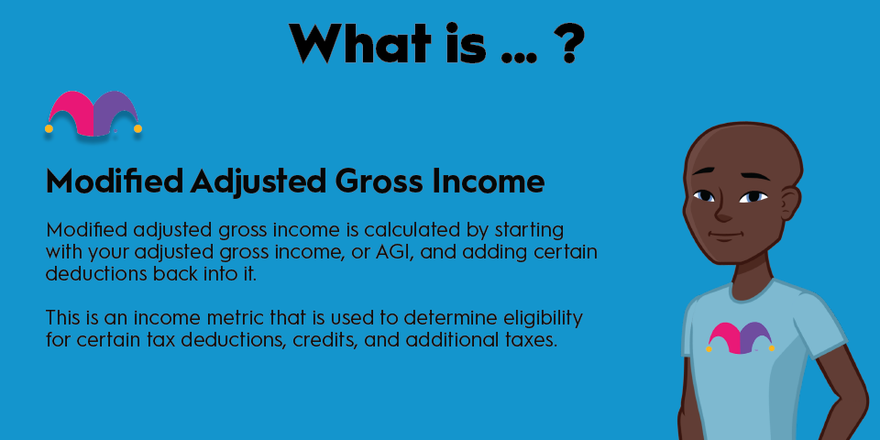

Modified adjusted gross income, also known as modified AGI or MAGI, is an income metric that is used to determine eligibility for certain tax deductions, credits, and additional taxes. In this article, we’ll discuss what MAGI is, why it’s important to you, and how to calculate yours.

What is modified adjusted gross income?

What is modified adjusted gross income?

Modified adjusted gross income is calculated by starting with your adjusted gross income, or AGI, and adding certain deductions back into it. As if calculating income metrics for tax purposes weren’t already complicated enough, the calculation method for MAGI can be slightly different, depending on its purpose.

For example, to determine eligibility for contributing to a Roth IRA, you would add the following to AGI:

- Student loan interest deduction.

- Excluded foreign earned income.

- Foreign housing deductions.

- Excluded savings bond interest.

- Excluded employer adoption benefits.

- Any traditional IRA deduction.

On the other hand, eligibility for the net investment income tax (NIIT) is determined by adding just the foreign earned income exclusion and certain adjustments for foreign investment activity. Other tax benefits whose eligibility is determined by their own variations of MAGI include:

- Education credits (American Opportunity Credit and Lifetime Learning Credit).

- Child Tax Credit.

- Premium Tax Credit.

- Traditional IRA deduction eligibility.

One important note is that all of the adjustments for even the lengthiest form of MAGI calculation don’t apply to most taxpayers. So for many people, MAGI and AGI are the exact same number -- and that’s been especially true while federal student loan interest has been paused.

Four different types of income

Four different types of income

Modified adjusted gross income is used to determine eligibility for some of the most common tax benefits in the United States, but it is one of four important income figures taxpayers should be aware of. In order of the (typically) largest number to the smallest:

- Gross income: Your gross income includes all of the money you make in a given year. For example, if your only source of income is your job, and you were paid a salary of $100,000, that is your gross income.

- Modified adjusted gross income (MAGI): This is an income metric that starts with your adjusted gross income, or AGI (more on that in a bit), and adds certain deductions back in.

- Adjusted gross income (AGI): This is calculated by starting with your gross income and subtracting certain adjustments, such as contributions to tax-deferred retirement accounts, student loan interest, half of the self-employment tax, health savings account (HSA) contributions, and a few others. For many people, AGI and MAGI are the same number.

- Taxable income: This is your AGI minus all of your tax deductions. In short, your taxable income is the number you actually pay income tax on and is usually significantly lower than your AGI and gross income.

Why is MAGI important?

Why is MAGI important?

MAGI is important because it determines your eligibility for certain tax benefits. The ability to deduct traditional IRA contributions and to contribute to a Roth IRA depends on your MAGI, as does the ability to use the valuable Child Tax Credit. It is also used to determine eligibility for the American Opportunity Credit and Lifetime Learning Credit for education expenses, as well as for the Premium Tax Credit for Americans who get their health insurance from the marketplace.

It can also be used to determine if you have to pay certain taxes, particularly the net investment income tax (NIIT), which is a 3.8% tax added to the investment income of certain high-income households.

Example

Example of calculating MAGI

As an example, let’s say that you’re single and want to determine if you can contribute to a Roth IRA in 2023. According to the IRS guidelines, your MAGI must be less than $138,000 to make a full contribution or less than $153,000 to make a partial contribution.

For 2023, you expect your adjusted gross income to be $135,000, but you paid $2,000 in interest on private student loans and had $500 in excluded savings bond interest. This makes your MAGI $137,500, so you will still qualify for a full Roth IRA contribution in 2023.