The penalty kick is one of the most dramatic moments in soccer. It's what results when an offensive player has been fouled inside the the 18-yard box that surrounds the goal, the defense unfairly taking away a scoring opportunity. When that happens, the referee blows his whistle and points to a white line 12 yards from the goal. From that spot, the offensive player will get a free shot on goal, facing only the opposing team's goalie.

The penalty kick. Image source: Getty Images.

This penalty kick has a high likelihood of resulting in a goal. In fact, some 90% of penalty kicks at the professional level reach the back of the net. That's because any professional worth his salt is going to strike the ball at approximately 70 miles per hour, putting it on goal in less than a second.

What's more, this penalty kick has a high probability of deciding the outcome of the match. In soccer, the team that scores first tends to win, or tie, almost 75% of the time. This, in other words, is a situation with a lot on the line.

Now imagine you're the goalkeeper. What should you do to prevent the other team from scoring?

There's what you do, and what you should do

It turns out that what professional goalies should do in this situation is very different from what they empirically do. What goalies most often do in this situation is guess. Assuming the taker of the penalty kick is aiming for one corner of the net or the other, the goalie tries to guess to which side the ball will be kicked. Then, just as the offensive player is about to kick the ball, the goalie will dive toward one side of the goal or the other in the hopes of blocking the shot.

Generally, this approach results in the goalie diving to the wrong side of the goal. That happens because the goalie doesn't think he has the option of waiting to see which side the ball is going to before deciding which way to jump. He moves early, with no information on which to base his decision.

This haphazard approach, coupled with the skill of professional penalty kick-takers, explains why some 90% of penalty kicks are converted. But what else could a goalie do?

A team of researchers from Israel studied thousands of professional penalty kicks and discovered that there is a better way -- a way that would nearly triple the odds that the goalie would stop the ball.

That way is to do nothing.

It makes sense why this approach would yield better results. Standing still -- or doing nothing -- means the goalie should stop anything shot near him, and it would also give him the chance to react to any ball that is not perfectly struck. In fact, the research suggests a stationary goalie would improve his save rate from a paltry 13% to a respectable 33%.

That improvement would lead to dramatically different outcomes at the very top tiers of professional soccer -- outcomes professional goalies spend thousands of hours training (and are paid millions of dollars) to produce. And yet, against their best interest, professional goalies almost never do nothing.

People's inclination to act, even when doing so is against our best interests, has a name: action bias. And action bias isn't just the enemy of the professional soccer goalie.

The tough thing about action bias

Action bias is pervasive in our lives. From changing lanes in traffic, to clicking relentlessly when a computer freezes up, to over-scheduling a son or daughter, it's our compulsion to act even when situations are outside our control. And it's a hallmark of who we are as human beings.

Consider the case of Adam and Eve. All Adam and Eve had to do to stay safe and content in utopia forever was to not do one thing, which was eat from the Tree of Knowledge of Good and Evil.

And God said, "Let there be action bias." Image source: Getty Images.

Yet depending on how you count time in the Bible, they may not have made it a single day. Observers can try to blame the serpent, but that fruit was going to get eaten eventually. Why? Hubris. Exceptionalism. The idea that the rules don't apply.

In the case of the professional soccer goalie, thousands of hours of practice, million-dollar paychecks, and the adoration of supporters affirm that he can produce above-average outcomes through deliberate action. But the math in the case of the penalty kick is clear: The goalie is almost three times more likely to prevent a goal by standing still, rather than attempting to anticipate the kick.

The math is not always so clear, but whether you're a lane-changer, a mouse-clicker, a parent with high expectations, or, as we'll see, a big business CEO or a stock market investor, you fall prey to action bias. And you do so to your detriment.

Dirty words

Four words explain this phenomenon, and they are at the core of who we are: delusion, fear, insecurity, and pride. Why do these feelings compel the professional soccer goalie to act, rather than remain still, when a penalty kick is taken?

- Delusion. Despite evidence to the contrary, the individual professional goalie believes he is exceptional -- far better than his peers -- and thus his odds of making the save are better.

- Fear. There are sometimes hundreds of thousands of people watching professional soccer games, and there is a long history of professional soccer players suffering professional and personal repercussions after failing on the game's brightest stages. Under such incredible pressure, how can a goalie be expected to sit pat?

- Insecurity. Being in control is comforting. How could an athlete sleep at night knowing that despite his salary and training, he may as well be replaced by a cardboard cut-out in the highest-pressure scenario in the game?

- Pride. The entire stadium is cheering for the goalie to make the save, to save the game, to bring home the win. The fans want to see a job well done.

Yet whether he acts out of delusion, fear, insecurity, pride, or some combination of the four, the overactive goalie is reducing the likelihood that he will prevent a goal. Meanwhile, the impatient driver risks causing an accident, the incessant clicker risks slowing the computer down further, and the overbearing parent risks preventing their children from discovering on their own what they're passionate about.

These are all risks with costs attached to them, but doing nothing isn't just about avoiding costs. It can also add value to your life -- and even save it.

Live safely

Writing in his book Deep Survival: Who Lives, Who Dies, and Why, author Laurence Gonzales explains how action bias and the hubris associated with it can turn the most mundane outings into life-or-death situations.

Think of hikers who get lost in the woods and, delusional about their ability to reach their destination, keep hiking instead of staying put -- thereby making it impossible for rescuers to find them. Or climbers who ignore the weather, taking so much pride in their skill that they assume they can handle any situation. Or paddlers who fall overboard and, frightened at the prospect of giving themselves over to float down the river, attempt to stand up in moving water. It turns out that these compulsions to action are all good ways to get yourself killed. Survivors, Gonzales concludes, face reality, stay cool, and don't do anything needless or rash that might make a situation worse.

The dark secret of big business

In the world of business, the situation that most resembles a penalty kick is the merger or acquisition. Just as 90% of penalty kicks fail to be saved, 90% of big corporate deals fail to achieve pre-deal expectations and end up destroying shareholder value. What's more, the feedback is almost as fast.

For example, Cisco Systems acquired Flip Video for $590 million in March 2009. By April 2011, Cisco had shut Flip down and written it off, admitting in accounting terms that the company got nothing for its $590 million.

Google, in a bigger deal, bought Motorola for $13 billion in 2012 with lofty expectations for growing its hardware business. Two years later, Google gave up and sold the unit to Lenovo for $3 billion.

AOL Time Warner, a massive merger meant to create an online content and distribution empire, was unwound within a decade. Bank of America nearly put itself out of business by acquiring Countrywide Financial at the height of the housing bubble. YUM! Brands paid up for a restaurant chain in China called Little Sheep and then never spoke of it again.

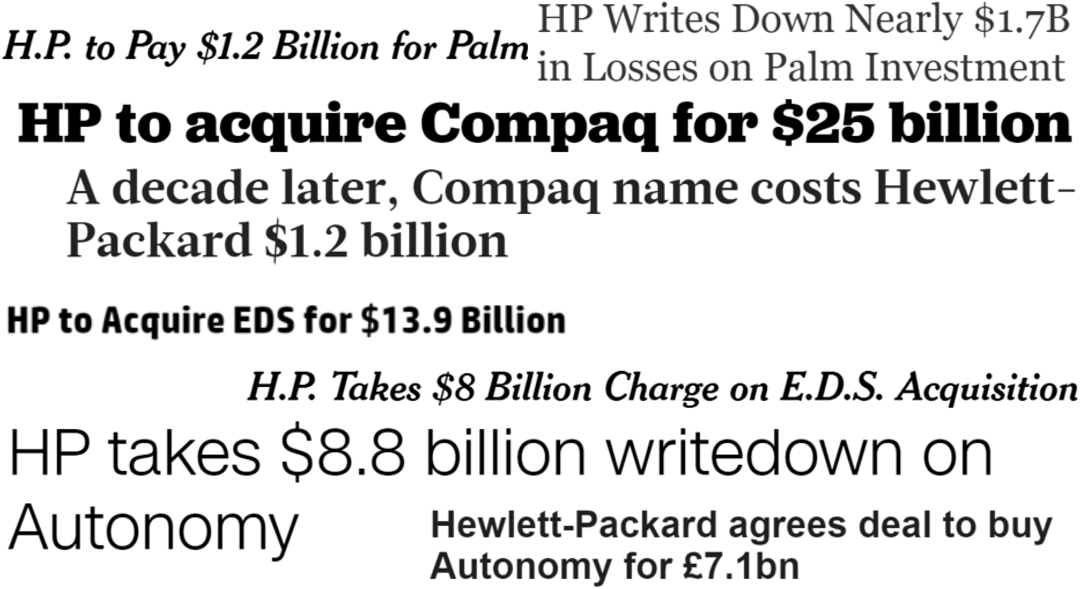

On and on it goes, culminating in the unsurpassed track record of Hewlett-Packard: Tens of billions of shareholder dollars wasted in little more than a decade.

Incredibly, two of these $8 billion writedowns happened in the same year.

Despite this long track record of value destruction, big companies continue to strike deals. 2015 was the biggest year in history for M&A, with $3.8 trillion spent by companies to buy other companies. They're all long shots. The math is clear. Some acquisitions will work out -- Google's YouTube buy and Disney's acquisition of Pixar come to mind -- but those are the exceptions that prove the rule. They are the equivalent of the goalie who guesses right, or the driver who changes lanes just as the police clear the accident.

More often, the synergies will not be realized, and shareholders will not benefit. But whether it's because of delusion, fear, insecurity, or pride, the wheeling-and-dealing CEO can't be accused of lack of effort.

The best investors are dead investors

Finally, we come to the world of investing. There's a story -- perhaps apocryphal -- that Fidelity once looked at all of its accounts to determine what its best-performing investors were doing right. After doing some digging, they concluded that the best long-term returns were being earned by account holders who were either dead or had forgotten they had accounts at Fidelity.

Whether that's a true tale or a tall tale, there are plenty of other studies that demonstrate that when it comes to making money, investors are their own worst enemies. One, "The Behavior of Individual Investors" by California-Davis professor Brad Barber and California-Berkeley professor Terrance Odean, is a particularly depressing read. Here's what Barber and Odean conclude about investors:

They trade frequently and have perverse stock selection ability, incurring unnecessary investment costs and return losses. They tend to sell their winners and hold their losers, generating unnecessary tax liabilities.

In other words, investors are doing everything wrong when it comes to managing their portfolios.

What makes the Barber and Odean study so depressing is that investors mean well. When they trade, they are trying to make money. They think they're putting their money into a more promising opportunity or taking some risk off the table, not realizing that a new stock likely has to do approximately 50% better than the old stock for the trade to break even. And they're doing so to achieve important financial goals such as funding a child's college education or a comfortable retirement. But in so doing, they are falling victim to action bias -- to delusion, fear, insecurity, and pride -- and making it less likely they will achieve the outcomes they seek.

Fortunately, there's a solution that stops short of forgetting about your accounts -- or worse, dying. It's for us all to do what professional soccer goalkeepers should do when facing down a game-deciding penalty kick: Stop trying so hard.

How to do nothing

This is easier said than done, but there are some helpful frameworks. First, set goals around inaction and celebrate their achievement. For example, I track how long it's been since I sold a stock, just as factories track their safety records.

Second, define success differently. The financial-industry standard in investing is to define success by measuring return against a benchmark, goading investors into trying to beat the market over shorter and shorter periods of time. But the fact is that most investors who try to beat the market are putting the nail in the coffin of that very aim. "Beat," after all, is a verb that means repeated, deliberate action, and the data shows that on the way to long-term outperformance, investors must tolerate sustained periods of woeful underperformance when nothing seems to work. So measure differently.

I declared 2015 my most successful year as an investor not because I earned the best returns of my career, but because it was the first year in my career in which I did not sell a single share of any stock. A lot of work went into making that happen. I had to own a portfolio composed of only my most favorite ideas, and I had to make sure I had exposed an amount of money to the vagaries of the stock market so significant that it would make me uncomfortable.

The opposite of 2015 for me was 2009. In 2009 I owned some names with obvious flaws, and with a baby on the way and plans to buy a house, I felt stress when my portfolio balance declined. That led me to sell stocks in the depths of a bear market. That's a bad investing year.

Finally, reserve action for those times when what you're doing is clearly a reasonably good investing decision. That means it has to be simple and inexpensive. If it's complicated, don't do it. If it's expensive, don't do it.

To be clear, action bias is not all bad. It's hardwired into us because it helps us survive. Standing around while you get attacked by a lion on the savanna is a lousy course of action.

But it's important to be aware of action bias and to take steps to combat it when it's compelling you to act against your own best interest. Whether you're a professional soccer goalie, a commuter, a parent, a CEO, or an investor, remember that -- and doubly so if you happen to be the CEO of Hewlett-Packard.