I read two interesting thoughts last weekend. The first is from legendary 18th-century economic god Adam Smith -- father of free-market thinking -- who wrote this on the topic of regulating banks:

exertions of the natural liberty of a few individuals, which might endanger the security of the whole society, are, and ought to be, restrained by the laws of all governments, of the most free as well as of the most despotical. The obligation of building party walls, in order to prevent the communication of fire, is a violation of natural liberty exactly of the same kind with the regulations of the banking trade which are here proposed.

The second came from JPMorgan Chase (NYSE: JPM) CEO Jamie Dimon's annual letter to shareholders, which says a skill he strives for is the "Ability to face facts."

Amen to both

The outcome of banking gone wild is now well-known. Less obvious are the dramatic changes banks underwent since the 1980s that concluded with the collapse of 2008.

By looking back over the past 25 years, it's easy to highlight Smith's point of banks running roughshod over everyone else. And we can show this with cold, hard facts Dimon appreciates.

The three facts that put our current financial system in perspective are charts of profit growth, compensation growth, and relative size of today's biggest banks. I owe credit for the inspiration of these charts to a presentation in March by former International Monetary Fund chief economist Simon Johnson. Let's look at each.

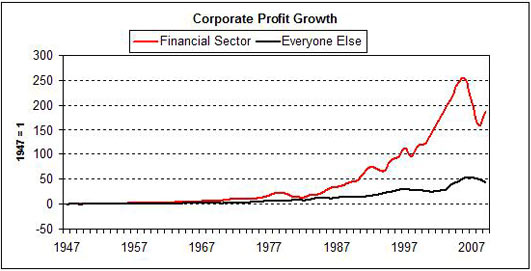

1. Money for nothin'

Every business, every corporation, and every consumer relies on banking in one way or another. That makes it a special industry, and it's why banks receive special treatment like backing from the Federal Deposit Insurance Corp. It also makes it an industry that should be at least somewhat anchored to the rest of the economy. When the economy does well, banking does well; when the economy does poorly, so do banks.

That's roughly how it worked for most of the post-World War II period until the early 1980s -- profit growth among banks hugged close to the businesses they lent to. Then something strange happened:

Source: Bureau of Economic Analysis, author's calculations.

Let me explain this chart a little more. The Bureau of Economic Analysis tracks total corporate profits by industry going back to 1947. I took total financial profits, and total profits from all other industries, and calibrated both groups to "1" in 1947. So what this chart shows is the relative profit growth of banks compared with everyone else.

From 1947 until the mid-'80s, financial profits and all other profits were fairly correlated. Then in the mid '80s ... snap! ... financial-sector profits left everyone else in the dust.

There are two explanations for this. One, we've had consistently falling interest rates since the '80s, which is great for most businesses, but banks especially. Two, the '80s were deregulation central. As Simon Johnson and James Kwak explain in the book 13 Bankers:

[A broad] deregulatory trend begun in the administration of Jimmy Carter ... transformed into a crusade by Ronald Reagan. The eventual result was an out-of-balance financial system that still enjoyed the backing of the federal government --- what president would allow the financial system to collapse on his watch? -- without the regulatory oversight necessary to prevent excessive risk-taking.

Two big innovations that came from this were an explosion of derivatives, and the securitization of debt. As the past two years taught us, both products can be great in moderation yet deadly when used in excess -- which they usually are.

The reason excess within financial products became standard is simple: Bankers were getting fat and happy off these things even when clients lost money. That brings up chart No. 2.

2. Lifestyles of the rich and fortunate

There was nothing glamorous about banking for most of the post- World War II period. The leaders made fortunes and gained power -- as leaders of all industries do -- yet the lower workers were just average Joes making average wages.

As with profits, that changed abruptly in the '80s:

Source: Bureau of Economic Analysis, author's calculations.

In 1959, the average finance employee made $4,880 a year, while the average in all other sectors made $4,560. By 2006, the average finance worker made $82,200 compared with $52,800 for everyone else. Nice.

The practice of paying bankers ungodly sums just for showing up isn't the historic norm. It's really something that sprung up in the '80s with the advent of financial engineering and the outburst of subsidized profits.

Another thing we've become accustomed to that isn't historically ordinary is the size of the largest banks. That brings up chart No. 3.

3. What too big to fail looks like

Source: Capital IQ (a division of Standard & Poor's), measuringworth.org, author's calculations.

This is the combined total assets of the four big commercial banks -- Citigroup (NYSE: C), Bank of America (NYSE: BAC), Wells Fargo (NYSE: WFC), and JPMorgan Chase -- as a percentage of gross domestic product. In 1992, the combined assets of these four banks amounted to 5.2% of GDP. By 2009, that number had increased tenfold, to 52% of GDP. The big jump came in the late '90s with the repeal of the Glass-Steagall Act, which allowed commercial banks to merge with investment banks. A second surge came in 2008 after surviving banks purchased their fallen neighbors.

This chart is particularly revealing because it thoroughly wrecks the claim -- made mostly by bank CEOs -- that megabanks must not be broken up because large companies like Apple and ExxonMobil absolutely need banks of today's size to conduct business. Eyeball the chart for three seconds and you realize how ludicrous this idea is. Big companies didn't struggle to raise capital in 1992. Or 1995. Or 2000. Or 2006. In fact, they thrived like never before. To suggest that reducing the size of big banks relative to GDP to where they were in, say, 1998, would somehow asphyxiate big businesses is comically refutable.

Don't shoot the messenger

These three charts don't tell the whole story, of course. You can gab away about how the Fed, Fannie and Freddie, China, the Democrats, the Republicans, the media, and whoever else you detest created the financial collapse. And please do.

What I hope they do is provide perspective. There's a growing group, without naming names, that acts like even the slightest smidge of financial reform will send us into a Socialist Stone Age. But when you see how dramatically and quickly the financial system skewed, you see how even significant reform would simply revert it back to where it was only a handful of years ago -- a time that was demonstrably more stable, produced higher growth, and, to the irony of all, represented the "old America" so many reform opponents want back.

Some say banks are making lots of money and paying themselves accordingly, but that's their right. That's capitalism. We encourage it. We cherish it. But as Adam Smith mentioned more than 200 years ago, it isn't capitalism if the misbehavior of a few bankers "endanger the security of the whole society." And that's exactly what happened in 2008.It wasn't capitalism. It was banks blowing up the economy. And a few of us are praying it'll soon end.

Check back every Tuesday and Friday for Morgan Housel's columns on finance and economics.