If you follow financial markets, you've probably heard of the VIX Index. It's often referred to as "Wall Street's fear gauge" because it tracks the market's expectation of short-term stock price volatility. Right now, the VIX is the canary in the stock market coal mine, warning us of the toxic complacency that is poisoning investors' ability to properly assess the risk of owning stocks. First, let me tell you why that's the case and then I'll identify several ways one can hedge those risks.

The following graph shows the full price history of the VIX index, beginning in January 1990:

Source: Yahoo! Finance.

The blue line represents the VIX, while the bold black line shows the index's long-term average value (20.4). There are two key observations to be made here:

- Periods of above-average values are followed by periods of below-average values and vice-versa (in fancy terms, the VIX is mean-reverting).

- The VIX is now about 17% below its long-term average.

How the VIX relates to your portfolio

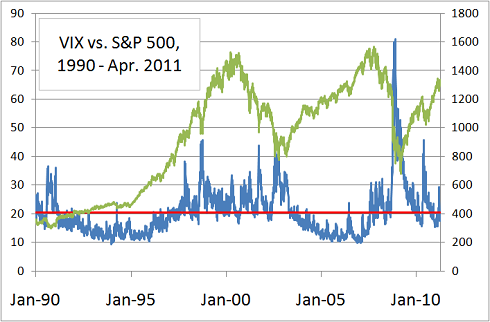

If all of this sounds wildly abstract and irrelevant to your portfolio, let me bring it home to you. Take a look at the next graph, which is the same as the previous one, with the addition of the S&P 500 (green line, left axis):

Source: Yahoo! Finance.

Two things are apparent from the graph:

- Long periods of below-average volatility are typically associated with bull markets.

- Conversely, during bear markets, investors will pay up to own options that provide their stock portfolios with downside protection.

This is not altogether surprising, since the VIX is derived from the prices investors are willing to pay for options on the S&P 500 index. Long periods of rising stock prices lower the incentive to buy options. Conversely, when stock prices are falling sharply, investors will pay up to own options that provide their stock portfolios with downside protection.

The fact that the VIX now sits below its long-term average does not mean that it has to spike upward anytime soon, concurrent with a correction in stocks. Go back to the previous graph: You'll see that since its inception, the VIX has experienced multiyear periods during which it remained below its long-term average (early to late '90s and the mid-'00s).

Is this market really less risky than average?

However, we're not reasoning in a vacuum here; the fact that the VIX index is lower today than its average value going back more than 20 years does suggest that investors are being complacent about the risks associated with owning stocks. Just consider a few of the factors weighing over financial markets now:

- A European sovereign debt crisis that is entirely unresolved, with an increasing risk of a breakup of the euro.

- Unsustainable fiscal positions in advanced economies, including the U.S., Japan, and the U.K.

- Spiking commodity prices, and in particular oil prices, resulting from supply shocks and political uncertainty.

Long-term optimist, short-term skeptic

On a long-term basis, I remain optimistic that the global economy will be able to wade through these problems successfully. In the short term, however, it's anyone's guess what the potential disruptions to the smooth functioning of trade and capital flows could be. And these are just three risks that we are already aware of; it does not account for black swans (though, mind you, these can also be positive, such as a major advance in renewable energy). In that context, here are some possible hedge ideas:

- If your portfolio is heavily tilted toward the U.S. or developed markets, consider adding exposure to emerging markets, which are on a sounder financial footing. Fellow Fool Tim Hanson isn't a big fan of index products such as the Vanguard Emerging Markets ETF (NYSE: VWO), but it is a cheap and straightforward option.

- Sophisticated investors (and only sophisticated investors) can consider a portfolio hedge using the iPath S&P 500 VIX Short-Term Futures ETN (NYSE: VXX), which tracks VIX futures, or options on this ETN.

- When the VIX is cheap, by definition, short-term options on S&P 500 futures are cheap also. Barring a spectacular anomaly, this will almost certainly hold for options on the SPDR S&P 500 ETF (NYSE: SPY). The trouble is that short-term options don't lend themselves to hedging a correction that is impossible to time; on the other hand, as Warren Buffett argued in the 2008 Berkshire Hathaway shareholders letter, the longer the maturity of a stock index option, the more likely it is overpriced, rather than underpriced.

- Investors might be able to hedge the volatility on high-profile stocks directly at some point, as the CBOE starts applying its VIX methodology to single issuers. The first wave of planned stocks: Apple (Nasdaq: AAPL), International Business Machines (NYSE: IBM), Amazon.com (Nasdaq: AMZN), Google (Nasdaq: GOOG), and Goldman Sachs.

The ultimate portfolio hedge

Whether you invest in index products or individual stocks, the best (and cheapest!) hedge is to combine a long-term investment horizon with a strict value discipline -- both of which look to be in short supply in the current market.

If you'd like to track the hedges mentioned in this article using My Watchlist, click here. Alternatively, if you'd like to track the protected stocks, click here. You'll get valuable updates as well as immediate access to a new special report, "Six Stocks to Watch from David and Tom Gardner." Click here to get started.