The global economy tends to be very cyclical, meaning it is prone to alternating periods of boom and bust. The four stages of an economic cycle are expansion, peak, contraction (also known as recession), and trough, followed by another expansion to mark the beginning of a new cycle. A typical economic cycle lasts about 5.5 years, although some are quite short (as little as 18 months) and others span more than a decade.

A supercycle is defined as a sustained period of expansion, usually driven by robust growth in demand for products and services. Economic supercycles tend to produce strong, sustained demand for raw and manufactured materials, such as metals and plastic, that exceeds what commodity producers can supply. Supercycles, which are also good for stock prices, are often associated with long-term periods of growth for the commodity markets.

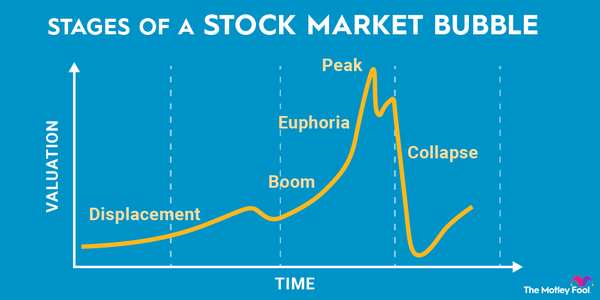

An example of an economic supercycle

An example of an economic supercycle

The last major economic supercycle began around 2002 when China entered an extended period of economic growth. The rapid industrialization and urbanization of that country, combined with China's acceptance into the World Trade Organization, catalyzed a supercycle.

China's economic supercycle fueled a similar extended boom in the global commodities market. The country's demand significantly increased for metals such as iron ore, copper, and aluminum, which are core components of infrastructure and manufactured goods. The country's producers were also consuming increasing amounts of energy. This robust demand caused commodities producers such as mining companies and oil producers to struggle to produce enough supply, which resulted in significant spikes in global commodity prices. For example, the price of copper, which for most of the 1990s was below $2,000 per ton, exceeded $10,000 per ton during this economic supercycle. The price of oil increased from $20 per barrel to a peak of more than $140 per barrel.

This economic supercycle ended around 2015 when China started tightening its lending standards. The increased difficulty of accessing credit slowed the country's pace of economic growth, and the demand for both materials and energy sharply declined. Crude oil prices, for example, decreased by 2016 to around $30 per barrel.

What does a supercycle look like?

What does a supercycle look like?

Commodity supercycles are driven by supercycles in the broader economy and are characterized by sustained rising demand for raw materials, manufactured materials, and sources of energy. But the commodities sector is especially cyclical, more so than the broader economy, because of the lag time that necessarily occurs between supply shortages and the completion of additional production capacity. Commodities producers struggling to meet demand often respond by initiating the development of new mines or oil fields, which can take years to complete. Too much new production capacity, which may be coupled with a reduction in the pace of demand growth, can cause supply shortages to become excesses in supply. The predictable result when supply significantly exceeds demand is that prices for the commodities crash.

A commodity supercycle is a sustained period, usually more than a decade, of increasing commodity demand. A long period of high commodity prices resulting from supply shortages greatly increases the amount of cash held by commodities producers, which prompts many of those producers to spend money on expanding their production capacities. Many commodities producers responding in a similar fashion to supply shortages increases the likelihood that too much new production capacity is created -- a dynamic that is only exacerbated by the long duration of supercycles. The difficulty of matching commodity supply with demand makes commodity prices especially volatile.

Different types of economic catalysts can trigger commodity supercycles. A few specific examples from recent history include:

- The industrialization of the United States in the late 19th century.

- The reconstruction of Europe and Japan after World War II.

- The emergence of China as a leading global manufacturer.

Each of these periods of sustained economic growth created step changes in demand for commodities. But regardless of whether demand for commodities is catalyzed by reconstruction or new growth, the result is the same during a commodity supercycle -- supply shortages cause commodity prices to rise, and the development of additional production capacity is initiated by commodities owners.

Commodities in demand

Which types of commodities are most in demand during a supercycle?

Economic supercycles tend to drive outsized demand for two types of commodities: industrial metals and energy, both of which are crucial inputs for the industrial economy.

The three most widely used industrial metals are:

- Iron ore: An essential component for making steel and constructing commercial buildings and bridges.

- Copper: Used to manufacture electrical equipment (such as wires and motors) and industrial machinery (like heat exchangers) and a key material in construction (such as for roofing and plumbing).

- Aluminum: A component of window frames, electrical transmission lines, airplane parts, and other manufactured goods.

The energy commodities that tend to be in high demand during an economic supercycle include:

- Crude oil: Crude oil is refined into petroleum products -- gasoline, jet fuel, and diesel -- and used for transportation and to power machinery.

- Coal: This commodity is purchased by electric utilities to produce electricity and by steelmakers (as coking coal or steelmaking coal) to manufacture steel.

- Natural gas: Natural gas is used by utilities, sometimes as a replacement for liquid fuels, to generate electricity.

Supercycles occurring in specific sectors of the economy can drive commodity supercycles for the materials most heavily used by those sectors. Here are three sector-specific supercycles that appear to be occurring and the materials most in demand by those sectors:

- Renewable energy development: Many foresee a multi-decade investment cycle ahead for renewable energy. Such a supercycle would drive increased demand for copper and steel since they're both vital components of solar panels and wind turbines.

- Adoption of electric vehicles: Advancements in battery storage technologies are partly driving the large-scale adoption of electric vehicles. With increasing demand for electric vehicles comes rising demand for battery metals such as cobalt, lithium, manganese, nickel, and graphite.

- Expansion of data infrastructure: Many people also foresee a massive investment cycle ahead for data infrastructure. Demand for industrial metals like copper would likely rise, along with demand for rare-earth metals, zinc, molybdenum, and other raw materials.

Aside from industrial metals, supercycles can also drive increasing demand for precious metals such as gold and silver. While commodity supercycles don't increase the industrial consumption of most precious metals, supercycles increase investor demand for precious metals because they can be used effectively to hedge against inflation.

Related investing topics

The next supercycle may not mirror those of the past

It's important to realize that a sustained transition to low-emission power sources and modes of transportation, along with a move away from industrialization and toward digitalization, could significantly change which commodities experience the most demand growth during a supercycle. These broad market transitions could negatively impact the demand for fossil fuel commodities such as oil, coal, and natural gas -- all of which have historically experienced robust and growing demand during a commodity supercycle. Given this possibility, investors should pay close attention to what exactly is driving an economic boom in order to invest in the commodities and producers likely to benefit the most over the long term.