Before March 1, Atlantic Power (AT +0.00%) was at the top of its game, doling out monthly dividends to the tune of 10% a year. Sure, there were skeptics who questioned how a small growth-by-acquisition utility could return that much cash directly back to shareholders, but the truth was this: Atlantic's dividend knocked every other utilities' out of the water.

But on March 1, the company reported quarterly earnings and announced a 66% dividend cut, shocking income investors who couldn't sell their shares fast enough. Atlantic, the company that had pumped profits into their brokerage account month after month, was waving the white flag. Its stock plummeted:

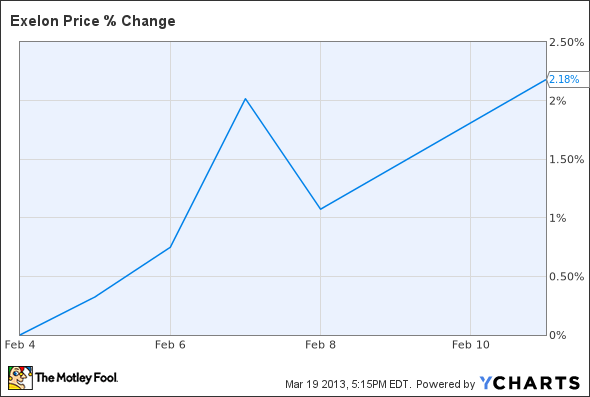

Atlantic wasn't the only utility to recently announce a dividend haircut. Exelon (EXC +1.09%) sliced its dividend by 40%, ending its 6.8% dividend yield for Q2 2013. But on Feb. 7, the day of the announcement, Exelon's stock bounced up.

Not all dividends are created equal

The reason for this mismatch is simple enough: Big dividends do not imply big profits, and Atlantic and Exelon are different companies. Their market caps alone put them in different bullpens, but each utility is in its own unique position. Their energy portfolios are different:

Source: Author; data from 10-K

Source: Atlantic Power 10-K

Their sales are headed in opposite directions, even as both utilities have acquired other businesses :

AT Revenue Quarterly data by YCharts.

And, most importantly, each is in a very different debt situation:

EXC Debt to Equity Ratio data by YCharts.

Insult to injury

After Atlantic's earnings report, I asked readers: Can it get any worse? The short answer: Yes.

As of last week, Atlantic may be in more trouble than even its books let on. Law firm Robins Geller Rudman & Dowd announced last Thursday that it is filing a class action lawsuit against Atlantic over allegedly misleading and/or false statements regarding its business and finances.

In its official complaint, the firm notes that "as the market learned the truth about Atlantic Power's mounting losses and its inability to maintain its outsized dividend through a number of misleading financial disclosures between Nov. 7, 2012, and March 4, 2013, more than $1 billion of the company's market capitalization disappeared."

These are serious allegations, and only time will tell whether Atlantic is found guilty of cooking its books. But either way, the once picture-perfect story of a darling dividend just grew darker.

Sustainable dividend

Big dividends don't imply big profits, but they don't imply big losses, either. Duke Energy's (DUK +0.97%) 0.23 cash dividend payout ratio ensures that its above-average 4.4% yield should be maintained for years to come, even as it dishes out $12 billion to modernize its aging generation fleet. Likewise, Ameren's (AEE +0.49%) 4.8% yield is supported by an enticing 0.76 cash dividend payout ratio, and the company's switchover to fully regulated businesses should provide some of the most consistent cash flow around.

And finally, let's consider the counterfactual: Small dividends don't imply big losses. NextEra Energy (NEE +1.43%), the largest producer of renewable energy in the U.S., offers investors a subpar 3.5% yield in exchange for a unique energy portfolio and potentially massive growth prospects.

Foolish bottom line

As dividends have delivered, dipped, or died, each utility's stock price has reacted differently over the years.

Atlantic's ready to reverse its downward demise with natural gas and renewable investments, and it may yet pull itself back into profitable territory. But if there's one lesson to learn from Atlantic's recent nosedive, it's that digging deeper is the only true way for investors to pull in long-term profit. Every company has a unique value offer, and it's up to individual investors to balance the various strengths, weaknesses, opportunities, and threats that inherently accompany any corporation.