The wealth-building power of compound interest will never cease to amaze me. It's a story of patience and attention to detail, where small, short-term differences add up to massive divergence over decades. And in the end, the biggest winners don't always deliver the fattest share-price returns.

Intel (INTC 0.53%) shares just passed the 4% dividend yield level -- again. The stock has been hit-and-miss in 2013, surging and falling like a high-octane roller coaster. Dividend payouts have remained stable, so the yield curve became a mirror image of the price chart. Right now, Intel's stock is falling again, which explains why effective yields are on the rise.

Either way, the dividend checks have grown like ragweeds over the past decade, and Intel's yields are extremely high in a historical perspective.

INTC Dividend Yield data by YCharts.

Not only that, but the company's board is getting a little overdue for another dividend policy boost. Payouts have grown an average of 12.8% over the last five years. Intel already offers the third most generous yield among the 30 Dow Jones Industrial Average (^DJI 0.62%) members; the next boost is likely to push Intel into second place.

Intel's share prices are suffering from the widely held idea that its products are becoming irrelevant. The onslaught of mobile computing solutions -- tablets, smartphones -- is powered by competing microchip designs, leaving Intel on the sidelines during a massive market revolution.

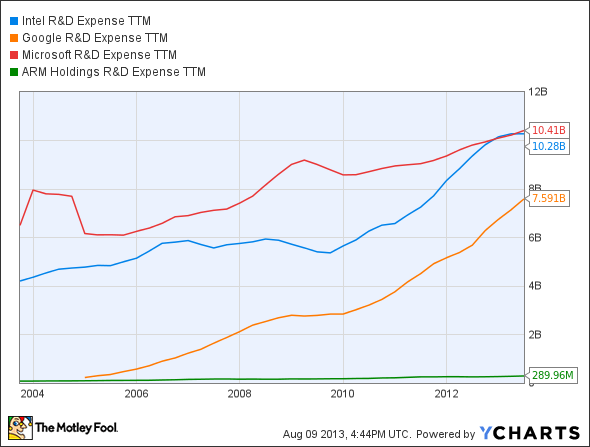

But then you're forgetting that Intel is getting its mobile house in order, and that the company can out-research pretty much anybody in Silicon Valley and beyond. Consider this telling chart:

INTC R&D Expense TTM data by YCharts.

Google (GOOG 0.54%) is one of the most innovative companies in the world. Big G spends more time shutting down failed experiments than many others do on their core projects -- and then Google starts another batch of experiments. It's no wonder that the company's R&D expenses are skyrocketing.

But Intel's R&D budget is not just larger than Google's -- it can also nearly match Mountain View's budget increases, blow by blow. That's no mean feat for a supposedly mature giant like Intel.

Microsoft (MSFT +0.45%) has pretty much always spent more on research than its hardware companion. But while Intel hit the gas pedal in recent years, Microsoft chose to respond to the changing marketplace by holding back on research. Intel is now spending just as much as Microsoft on paving the way toward future success, and that's new.

And mobile expert ARM Holdings (ARMH +0.00%), which provided the blueprints for the current generation of smartphone and tablet chips, is just a blip on the radar. You might think that the company would sink the windfall from its mobile success into heavy research on the next Next Big Thing, but the numbers tell a somewhat different story. ARM's R&D budgets have increased by 84% over the last five years. Intel largely kept pace with a 75% boost.

Economies of scale really do matter. Come back in another five years and see what's new. You'll find Intel firmly established in the now-mature mobile market while ARM fights to find another winning lottery ticket. Intel's earnings will bounce back with mobile support, enabling even more dividend increases.

Intel is too big, too rich, and too forward-thinking to be forgotten. This is why I own Intel stock myself. There's also a bullish CAPScall to go along with the real-money position. The rich dividend is delicious icing on the undervalued cake.