Investors are always looking for undervalued, top-quality brands with strong potential for international growth. This has become very difficult in today's business climate. Coach (COH +2.63%) may be one rare example. Despite being a luxury good manufacturer in excellent financial condition, with lower price points than most of its direct competitors and strong exposure to emerging economies, so far this year the stock has been underperforming, with an overall return of -3.38%. Does this represent a buying opportunity?

Rock-solid fundamentals

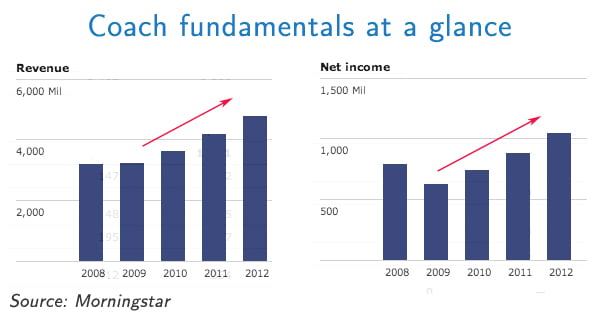

Historically, Coach has performed well. Because Coach products are expensive and frequently given as gifts, the company's revenue did not grow between 2008-2009, as customers made significant reductions in their discretionary spending. However, Coach's fundamentals have improved significantly since the Financial Crisis, both in terms of revenue base and margins. The bad news is that after four years of healthy growth, investors now seem worried about whether Coach can continue on this positive trajectory.

Source: Morningstar financial spreadsheets.

However, such worries may not be justified. Although North American comp-store sales saw a 1.7% decline in volume, the latest earnings call figures show that Coach did fairly well overseas. Despite a weaker yen causing adverse currency fluctuations in the third quarter, Coach had an increase of 6% to $382 million in overseas sales. In China sales were up 40% in the third quarter. Without the adverse currency fluctuations, Coach's overseas sales would have been up 14%.

International expansion

Coach just opened its 100th Chinese store this past quarter. There is plenty of room to expand in Indonesia, Malaysia, Latin American and Singapore, where their presence is still limited. Continued international expansion will improve Coach's revenues, including cash flow.

A promising move into the shoe market

In March of this year, Coach entered the shoe market in cooperation with Jimlar Corporation. It launched a new line of shoes in 170 North American retail locations. The launch will continue into more locations as the year plays out. The company predicts $250 million in footwear sales by the end of the fiscal year. The upshot is that this move into footwear may risk Coach's historically high margins in the short term.

Valuation

Over the past three years Coach has converted 22.8% of its revenue into free cash flow. Considering that Coach's international presence is still very limited, the company won't have any problem growing its business. It doubled its sales in China in 2010 to $100 million, and looks to achieve $500 million in sales in China by 2014. On the other hand, as Coach increases its scale of operations, sourcing and distribution advantages will help to reduce its cost base. These two trends are already set in motion, and will contribute to further strengthening cash flow generation.

Coach's competitors

In the latest earnings call Tiffany & Co. (TIF +0.00%) announced better than expected results. This is due to the jewelry company's strong presence in Asia. Its global sales increased 9% year over year to $895 million. This was well above the consensus estimate. Earnings per share were 10% higher year over year, at $0.70 per share.

But trading at 25 times earnings, Tiffany & Co. also has some worrisome issues. I am particularly concerned about their exposure to Abenomics. In fact, the company achieved a 21% growth in sales in the island of the rising sun, ex-currency. But because of a weaker yen, this resulted in a real growth rate of only 2%.

What's interesting is that Tiffany & Co. actually increased the price of its products in Japan. This was intended to offset the negative effect of Abenomics on margins. Although the risk of increasing prices is that it may decrease sales, in Japan the price increases seems to have had the opposite effect. The higher its prices, the higher the demand for its products. This is a unique competitive advantage.

Guess? (GES 0.06%) is also in the business of selling luxury goods and accessories. Although its fundamentals are not improving, its stock price is, suggesting an overvaluation.

Unfortunately, Guess has little exposure in Asian markets. This might be reason enough to be bearish. Even worse, its revenue in America fell more than Tiffany's or Coach's, despite dealing with the same macroeconomic conditions, Guess may be more vulnerable in the current economy. That's probably because its revenue, which relies heavily on apparel, is more exposed to business cycles. Apparel is constantly changing, depending on the trend in fashion.

Final foolish thoughts

Coach is a unique company with strong brand awareness. It's currently undervalued due to its untapped potential in the Asian markets, where there is plenty of room for growth. Strong financial performance since 2008 shows the luxury company has completely recovered from the crisis and managed to remain fashionable. With its emerging foray into the shoe market, it seems perfectly poised for an exciting future. What else would an investor look for? Just like its famous bags, its current share price is just too pretty to ignore.