Shares are up 50% this year for Adobe Systems (ADBE +0.47%) even though sales have been poor. Revenue declined 10.1% from the same period a year ago. Apparently, the Street believes Adobe will recover. What does the future hold?

Not just a poor quarter

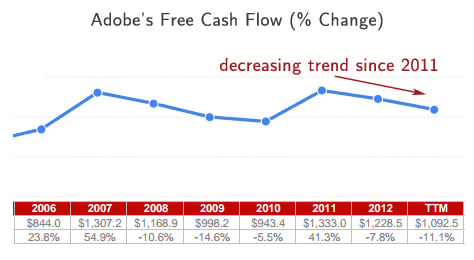

Adobe's free cash flow has been declining steadily since 2011, as shown in the image below. The reason may be its stagnant business model. It has continued to sell its software through Creative Suite products with perpetual licensing agreements.

Source: Oldschoolvalue

In an attempt to offset the negative influence of its legacy business, Adobe is now shifting toward a subscription, cloud-based model called Creative Cloud.

In theory, Adobe should be on solid footing after this transition. Paid subscriptions will roll in monthly. It also opens the door to additional paid services such as storage, special updates, training, and maintenance. So far, Adobe appears to be making progress, exiting the second quarter with 700,000 paid subscriptions.

But Adobe faces two major challenges: increasing competition in the cloud market and a recent shift in technological preferences with developers rapidly moving from Adobe Flash to HTML5.

How will these challenges affect Adobe's growth.

Increasing competition

Adobe's Creative Cloud, for which subscriptions average $50 a month, faces increasing competition from at least 15 other solution providers. GIMP is free to users and Sketch competes with Adobe Fireworks for a one-time fee of $50.

Adobe's Marketing Cloud, which has so far grown only 7% this year, is struggling, although it does offer an excellent integrated marketing solution. The reason is fierce competition. The industry is still dominated by Salesforce (CRM 0.03%), which recently spent $2.5 billion to acquire email marketing vendor ExactTarget to further broaden its platform of offerings.

Salesforce goes beyond marketing solutions, covering every step of the process from sales automation solutions to customer relationship management. This attracts users who prefer to rely on just one cloud provider. Salesforce's business model is already based on subscriptions. And to keep its subscribers engaged, the company provides frequent updates, training, certifications, and permanent support. As a result, its revenue is recurring and can be used to finance the necessary acquisitions to keep the company dominant.

Marketo (NASDAQ: MKTO) is another company competing in the cloud marketing arena. With fewer resources than both Adobe and Saleforce, Marketo generated revenue of $14 million in 2010, $32.4 million in 2011, and $58.4 million in 2012. That translates to 131% and 80% year-over-year growth, respectively. Conversely, Adobe's cloud marketing unit only grew 17% last year.

Marketo's products are very easy to use for marketing automation, social media, sales insight, and revenue analytics. Its products are among the least expensive in the industry. But because Marketo only has 2300 customers, its revenue growth is still not enough to generate consistent cash flow. The company had a $1.21 loss per share in 2012.

Are we approaching the end of Flash?

Web developers are moving from Adobe Flash to HTML5 because it is more suitable for mobile development. But Adobe stopped developing mobile versions of Flash nearly two years ago. Apparently Adobe felt it couldn't compete in the emerging mobile marketplace with HTML5 having some very important technological advantages. HTML5 is faster, doesn't need plug-ins and reads and stores data from the hard disk.

It wouldn't surprise me if Flash also disappeared from the desktop arena. This would negatively influence any revenue still coming in from Adobe Flash Professional.

Signals of overvaluation

Oldschoolvalue financial spreadsheets confirm that Adobe's current stock price is higher than the value its fundamentals dictate. A discounted cash flow model with a 9% discount rate, 3% terminal growth rate and 5% average cash flow growth rate for the next 10 years shows a fair value of $37 per share. This implies a 21% downside.

Source: Oldschoolvalue

Final foolish thoughts

While Adobe's transition to a subscription cloud based business model brings new opportunities, it's over optimistic to assume this comes with a quick or huge growth in revenue once the transition is complete.

Adobe faces stiff competition in cloud marketing and in its Creative Cloud flagship unit. With the end of Flash looming and the effect that could have on the company, Adobe's current valuation may not be sustainable in the medium run.