Most of the attention in the currency markets continues to center on the U.S. dollar and any potential volatility that could be seen if the Federal Reserve starts to signal an end date for its quantitative-easing programs. Of course, a scenario like that would be heavily bullish for the greenback. Given the long-term weakness in correlated assets like the PowerShares DB US Dollar Index Bullish ETF (UUP 0.29%), a majority of the market is watching intently for new developments.

However, there is still money to be made in some of the less popular markets, and central-bank commentary out of Switzerland last week suggests that assets tied to the Swiss franc are set for prolonged weakness against their major-currency counterparts.

Bounces this year in the CurrencyShares Swiss Franc Trust (FXF +0.38%) have been minimal at best, but last month prices broke above the January highs of just more than $109. It makes sense to look at some of the underlying factors at work to determine whether this latest breakout marks the beginning of a new trend or another selling opportunity. Centrally important is the steady stance of the Swiss National Bank, which reiterated this week its intention to maintain its currency price floor relative to the euro. The EUR/CHF price floor of 1.2 has been in place since September 2011 as a measure to protect the export-driven economy from slipping into recession and to stop deflationary pressures from building. This price floor essentially prevents the euro from rising above a ratio of 1.2 against the Swiss franc. Prior to these actions, the franc had approached parity with the euro as its safe-haven allure drew investors away from the increasing uncertainty of the debt-laden eurozone.

SNB tries to focus on fundamentals, rather than sentiment

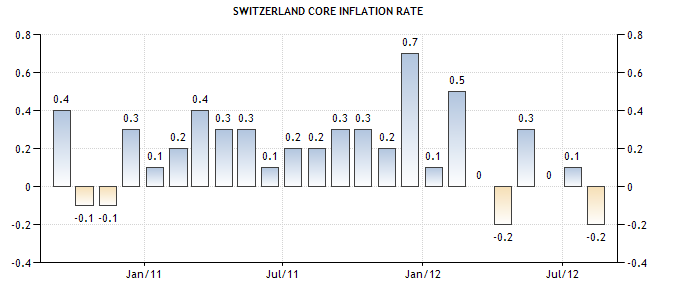

Consistent action by the SNB suggests that the CurrencyShares Euro Trust ETF (FXE +0.32%) will outperform ETFs tied to the Swiss Franc well into next year. What could derail this forecast? Any suggestion that the SNB is changing its stance. This will depend on the outlook for inflation, as well as earnings prospects for Switzerland's export markets. In the chart below, we can see there is little risk of a shift in dynamics anytime soon, as consumer prices have actually fallen in recent quarters.

Source: Trading Economics.

Switzerland's latest official statistics on consumer inflation actually show that prices are falling relative to historical averages. This removes a major cause for concern at the SNB that could have otherwise led to a change in policy expectations.

Watching interest rates

Comments from the SNB have also made it clear that the central bank is ready and willing to use additional tools to support the economy and prevent recession. With interest rates already at zero, however, there is little flexibility for the SNB to make any changes to its rate policy. Doing so would almost certainly encourage investors to put pressure on the established price floor. For now, there is little to suggest that we will see any bullish moves in ETFs tied to the Swiss Franc anytime in the next few quarters. Whether this means investors should consider assets tied to the euro or the U.S. dollar is another issue. That decision hinges on policy at the Federal Reserve. In any case, both the euro and the dollar are well-positioned to outperform the Swiss franc well into next year.