The market's valuation of Oracle (ORCL -4.21%) continues to suggest doubt over its future direction. It's traditional on-premise on-license sales are being threatened by pure-play software as a service, or SaaS, companies like Workday (WDAY +5.84%) and Salesforce.com (CRM +4.24%). Meanwhile, analysts are also questioning its future margins, given that management declared an intent to be "price competitive" with Amazon (AMZN -0.70%) Web Services and Microsoft's (MSFT +0.02%) Azure. Are the skeptics right about Oracle, or is the stock a good value?

Oracle reports a good second quarter

After disappointments from IBM and Cisco, investors have approached Oracle's recent results with caution, despite the fact that the numbers came in slightly better than expected.

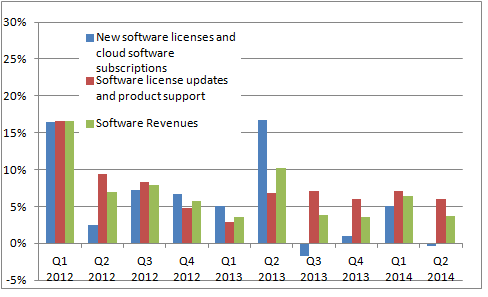

- New software licenses and cloud software subscriptions (26% of revenue) grew 1% constant currency growth vs. internal guidance of -4%-6% growth.

- Hardware systems product sales declined 2% in constant currency vs. internal guidance of -9%-1% growth.

- Non-GAAP earnings were $0.69 vs. internal guidance of $0.65-$0.69.

Although new software licenses and cloud subscription growth appears weak, Foolish investors should note that the company came up against some very strong numbers from last year's second quarter.

Source: company presentations.

Oracle's management articulated that its mix of software sales had a larger share of renewals and annuity deals versus new license deals. This kind of shift usually involves trading off some upfront revenue for an income stream over time. Indeed, Oracle's management argued, "you would think it would take you a couple to three years to get to that full productivity of the equivalent of a recurring stream of revenue to what you would have typically seen in license."

In other words, Oracle's revenue is likely to be negatively affected in the short term with this shift toward subscription-based sales.

The geographical breakdown confirmed Oracle's strength in the Americas, with sales up 5%, along with "good growth" in China. However, the real talking point is how aggressively Oracle is seeking to expand its cloud infrastructure services.

Oracle takes on Microsoft, Amazon, and Rackspace

As you would expect from a megacap tech company, Oracle's cloud offerings include SaaS, applications, and infrastructure. However, on its recent conference call, Oracle's CEO, Larry Ellison, explained that his company's plans involve being "price competitive" with Amazon, Microsoft's Azure, and Rackspace. Ellison also plans to make Oracle "highly differentiated at both the platform level and the application level."

The plan can easily be criticized for potentially sacrificing infrastructure margins at the expense of chasing future revenue. The market is competitive enough already, as Microsoft has already promised to match Amazon on pricing and features.

Oracle needs to address the threat that pure-play SaaS companies like Salesforce and Workday will grab market share within their respective niches of customer relation management and human capital management. Therefore, a strategy like this will help efforts to retain leadership with long-term recurring revenue from cloud applications.

Similarly, Microsoft and Amazon have their own services that will benefit from selling cloud infrastructure at less-than-optimal prices. The important strategic issue for Oracle is to remain relevant as SaaS solutions become more important.

Oracle's financial firepower and margins

Oracle has the financial firepower to make these moves. It's trailing twelve month free cash flow generation of $14.6 billion represents approximately 9.6% of its enterprise value. Furthermore, Oracle is investing in dedicated sales teams to compete for business against Workday and Salesforce. Sales and marketing expenses increased 12% in constant currency during the quarter, as Oracle built out sales capacity to win future business in the cloud.

All told, these initiatives may trim margins, but Oracle has a lot of financial leeway, and so does its valuation. Despite a 20% rise in the last six months, the stock still trades on just 12.5 times forward earnings to May 2014. Operating income margins fell to 36% in the first half, versus 37% last year, but 80% of the increase in operating expenses came from investments in sales and marketing.

The bottom line

Investors can be quick to criticize management for failing to adjust to structural changes, but Oracle is making significant efforts to manage the transition of software into the cloud. Investments in sales capacity, infrastructure services, cloud-based acquisitions, and efforts to respond directly to the threat posed by Salesforce and Workday are all demonstrations of intent.

Oracle is responding to structural changes in its marketplace, and it will take time to come to fruition. However, the stock's valuation suggests it can withstand some margin erosion along the way.