Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does Windstream Holdings Inc (WIN +0.00%) fit the bill? Let's take a look at what its recent results tell us about its potential for future gains.

What we're looking for

The graphs you're about to see tell Windstream's story, and we'll be grading the quality of that story in several ways:

- Growth: Are profits, margins, and free cash flow all increasing?

- Valuation: Is share price growing in line with earnings per share?

- Opportunities: Is return on equity increasing while debt to equity declines?

- Dividends: Are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let's take a look at Windstream's key statistics:

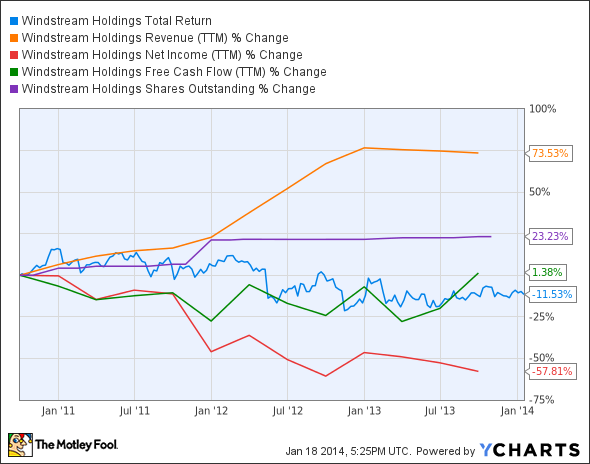

WIN Total Return Price data by YCharts.

|

Passing Criteria |

3-Year* Change |

Grade |

|---|---|---|

|

Revenue growth > 30% |

73.5% |

Pass |

|

Improving profit margin |

(75.7%) |

Fail |

|

Free cash flow growth > Net income growth |

1.4% vs. (57.8%) |

Pass |

|

Improving EPS |

(68.6%) |

Fail |

|

Stock growth (+ 15%) < EPS growth |

(11.5%) vs. (68.6%) |

Fail |

Source: YCharts. * Period begins at end of Q3 2010.

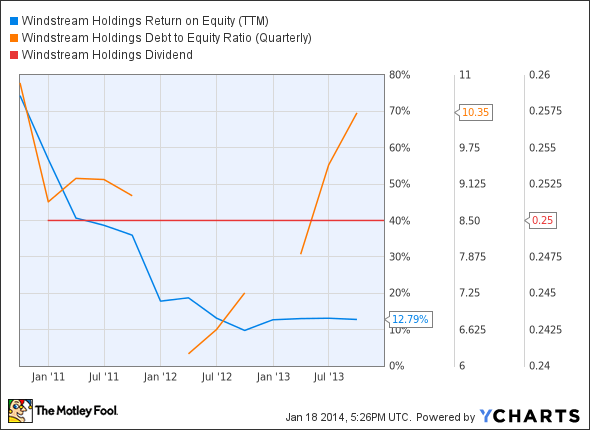

WIN Return on Equity (TTM) data by YCharts.

|

Passing Criteria |

3-Year* Change |

Grade |

|---|---|---|

|

Improving return on equity |

(82.8%) |

Fail |

|

Declining debt to equity |

(4.7%) |

Pass |

|

Dividend growth > 25% |

0% |

Fail |

|

Free cash flow payout ratio < 50% |

80.4% |

Fail |

Source: YCharts. * Period begins at end of Q3 2010.

How we got here and where we're going

Things don't look good for Windstream -- the telecom services provider earns a measly two out of nine possible passing grades. Although Windstream's revenue has soared over the past three years, the company's profit margins have collapsed as it struggles to build out the infrastructure necessary to support its next-gen offerings. Windstream has been an income investor favorite thanks to its hefty dividend yield, but this payout has been flat and its free cash flow payout ratio seems unmanageably high at present. Let's dig a little deeper to find out what Windstream is currently doing to overcome its fundamental weaknesses.

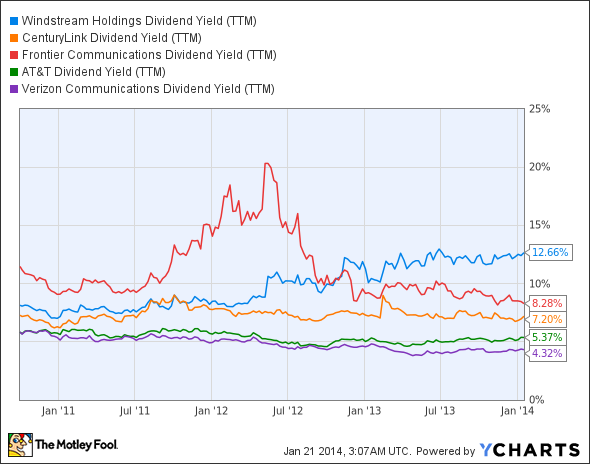

Over the past few years, regional telecoms Windstream and CenturyLink (CTL 1.23%) have both faced major headwinds in high-margin areas like enterprise telecom and residential broadband. The rising demand for smartphones has siphoned customers away from landlines, which has forced regional telecom providers to build out their high-speed Internet, digital video, and enterprise businesses. Fool contributor Chad Henage notes that AT&T (T +4.30%), Verizon, and Windstream all reported landline losses of at least 6% in their current quarters, so the landline exodus is nationwide and hardly confined to regional providers. However, Windstream's dividend yield, presently above 12% despite losing customers in its core segments, has held up above its telecom peers for at least a year since Frontier Communications (FTR +0.00%) was forced to slash its payouts:

WIN Dividend Yield (TTM) data by YCharts.

Quite recently, Windstream's management had to reassure investors that the company generates enough amount free cash flow to support quarterly dividend payouts. While Windstream's free cash flow payout ratio is high, it's not too far out of line with those of larger rivals AT&T and Verizon -- the free cash flow payout ratio for these three companies presently hold roughly 80%, 78%, and 61%, respectively. After its dividend cut, Frontier Communications now appears to boast the most defensible payout of the bunch, as its free cash flow payout ratio is more than 50% at present.

Windstream also has a humongous debt load of more than $8.8 billion, which could hinder progress and force it to slash shareholder distributions in the near future if it fails to find new avenues of post-landline growth. Frontier is already threatening Windstream in the rural telecom market thanks to its pending acquisition of AT&T's wireline business and its Connecticut-based fiber network for $2 billion. Morgan Stanley downgraded Windstream to a sell rating two months ago over concerns regarding the sustainability of its dividends.

Fool contributor Dan Caplinger notes that Windstream has high hopes in the cloud computing market, as it's opened several data centers in key strategic locations in the U.S. The company is now building a fourth enterprise-class data center in Charlotte to meet the surging customer demand. While Windstream and Frontier have faced difficulties convincing rural customers to sign up for high-speed Internet and video services, CenturyLink has done better at retaining its voice customers while boosting broadband and video subscriber counts. It will be interesting to see how Windstream tries to take on Frontier and CenturyLink in the enterprise-services business over the next few quarters.

Putting the pieces together

Today, Windstream has few of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.