Source: Buffalo Wild Wings.

Buffalo Wild Wings (BWLD +0.00%) stock fell by nearly 10% last week after the company's earnings report disappointed investors. However, this tasty restaurant chain is still generating mouthwatering growth rates, and it looks attractively valued in comparison to peers, be it fast-casual chains like Chipotle Mexican Grill (CMG 1.65%) and Panera Bread (PNRA +0.00%) or big established players like McDonald's (MCD +0.85%) and Yum! Brands (YUM 0.77%).

Is the recent dip in Buffalo Wild Wings a buying opportunity?

Hot and spicy wings

Sales during the fourth quarter of 2013 increased by 12.4% to $341.5 million. When adjusted by calendar effects, meaning 13 weeks in the fourth quarter of 2013 versus 14 weeks in 2012, sales grew by a remarkable 22% annually. Same-store sales increased 5.2% at company-owned restaurants and 3.1% at franchised locations, and Buffalo Wild Wings opened 53 additional company-owned and 49 franchised restaurants during the period.

Cost of sales and labor decreased as a percentage of revenues during the quarter. The company started selling wings by weight as opposed to by number last year, and this seems to be yielding good results in terms of cost management. Labor costs are expected to rise in the coming quarters as Buffalo Wild Wings continues expanding its Guest Experience Captains to more locations, but it's good to know that the company is proving its ability to keep labor expenses under control via efficient personnel management policies.

Earnings per share increased by 23.6% annually to $1.10 in the quarter. Excluding the 14th week in the fourth quarter of 2012, diluted earnings per share jumped by a remarkable 57.1% during the period.

Buffalo Wild Wings is still delivering growth rates that most other companies in the industry can only envy, and healthy demand indicates that the company has plenty of room for continued expansion in the coming years.

A fair price

The restaurant chain industry could be differentiated into two basic groups: the high-growth players in the fast-casual niche like Buffalo Wild Wings, Chipotle Mexican Grill, and Panera, or the more established and traditional global chains like McDonald's and Yum! Brands.

McDonald's is reporting stagnant performance lately, both in the U.S. and in international markets. Global comparable-store sales decreased by 0.1% in the fourth quarter of 2013 as market saturation and lack of successful menu innovations are generating serious difficulties for the company.

Yum! Brands is being hurt by flat sales in the U.S., but management is optimistic when it comes to international growth opportunities. Sales in China seem to be stabilizing after the negative impact from safety concerns regarding its KFC poultry suppliers, and the company expects an increase of at least 20% in earnings per share for 2014 versus 2013. When it comes to the U.S., however, there is no sign of a turnaround or accelerating growth rates for Yum! Brands.

Chipotle Mexican Grill is the undisputed growth leader in the fast-casual segment, and the company continues firing on all cylinders, with revenues increasing by 20.7% and comparable-restaurant sales jumping by a whopping 9.3% during the fourth quarter of 2013. The company trades at a considerable valuation premium to competitors, but Chipotle deserves a higher price tag because of its outstanding performance and superior growth prospects.

Panera has been slowing down in recent quarters: Total revenues grew 8% in the third quarter of 2013, and comparable-store sales increased by 1.7% during the period. This was not only lower than analysts' expectations, but also below the company's own guidance.

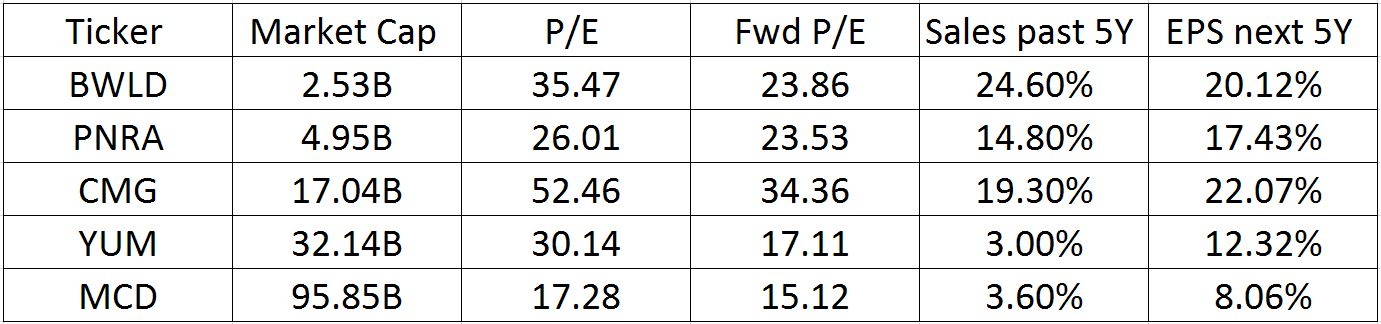

Data Source: FinViz.

When comparing valuation ratios like forward P/E, Buffalo Wild Wings and Panera trade at similar valuations, but Buffalo Wild Wings is generating superior performance and has a higher forecast growth rate for the next five years. As for Yum! Brands and McDonald's, they are materially cheaper than Buffalo Wild Wings, but they are no match when it comes to growth potential.

All in all, Buffalo Wild Wings seems fairly valued, if not a bit undervalued, when considering both valuation ratios and growth potential versus other companies in the business.

Bottom line

The stock market tends to overreact to earnings announcements in the short term, and that seems to be the case with Buffalo Wild Wings lately. The company is still generating compelling growth rates, and its valuation is quite reasonable in comparison to industry peers. This growing restaurant chain is well positioned to deliver delicious returns for investors in the coming years.