It's been a rough road of late for shares of Pandora Media (P +0.00%), with its shares down some 16% in the last month alone.

Some of the skepticism we've seen take hold of growth stocks in general has undoubtedly found its way into Pandora's shares as well. However, there's also good reason to think that something more rudimentary is also weighing on Pandora. Pandora's stock plunged some 8% last Tuesday when the streaming radio upstart released its April audience metrics, once again underlining that investors are beginning to question the growth story at Pandora specifically.

For those not already familiar, I'm something of a Pandora stalker as I

Source: Pandora

find its mix of pricey multiples, disruptive potential, and increasing competition, especially from tech giant Apple (AAPL +0.33%), make for a great case study in growth investing. The finance geek in me just can't get enough of this storyline. So keeping that in mind, let's look at Pandora's recent figures and one trend at Pandora that has me worried.

April showers

To be perfectly fair, Pandora's April audience metrics were a mixed bag. Some parts were encouraging, others alarming.

For the uninitiated, Pandora reports three user statistics in its monthly audience metrics reports: total listener hours streamed, its share of the overall U.S. radio market, and its monthly active users. In April, Pandora increased its number of listener hours streamed by an impressive 30% to a total of 1.31 billion hours in total. Pandora's share of the overall U.S. radio market (streaming and regular) reached 9.28%, up 7.3% from last April. And lastly, Pandora's monthly active users totaled 70.1 million strong in April, which was up 8% year-over-year.

The total hours listened figures stands out as the key bright spot for Pandora's April report. In fact, Pandora hasn't seen a bump in listener hours like that since last March. However, I'll contend that user growth is arguably more important to Pandora's overall long-term trajectory right now than total listener hours, and that's precisely what has me worried.

Has Pandora's user growth peaked?

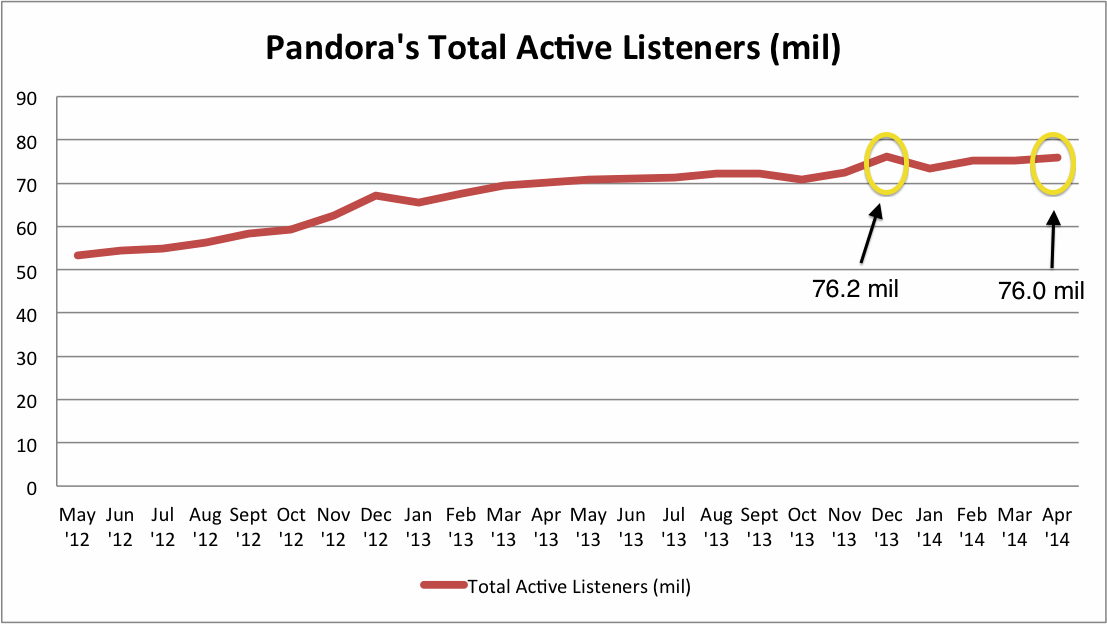

From its April audience report, we know Pandora grew its monthly active user base by 8% year-over-year, which for a growth stock of Pandora's caliber should arguably have alarm bells ringing to begin with. It's also worth noting that this marks the second consecutive single-digit year-over-year user growth we've seen from Pandora (8% in March as well). But when presented sequentially, the figures get downright scary.

For those keeping score at home, Pandora's total monthly active user April figure of 76 million remains 200,000 shy of its total user base from last December. That's right. Not only has Pandora not increased its user base in four months, it's actually lost users in aggregate since the end of last year. See for yourself.

Source: Pandora Media Investor Relations

This is really what it comes down to. In order for Pandora to truly fulfill its immense promise, it's imperative that Pandora continues to grow its active user base. Its user growth could (and will to some extent) continue to tick upward to some extent. But growing at 8% won't move the needle the way Pandora needs.

Pandora's growth equation is put under further pressure because of the lack of options it has in terms of geographic expansion. Right now, Pandora is almost entirely pigeon-holed in the U.S. market, meaning it will need to negotiate new international licensing deals with records labels. And in case you haven't noticed, Pandora and the record labels haven't historically been the best of friends. Further stacking the deck against Pandora's international odds is the fact that other scaled competitors like Spotify and Apple's iTunes Radio are already operating abroad, eliminating the first-mover advantage Pandora enjoyed in the U.S. streaming market.

And the recent tech story de jour, that of Apple's pending purchase of Beats, further reiterates Apple's plans to double down on streaming services with Apple's iOS 8 software update later this year. Apple casts a long shadow in any industry in which it operates, but between Apple's insanely large cash stockpile, its strong history within the music industry, and its ability to position its products wherever it likes on both smartphone and tablet software, Pandora investors should be shaking in their boots given Apple's renewed interested in this space.

Apple along could be a Pandora killer, but as I hope you see in a broader sense as well, there just aren't many easy short-term user growth drivers out there for Pandora today.

A moving target at Pandora

To be fair, Pandora will undoubtedly make more money on a per-user basis by pulling still-evolving monetization levers, like expanding its local advertising sales force, among others. You'll hear no argument from me on the monetization front.

It's also worth noting that Pandora is a current recommendation of two Motley Fool premium newsletters and favorite of our co-founder David Gardner. For the record, David is without question a more skilled investors than I, probably by several orders of magnitude. I can't hold a candle to David's success or track record.

However, as I at least believe the numbers bear out, Pandora will need to both increase its per-user ad profits and continue to increase its user base meaningfully in order to justify the $4.5 billion market cap it enjoys today.

Pandora's shares remain up over 200% since November 2012. With Pandora trading at 6.3x its LTM sales and a whopping 45x its 2015 estimated earnings, which I think you can fairly call into question as well, Pandora's share price pulling back lately certainly seems justified from where I'm sitting.

So I'm not saying Pandora is doomed at all here. Rather, I'm simply suggesting Pandora might not deserve the kind of premium the market's giving it today either.