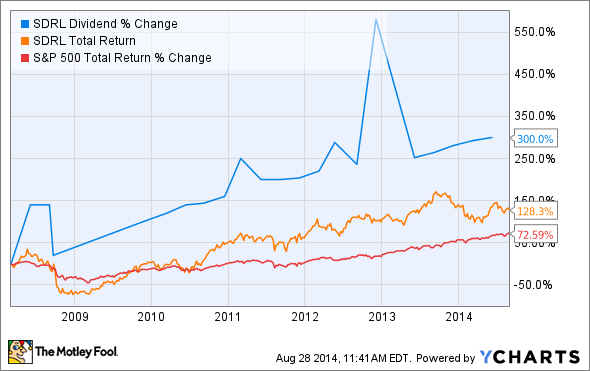

Income investors have long loved Seadrill (SDRL +0.00%) for its 11% yield and fast-growing dividend. The company's rapid fleet expansion has seen the company grow quickly and, combined with the dividend, has rewarded long-term investors with market-beating performance.

SDRL Dividend data by YCharts.

However, in the past few quarters, the offshore drilling industry has faced declining demand, as major oil companies pull back on spending. In addition, new rig supply has resulted in what Seadrill's management calls "fierce" competition for new ultra deep-water (UDW) rig contracts that resulted in the growth-happy company announcing it would no longer be ordering new rigs until market conditions improved. The announcement was made during the release of Seadrill's second-quarter earnings, which plunged 63% from a year ago.

What about the dividend?

For the quarter, Seadrill maintained its dividend at $1/share, and reiterated its commitment to this payout through 2016. However, with the current dividend costing the company $469 million/quarter, investors can be forgiven for worrying about the long-term sustainability of the dividend. This is especially true given the fact that in the past six months, Seadrill has paid out $938 million in dividends, yet cash flows from operations have only been $881 million. During this time, Seadrill spent $2.165 billion on expansion and debt servicing.

As I'll now explain, there are several reasons to be cautiously optimistic that Seadrill's dividend is safe, and that the company's long-term prospects remain bright.

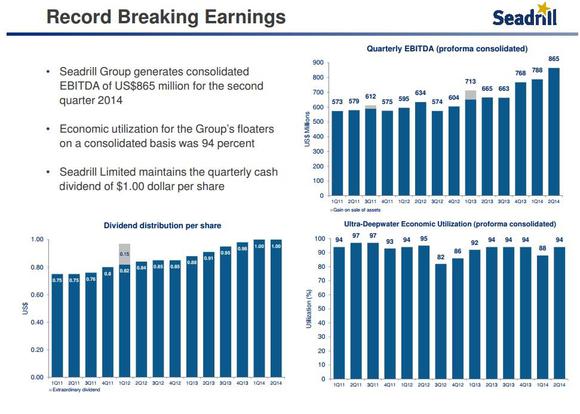

The bright side of earnings

Source: Seadrill Q2 Earnings Presentation, page 4.

As seen above, Seadrill's EBITDA, or earnings before interest, taxes, depreciation, and amortization, rose 30% and achieved a record high. Similarly its UDW fleet utilization remained high at 94%, and CEO Per Wullf stated that he expects this to increase to 98% for the third quarter.

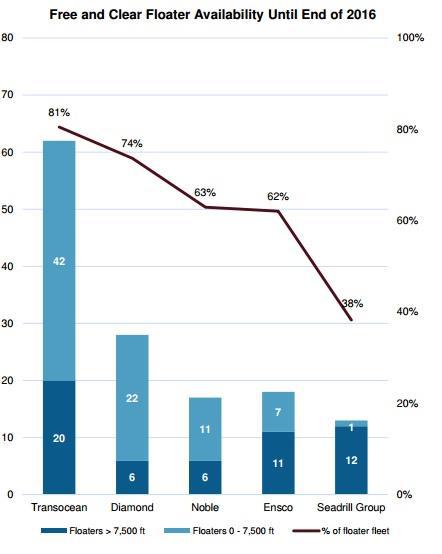

This high utilization is evidence that, though demand has softened, Seadrill's fleet of young, state-of-the-art ships remain in high demand through at least 2016, when analysts believe the market will improve, and can still command premium day rates. This puts Seadrill in a much better situation than competitors such as Transocean and Diamond Offshore Drilling, whose fleets are far older and face daunting contract cliffs in the years ahead.

Source: Seadrill Q2 Earnings Presentation, page 9.

The fact that Seadrill was able to secure new contracts for its West Saturn and West Jupiter UDW rigs at rates of $633,750 and $567,000 respectively, illustrates that the company's superior fleet has thus far been largely immune to the market weakness.

With a total contract backlog of $20 billion, Seadrill's dividend is in no immediate danger. As long as the company can continue securing similar rates for its 14 uncontracted new builds, management's confidence in the sustainability of the company's payout will prove correct.

Alternative financing further secures payout

Source: Seadrill Q2 Earnings Presentation, page 18.

During the second quarter, Seadrill sold 230 million shares of SapuraKencana for $300 million. As the above image shows, the company still has $1.21 billion in investments that it could tap should market conditions get worse.

In addition, Seadrill was able to raise $373 million from its MLP, Seadrill Partners, by selling it a 28% stake of Seadrill Operating LP.

Seadrill's other MLP, North Atlantic Drilling, of which Seadrill owns 70%, just won a $4.1 billion contract to provide five harsh environment rigs to Russian oil giant Rosneft starting in 2015. Growing distibutions and incentive distribution fees from its MLPs should help Seadrill secure its dividend during this period of temporary weakness.

Seadrill was also able to secure $2.85 billion in credit to refinance three rigs and finish building three others. This shows that the credit markets are still willing to offer the company ample and attractively priced debt to complete its aggressive growth expansion, while continuing to fund the generous dividend.

Risks to watch for

According to Per Wullf, the fact that oil has remained at $100/barrel for the last 3.5 years has been integral to his company's success. Oil's high price has been supported by the global economic recovery increasing demand, especially in nations such as China and India. A global recession could see oil prices plunge, which would turn the short-term weakness in the offshore market into a potentially much longer cyclical downturn. For Seadrill, a company with $12.2 billion in debt, such a situation would certainly put the dividend at risk.

Investors should watch for management to continue securing the balance sheet -- Seadrill's long-term debt decreased 7% this past quarter -- and watch to make sure the company can secure good day rates for its large number of upcoming new builds. This is especially true beginning in 2015, when Seadrill's management believes the market will begin to strengthen.

Foolish takeaway

The downturn in the offshore drilling market is expected to last another year or two. In the meantime, older rig operators are likely to face brutal downward pricing pressure, shorter contracts, and diminished cash flows. Thus far, Seadrill has largely avoided these problems, and its dividend remains secure. Patient long-term income investors who are willing to buy on the current weakness are likely to be rewarded with both a generous yield, and long-term market beating total returns.