Since topping out at almost $24 back in 2012, shares of Clean Energy Fuels Corp (CLNE 2.98%) have consistently and steadily declined. After some positive momentum at the end of last year that saw the stock price creep close to $14, shares have again fallen below $10 recently, and are down 23% since the beginning of 2014.

What gives? Is Clean Energy Fuels doomed to remain an underperforming stock, or is there more to the story?

The stock's performance has been simply horrible during the past couple of years, but there has been substantial improvement in the business that's easy to miss if you don't know what to look for. Let's take a closer look.

What's the business story?

Source: Clean Energy Fuels.

There are more than 200 million cars in the U.S., and they consume more than 150 billion gallons of gasoline. This is a huge market, but it's a market that natural gas has basically not broken into in the U.S. -- and may never to any large extent -- because of the limited availability and cost of NG cars, and the limited access to natural gas for vehicles.

The diesel market, however, is a different story. Heavy trucking is an ideal target for natural gas because these vehicles can consume more than 20,000 gallons annually, which makes a fuel that's 20% or 30% cheaper very appealing.

Shipping companies operate with very thin profit margins. Take Berkshire Hathaway subsidiary McLane: It generated only $486 million in net income last year -- that's barely more than 1% -- on $45 billion in total revenue. For shippers, the opportunity to reduce fuel costs by 20% is very appealing.

This is the market Clean Energy Fuels is targeting, as well as its core business of buses and other public transit, solid waste, and municipal fleets.

The story behind the debt, and what the future looks like

We're talking about more than $600 million in debt at high interest rates -- most of which is convertible to stock, meaning impending dilution for shareholders in future years -- and a cash stockpile that's having to meet the shortfall between cash from operations and expenses. Sounds pretty horrible, right? When you peel back the layers, and understand what all that debt is about, and why costs aren't (yet) being met by cash flows, things really aren't as terrible as they seem. First, let's take a look at the debt, and where it originated.

In 2011, Clean Energy Fuels announced its "America's Natural Gas Highway," or ANGH, initiative, and in 2012, announced its partnership with Pilot Flying J truck stops to co-locate 150 natural gas refueling stations at its truck stops. Pilot Flying J operates more than 550 locations, making it the largest truck stop operator and seller of diesel in the U.S., selling nearly as much fuel as No. 2 and No. 3, Love's and TravelCenters of America, combined.

Essentially all of the current debt, largely held in convertible notes that come due between 2016 and 2020, has funded ANGH expansion. To date, Clean Energy Fuels has constructed more than 90 of the stations, though only about 30 have been opened. The fact that so many of these stations, built in 2012 and 2013, have yet to open, is the big issue.

Sales of the Cummins Westport engines for trucking are more than 20% ahead of last year's pace.

The reality is, the stations were built largely on expectations that engine maker Cummins' (CMI 1.81%) and Westport Innovations' (WPRT 8.08%) joint venture would be coming to market with a 12 liter natural gas engine in 2012. The short version is, this engine came to market nearly one year later than anticipated, and Clean Energy was well ahead of the rollout of trucks. And, while there are clear advantages to having so many stations ready to go, and located at the busiest truck stops, it's a double-edged sword because of the debt expense and fixed costs tied to the asset base.

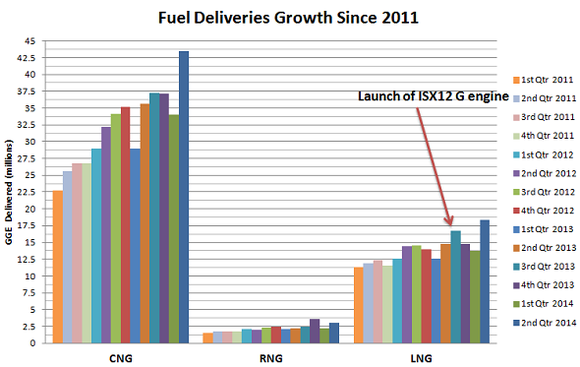

But there's some good news. Since the Cummins Westport 12 liter engine came to market last year, growth in gallons delivered has begun to accelerate:

Data source: Clean Energy SEC Filings.

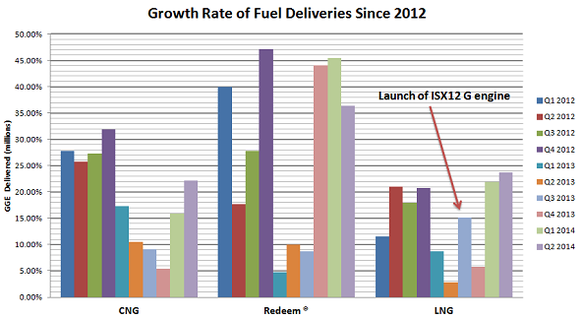

Percentage of growth is also accelerating:

Data source: Clean Energy SEC Filings.

With more than 90 of the planned 150 stations already built, and around 60 ready to open, management has stated that capex spend going forward should be much lower than the past couple of years. Further, as these stations open, they won't really increase fixed costs above current levels, but will add substantially to the bottom line. We'll discuss that in the next section.

Cash, convertible notes, and a sustainable business

The business is not sustainable at current fuel sales levels -- that's pretty clear -- but the business is built for growth, and that growth is happening. Clean Energy has about $276 million in cash and short-term investments (bonds), and announced that its capex spend for the year would be reduced from $135 million to less than $85 million as the focus shifts to opening stations already built.

SG&A expense has fallen a little in 2014, meaning that new stations being opened -- 27 so far in 2014 -- add almost no administrative expense. Further, the increase in depreciation and amortization makes sense, because as new stations are brought online, they will be depreciated over their usable life. It's also important to note that this is accounting value, and not necessarily a cash impact on the business. What does this matter? Just because D&A increases, it doesn't mean there's a material impact on the company's financial position. Combined, these all point to the company finishing the year with a substantial remaining cash cushion, and improving results further reducing net cash outflows. As the chart below shows, much of the shortfall to free cash flow is attributable to capex:

CLNE Capital Expenditures (TTM) data by YCharts.

The fix for that is slowing the rate of station construction, and opening stations to increasing fuel deliveries.

According to management, each gallon of fuel sold nets around $0.30 in margin. Based on a 20% growth rate -- within historical averages and below recent results -- the company will be both adjusted EBITDA positive and operating cash flow positive by 2016, adding somewhere around $30 million in profit dollars based on 20% sales growth. Ramp the growth rate to 25%, roughly what we've seen in 2014, and you're talking about adding nearly $40 million in profit dollars in 2016 compared to today's levels.

These metrics will matter a lot to investors holding those convertible notes. Think about it this way: Today's quarterly debt expense is around $40 million per year, and the first $150 million tranche comes due in 2016. This tranche costs about $11 million per year based on the 7.5% interest rate. These notes could be converted to shares at $15 per share -- a substantial premium to today's share price -- so how does the company cover this $150 million shortfall if shares aren't trading higher than $15 in two years?

If the growth I've outlined above does happen -- remember it's based on realistic, historically supported trends -- it's not hard to imagine that the company will be able to find a partner willing to provide it with capital, and probably at better terms than the current notes. Based on the reduced capex and increasing fuel sales numbers, it could easily roll into those 2016 maturities with $100 million in cash on hand and a consistently improving cash flow position.

Don't let fear and greed take the reins

One look at the headlines during the past year can paint a scary picture for Clean Energy, but a little digging into the business results and trends shows a different story. If you're going to invest in Clean Energy Fuels, as I have, don't get too caught up in the headlines, especially when there isn't any material information to support negative claims.

Take Warren Buffett's approach: Focus on the business results instead. You'll rest easier, better understand the companies you own, and be less likely to buy or sell on bad information.