Image of Coke cup on a rail by Leo Hidalgo under Creative Commons license.

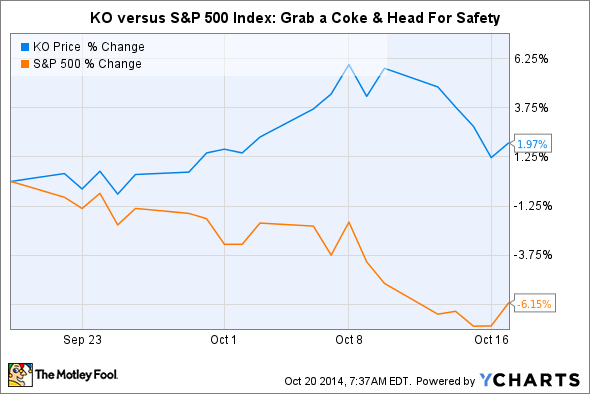

During the last four weeks, the stock market decided to forgive all of The Coca-Cola Company's (KO 0.64%) recent sins. As the S&P 500 index declined by more than 6%, and volatility returned from a prolonged vacation, investors suddenly remembered the affection they had for a cash flow titan with the most recognized brand on earth, and a dividend yield approaching 3%. Coke stock not only held its ground, but managed to gain a couple of percentage points, reversing its trend of lagging the S&P for most of 2014. The divergence is pronounced:

This week, investors will return to reality after Coca-Cola releases earnings on Tuesday before the market open. Will the company's third quarter of 2014 give buyers a reason to continue to flock to its shares? Or will attention refocus on the hindrances to Coke's stock price over the last two years? Below are three key issues which will help to decide sentiment either way.

Will Coke buck its net revenue trend?

As I discussed in a recent article, Coca-Cola's top-line has stalled in recent years, and this is one of the most vexing problems the company faces. After peaking in 2012 at $48 billion, annual revenue has declined more than $1 billion -- the company recorded $46.9 billion on its books in 2013. During the first two quarters of this year, Coca-Cola's revenue of $23.2 billion represents a decline of 2.7% versus the prior year.

In the third quarter of 2013, Coke's revenue came in at $12.0 billion, and investors will be looking for at least this number on the top line. The company should have a decent chance of hitting this mark, as its summer "Share A Coke" campaign, in which consumers could purchase personalized Coke bottles, was apparently quite successful. According to the Wall Street Journal, during June, July, and August of this year, the promotion spurred a 0.4% rise in U.S. soft drink volumes -- the first time in eleven years volumes didn't decline.

Cash flow under scrutiny

If Coca-Cola does manage to break its trend of shrinking revenue, it will do so on the strength of an increased marketing spend. Earlier this year, management announced its goal to increase Coca-Cola's marketing budget by $1 billion between now and 2016. Yet higher marketing expenditures to stabilize soft drink sales, coupled with margin pressure from other sources including currency headwinds (discussed below), may put a squeeze on Coke's tremendous cash flow.

During the first half of 2014, Coke's operating cash flow increased handily versus the prior year, from $4.0 to $4.5 billion. However, this was largely propelled by working capital changes of $580 million. Investors will be watching this period's operating cash flow for any signs of deterioration. Some mild retracement is to be expected over the next few quarters, as Coke invests in stabilizing sweetened carbonated beverages such as brand Coke and brand Diet Coke. But any significant tailing off will be an early clue that the task of propping up these "sparkling" beverages won't be easy or quick.

Will the strong dollar undermine Coke's profits?

There are few companies in existence which can claim as wide a footprint as Coca-Cola, which sells its products through a distribution network that spans more than 200 countries. Yet this competitive advantage has also become something of a weight on the company's recent results.

Much of the revenue decline discussed above can be traced back to a trend of currency depreciation against the U.S. dollar in the various countries in which Coke does business. Take the first half of this year for example: on a GAAP (Generally Accepted Accounting Principles) basis, Coke's revenue declined by nearly 3%. But on a currency neutral basis, that is, if you remove the effects of currency fluctuations when converting Coke's sales back to dollars, revenue was actually flat.

For the long-term investor, it's important to invest in companies which show revenue and profit increases after all currency effects are accounted for. This is a goal that Coke may struggle with in the near term. The company has already recorded a negative impact of $268 million on income before taxes through June of this year, due to Venezuelan currency devaluation. Other countries whose currencies are losing ground quickly against the dollar, and which could pressure Coke's profit and loss statement, include Argentina and Russia.

Coke billboard in Khabarovsk, Russia. Image by Sharon Hahn Darlin under Creative Commons license.

Coke has a bit of a built-in buffer against currency slippage, in that it still derives about 46% of revenue from North America, primarily designated in U.S. dollars. Arch rival Pepsi, which has a similarly global business, and also has a revenue concentration in North America, recently reported third quarter results that beat expectations. Nevertheless, don't be surprised if Coca-Cola's management blames currency woes for its results: the U.S. dollar gained nearly 7.75% against a basket of other major currencies during the three months Coke will report on tomorrow.

A final note: one phenomenon that could trump all the earnings factors above would be a jump in the sales of non-sparkling, or "still" beverages. These are the bottled waters, juices, energy drinks, coffees, and teas that Coke has ramped up in recent years to stem losses from its carbonated beverages. I recently discussed the potential of these drinks in Coke's massive portfolio here. This side of Coke's business represents its best growth opportunity. Any positive surprises in still beverages will give investors a reason to continue the love they've shown for these shares over the last month.