The S&P 500 has more than tripled in value since early 2009.

It's one of the best five-year periods in market history, roughly matching the 1995-2000 bull market that created one of the largest bubbles ever.

What's that mean for market values today?

Depends who you ask.

James Paulsen, chief investment strategist at Wells Capital Management, noted last week that the median S&P 500 company now trades at the highest price-to-earnings ratio since his records began in 1950.

The only reason the market as a whole doesn't look as overvalued as the median component is because some of the S&P 500's largest companies that carry the most weight in the index, like ExxonMobil (XOM 0.51%) and Apple (AAPL 0.75%), are still fairly cheap.

The median company is also near a record high measured on price-to-book value and price-to-cash flow.

These are eye-opening statistics that show how much the rally of the last five years may have borrowed from future returns.

But then again...

There are all kinds of ways to value the market. None is necessarily right or wrong, because what matters -- what moves markets -- is whatever investors care about at a given moment.

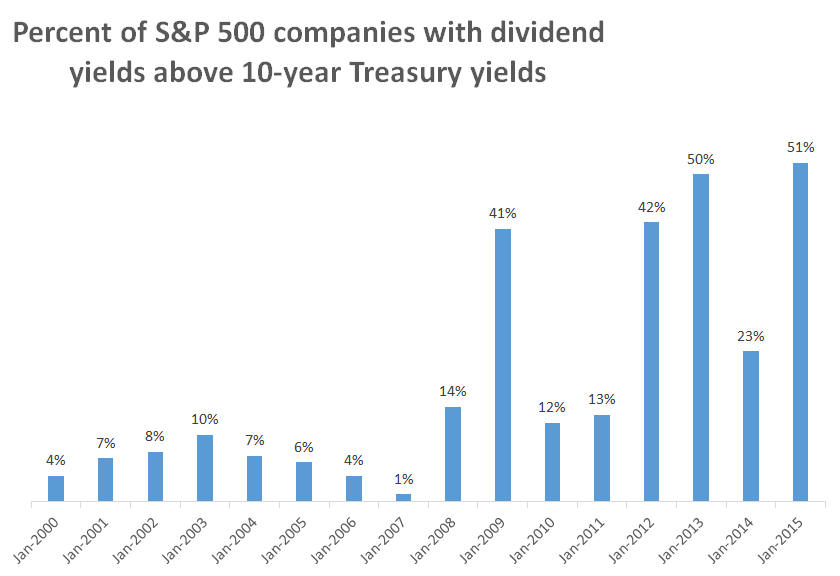

And what do people care about right now? Dividends, for one.

With interest rates at rock-bottom levels, dividends have become wildly popular as one of the last remaining places you can earn a yield above the rate of inflation. They became viewed as bond substitutes for income-starved investors. Boring, low-growth sectors that emphasize dividends, like utilities, trade at a higher valuation than high-growth technology stocks. The clamor for dividends in the last five years has been insatiable.

Two things happened recently to help that trend:

- Interest rates on Treasury bonds have plunged. Ten-year Treasuries now yield 1.8%, from 2.9% a year ago.

- Dividend payouts have surged. The S&P 500 is up 72% since 2010, but S&P 500 dividends are up 84%.

Source: S&P Capital IQ, Federal Reserve.

- Why markets must always crash

- What I plan to do when the market crashes

- Some things to remember about market plunges

More from The Motley Fool: Where Are The Customers' Yachts?