Image Source: Chevron Australia corporate website

Sometimes, even strong companies will put up a real stinker of a performance, and Chevron's (CVX 1.02%) 2015 performance was one of those. Oil's continued slide, coupled with a large spending budget, has put Chevron in a position that some are wondering whether the company will be able to keep its dividend aristocrat status.

At the same time, the expectations for Chevron are pretty low, so some slightly better-than-expected results with some oil-price relief could potentially translate into a stellar year for Chevron investors. To see if a great 2016 is in the cards, let's take a look at what Chevron needs to do to improve its chances for a great 2016 and what suggests it could see much brighter days ahead.

A little oil-price discipline goes a long way

It doesn't take much of a market genius to realize that Chevron's shares are going to sway with oil prices. Even as an integrated oil and gas company, it it still more closely tied to the actual production side of the business than peers such as ExxonMobil (XOM 1.51%) or Royal Dutch Shell (NYSE: RDS-A) (NYSE: RDS-B). It's no surprise, then, that shares of Chevron have taken such a hard hit over the past 18 months.

Even though Chevron's results will sway with prices, one thing that it and all other oil and gas producers can do to mitigate huge losses is to (1) keep costs as low as possible, and (2) be conservative on price outlooks when making new investment decisions. No one would probably have faulted Chevron for having a long-term oil price of $70 per barrel. It was still on the higher side of what other integrated majors were anticipating

| Company | Brent Oil Price Assumption for Production Outlook |

|---|---|

| Chevron | $70 |

| BP | $60 (was $80 until last quarter) |

| ExxonMobil | $55 |

| Royal Dutch Shell | $70 |

| Total SA | $60 (may revise down to $45) |

With close to 100 years under its belt, this isn't the first oil price decline Chevton has seen, and chances are this oil downturn isn't the last one it will deal with. To get in better shape for the rest of 2016 and beyond, though, it's in the company's best interest to make more conservative assumptions about the future price of oil. That would go a long way in helping the company get out of the rut it finds itself in today.

Building the foundation

That all being said, there are some reasons to think that things are going to start to get better for Chevron. For the past couple of years the company has been spending on capital projects at a higher rate than its peers based on the company's size. Two of these projects, Gorgon and Wheatstone LNG, have eaten up tens of billions in capital over the past several years. So while companies such as ExxonMobil and Shell have been able to wind down spending as a large portion of new projects have come online in recent months, Chevron is still shelling out huge chunks of cash in relation to its operational cash flows.

| Company | Operational Cash Flow As a Percentage of Capital Expenditures |

|---|---|

| Chevron | 67% |

| BP | 98% |

| ExxonMobil | 127% |

| Royal Dutch Shell | 139% |

| Total | 79% |

Source: S&P Capital IQ

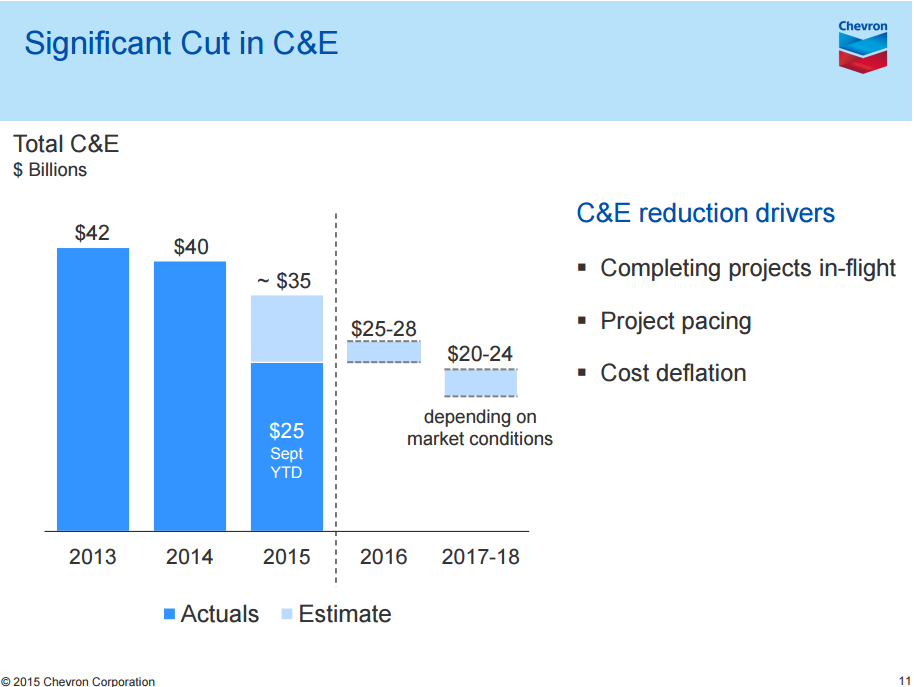

With many of these projects starting to wind down, though, Chevron is now in a position that it can drastically cut spending. By 2018, management expects to be spending $9 billion to $15 billion less between now and 2017.

Image source: Chevron investor presentation.

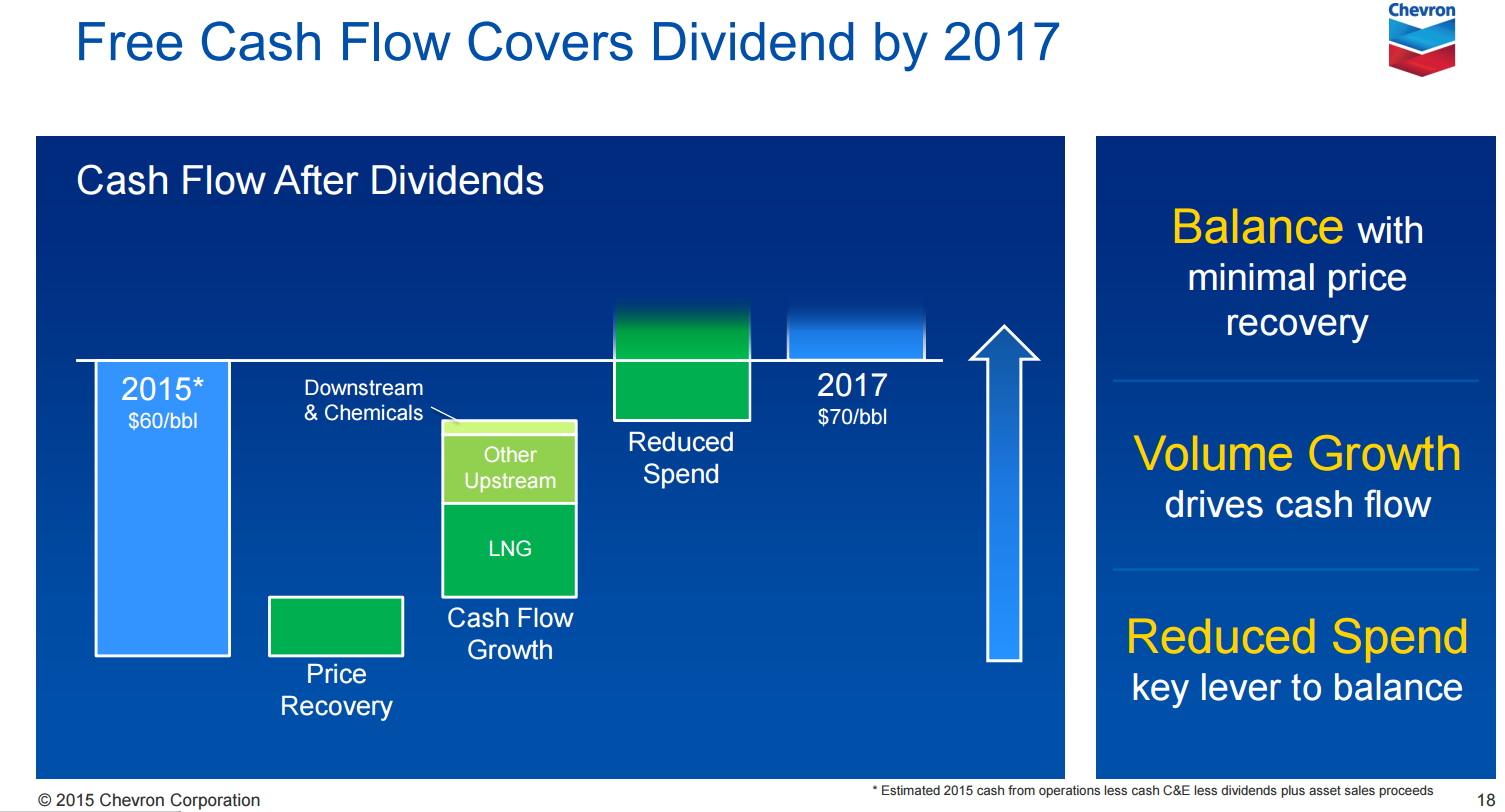

The other thing to keep in mind is that many of these projects that are eating into cash flow will start to generate some cash. Bringing Gorgon and Wheatstone online is expected to increase cash from operations by a significant amount since about 80% of its production capacity is subscribed under attractive long-term supply contracts. With a few other projects turning from cash consumers to cash producers over that time frame, it could really help close the gap on its cash spending deficit.

Source: Chevron investor presentation.

What a Fool believes

Unlike many of its peers that have been able to drastically scale back spending needs. Chevron needs another year of elevated spending levels to complete its suite of projects. This means that 2016 may not be the company's time to shine. Beyond that, though, Chevron could be in much better shape. The completion of both Gorgon and Wheastone LNG projects will turn a lot of unproductive working capital into cash generating assets under long-term contracts.

If we were to see oil and gas prices start to rise as we head into 2017, then Chevron might look at lot better than it does today.