An IRA is an investment account that provides tax breaks for retirement savings. Investing money in an IRA is one of the best ways to prepare for your later years because anyone with earned income can open one -- even those without access to an employer-sponsored retirement plan.

However, before contributing to an IRA, you should understand which type is right for your situation, and you should learn the rules governing deductible contributions and penalty-free withdrawals.

What is an IRA?

IRA stands for individual retirement account. There are several types, but each allows you to make tax-advantaged contributions from income you earn to build a nest egg for retirement.

The different kinds of IRAs have different contribution limits, and some also impose income limits on contributors. For example, the two most commonly used IRAs -- traditional and Roth -- have an aggregate contribution limit of $7,000 in 2025 and $7,500 in 2026, although those 50 or older can make an additional catch-up contribution annually. They can contribute a maximum of $8,000 in 2025 and $8,600 in 2026.

You can open an IRA with any financial institution, including:

- Discount online brokers

- Traditional banks

- Robo-advisors

- Investment management firms

Once you’ve made a contribution, you can purchase any assets your brokerage allows, including stocks, bonds, and mutual funds.

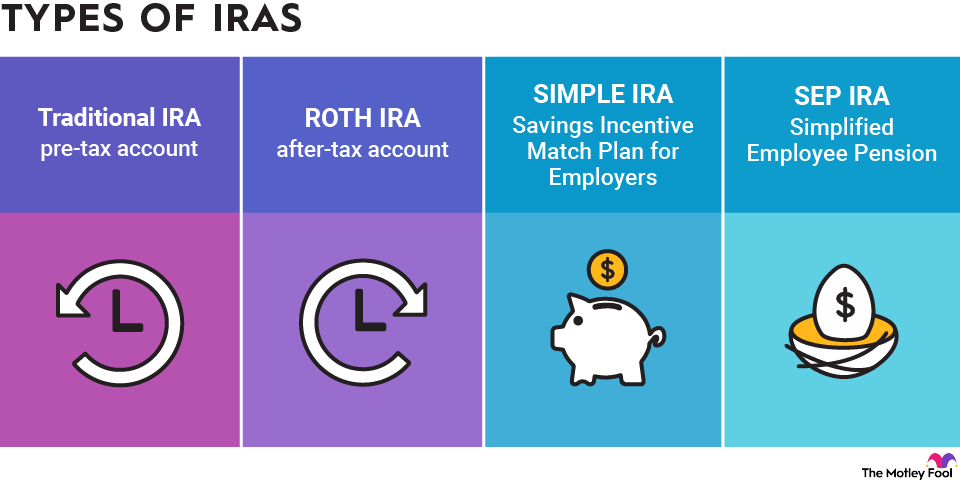

Types of IRAs

There are several kinds of IRAs available, and they all work a little differently. Some common types of IRAs are:

Traditional IRAs

Traditional IRAs allow you to invest pretax income toward your retirement. These contributions grow tax-deferred until you withdraw them, and they can be tax-deductible, too. While anyone can contribute to this type of IRA (regardless of income), there are some restrictions.

You can deduct up to $7,000 in 2025 or $7,500 in 2026. Those 50 and older can save up to $8,000 and $8,600, respectively, in 2025 and 2026. These are the maximum amounts you can contribute for the year between both traditional and Roth IRAs. Contributions are also fully tax-deductible if neither you nor your spouse has a workplace retirement plan.

Your eligibility to deduct contributions begins to phase out at the following income levels in 2025:

- $79,000 for single filers

- $126,000 for a married joint filer with a workplace plan

- $236,000 for a married joint filer whose spouse has a workplace plan

Your eligibility to deduct contributions begins to phase out at the following income levels in 2026:

- $81,000 for single filers

- $129,000 for a married joint filer with a workplace plan

- $242,000 for a married joint filer whose spouse has a workplace plan

A traditional IRA has many benefits and can be an ideal choice if you feel that your tax bracket is likely to be lower in retirement than it currently is. If you expect your tax rate to drop, it makes sense to claim your tax benefits up front when they are worth more and to pay taxes on distributions at your ordinary income tax rate later when your rate is lower.

Roth IRAs

The main difference between a traditional IRA and a Roth IRA is that you make contributions to a Roth IRA with after-tax dollars. While contributions aren’t deductible in the year they’re made, this money grows tax-free, and you don't owe taxes on withdrawals in retirement. Roth IRAs are also subject to the same aggregate contribution limit as traditional IRAs: $7,000 in 2025 and $7,500 in 2026, or $8,000 in 2025 and $8,600 in 2026 if you're 50 or older. Unlike traditional IRAs, Roth IRAs have income limits on who can contribute.

If you expect your tax rate to increase in retirement, a Roth IRA is a good choice. That's because you will be able to make tax-free withdrawals later on when your money would otherwise be taxed at a higher rate.

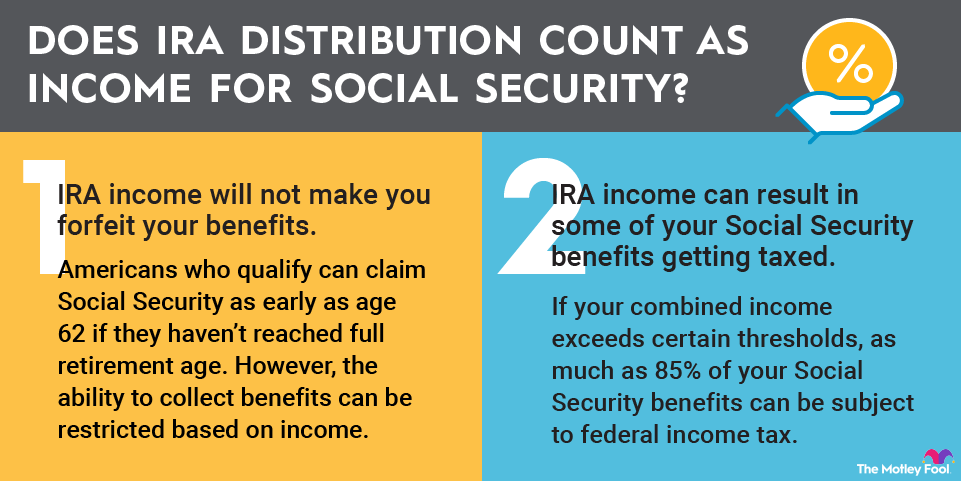

If you are worried about crossing the income threshold where Social Security benefits become taxable, then a Roth IRA can also be a good idea. That's because the IRS doesn't count distributions from a Roth IRA when determining if your Social Security is taxable.

SEP IRAs

Small business owners and self-employed individuals can set up Simplified Employee Pension IRAs, or SEP-IRAs. Only employers and the self-employed can make contributions to this type of account.

The annual contribution limit is the lesser of 25% of employee compensation, or $70,000 in 2025 and $72,000 in 2026. There are no income limits for contributing to a SEP-IRA. You deduct your contributions in the year you make them.

SEP-IRAs are a good choice for self-employed workers or small-business owners who want to contribute the maximum amount of money to their retirement account. However, you must contribute the same percentage to all eligible employees who participate. If you have a large staff, you could be required to contribute a significant amount to their retirement accounts if you want to maximize your own retirement contributions.

SIMPLE IRAs

Just as with SEP-IRAs, employers and the self-employed can set up SIMPLE IRAs, but both employers and employees can contribute to this type of account. Employees may contribute up to $16,500 in 2025 and $17,000 in 2025. Some workers are eligible for an increased elective deferral limit, which allows contributions of up to $17,600 in 2025 or $18,100 in 2026.

Workers 50 and older in the smallest SIMPLE IRA plans (25 or fewer employees) have a special catch-up contribution limit of $3,850 for 2025 and 2026. Larger SIMPLE IRA plans (26 to 100 employees) permit catch-up contributions of $3,500 in 2025 and $4,000 in 2026 for those 50 and older. Employees aged 60 to 63 in all SIMPLE IRA plans may make catch-up contributions of up to $5,250 in both years.

There are no income limits for contributions to this type of account.

This account may have lower contribution limits than the SEP-IRA, but you have more flexibility in structuring contributions to employees.

Rollover IRAs

A rollover IRA is a type of IRA that allows you to transfer money from another retirement account. For example, if you leave a job and you had a 401(k) at your workplace, you can move the money from your 401(k) into a rollover IRA.

You do not need to open a specific "rollover IRA" in order to move your money from your existing retirement account. You can transfer your funds into any existing IRA that you already have. However, rolling over money can sometimes have tax consequences.

If you do not want to owe taxes, move your money into the same type of account that you currently have. For example, you can roll over a traditional 401(k) into a traditional IRA or a Roth 401(k) into a Roth IRA.

Spousal IRAs

A spousal IRA is a regular IRA that you fund on behalf of a spouse who has little or no earned income. You can use either a traditional or Roth IRA to save for a non-employed spouse. The contribution limit is the same as it is for a traditional and Roth IRA that you would open for yourself -- $7,000 in 2025 and $7,500 in 2025, plus an additional $1,000 in catch-up contributions for those who are 50 and older ($1,100 in 2026).

If you or your spouse does not have enough earned income to contribute to your own IRA, a spousal IRA can be an ideal choice.

Advantages of IRAs

IRAs have several advantages, such as:

- You have a choice of investment accounts: You can decide between traditional and Roth IRAs, depending on whether you would prefer your tax break upfront during the year you contribute or would prefer to defer your tax savings until you are a retiree. You also have the choice to contribute to accounts that provide higher contribution limits if you are self-employed or own your own business.

- Contributions provide significant tax advantages: Traditional IRAs allow you to contribute to your account with pretax dollars, while Roth IRAs allow you to benefit from tax-free withdrawals in retirement. You can choose whether to save on taxes now or in your later years.

- You do not need an employer to open an IRA for you: Although there are a few types of IRAs that employers can offer for employees, you can set up the most common IRA account types (traditional and Roth) for yourself. You have the option to use an IRA as a supplement to a workplace savings plan, or you can open one to take advantage of tax breaks for retirement savings if your employer doesn’t offer a 401(k) or similar plan type.

- Opening an IRA is simple. If you are a self-employed worker or own your own business, SEP and SIMPLE IRAs can be easier to establish than other types of workplace retirement plans, such as a 401(k).

- You have more flexibility in investment options: You can choose from a wide variety of financial institutions to hold your IRA, including brokerage accounts, robo-advisors, banks, and self-directed IRAs. These types of accounts also usually offer several different investments to choose from, so you can invest your money in a wider variety of assets than would be available in a typical workplace 401(k) plan.

- Most institutions allow you to open an IRA with no fees and no minimum balance: Many brokers and banks make it easy to get started investing, with few or no costs associated with opening or maintaining your account.

- You can borrow from your account. This is an option as long as you follow the rules about borrowing from your IRA.

Explore Related Retirement Topics

IRA FAQs

About the Author