Wake up to the latest market news, company insights, and a bit of Foolish fun -- all wrapped up in one quick, easy-to-read email, called Breakfast News. Delivered at 7:30 a.m. ET every single market day. See an example of our weekday Breakfast News email & sign-up below.

Loading image...

Loading raw_html...

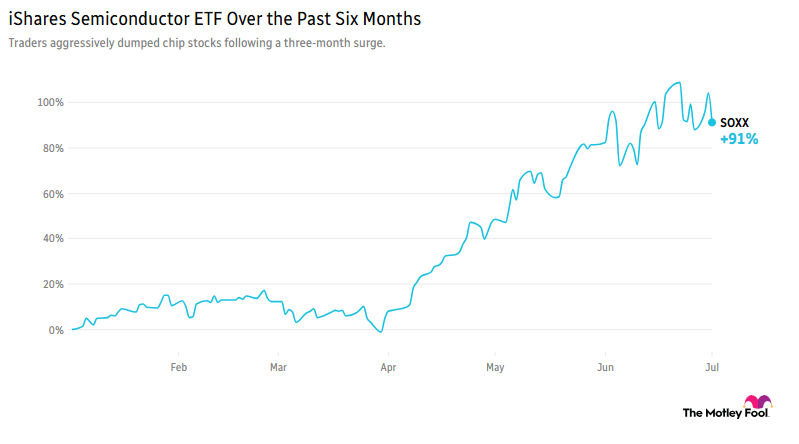

1) Chip Sell-Off Drags Tech Stocks Into Third Quarter

Loading paragraph...

2) Sell-Offs Are the Toll, Not the Trap

Loading paragraph...

3) Amazon's End-to-End Silicon Plans

Loading paragraph...

4) SpaceX Isn't the Only Summer IPO…

Loading paragraph...

Loading raw_html...

Loading paragraph...

6) Today's Take: The View From the Top

Loading paragraph...

7) Your Take

Loading paragraph...

![fedfunds-jun26-nochange[1]](https://g.foolcdn.com/image/?url=https%3A%2F%2Fg.foolcdn.com%2Feditorial%2Fimages%2F875175%2Ffedfunds-jun26-nochange1.png&w=384&op=resize)