Wake up to the latest market news, company insights, and a bit of Foolish fun -- all wrapped up in one quick, easy-to-read email, called Breakfast News. Delivered at 7:30 a.m. ET every single market day. See an example of our weekday Breakfast News email & sign-up below.

Loading image...

Loading raw_html...

1) No Buyers at The Trade Desk

Loading paragraph...

Loading raw_html...

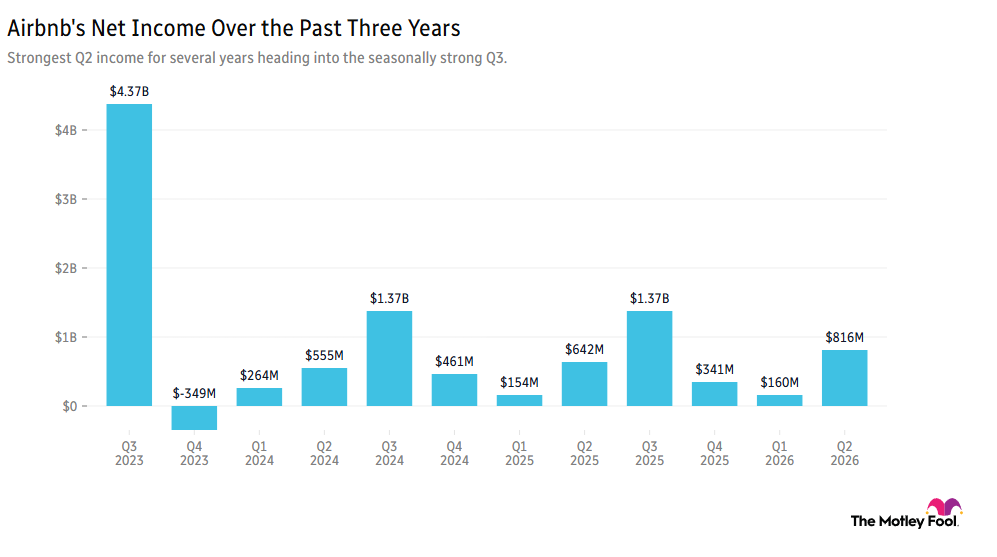

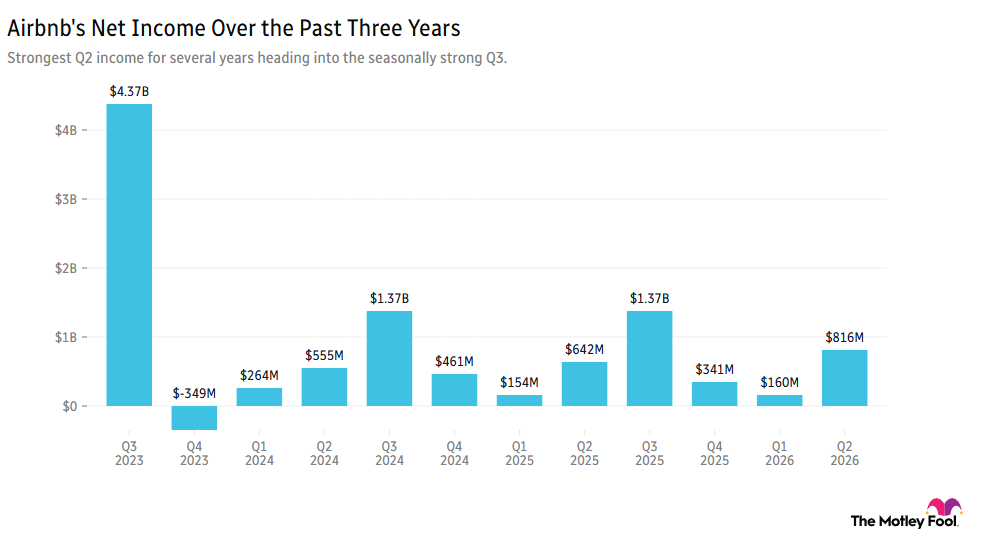

2) Gen Z Is Powering Airbnb's Fastest Growth in Years

Loading paragraph...

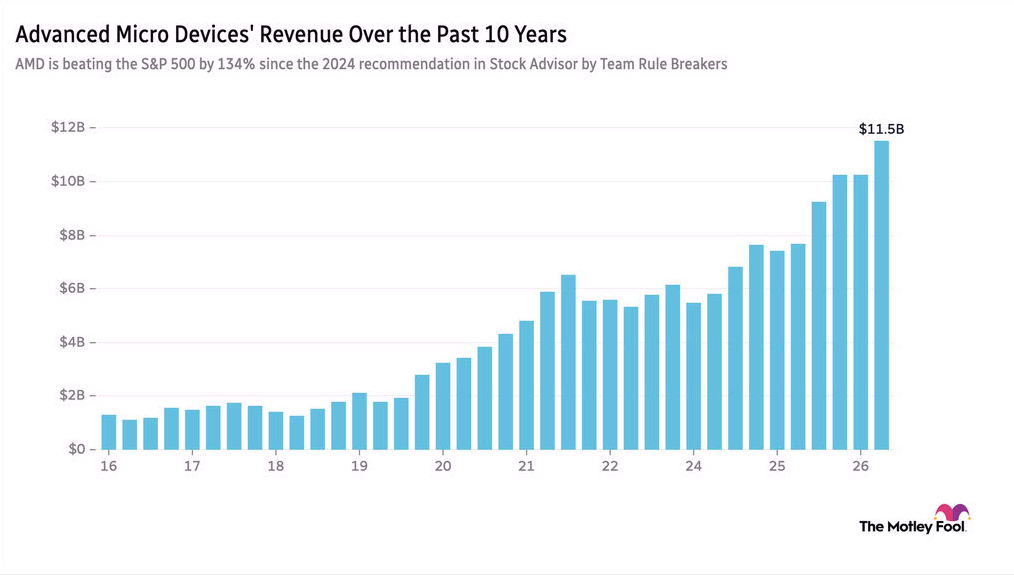

3) AMD Joins Nvidia in Hardwiring AI Into Silicon

Loading paragraph...

4) Cloudflare, Twilio, and Atlassian Rally on Broadening Demand

Loading paragraph...

5) Don't Price in Tesla's $119 Billion Terafab Yet

Loading paragraph...

6) Today's Take: How Much Tech Is Too Much Tech?

Loading paragraph...

7) Your Take

Loading paragraph...