Wake up to the latest market news, company insights, and a bit of Foolish fun -- all wrapped up in one quick, easy-to-read email, called Breakfast News. Delivered at 7:30 a.m. ET every single market day. See an example of our weekday Breakfast News email & sign-up below.

Loading image...

Loading raw_html...

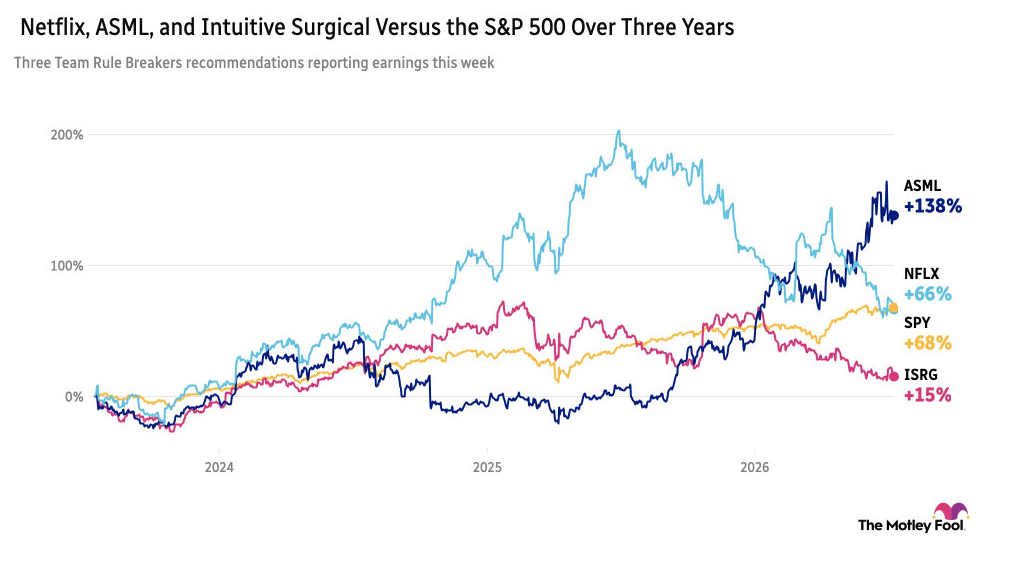

1) Netflix Heads Up the Week's Team Rule Breakers Earnings

Loading paragraph...

2) Selected Q2 Earnings from Team Hidden Gems Recs

Loading paragraph...

3) Markets Uncertain as Inflation Looms

Loading paragraph...

4) Today's Take: The Risk You Never Noticed

Loading paragraph...

5) Your Take

Which company's earnings are you most interested in following this quarter, and why?

Share with friends and family, or become a member to hear what your fellow Fools are saying!

![fedfunds-jun26-nochange[1]](https://g.foolcdn.com/image/?url=https%3A%2F%2Fg.foolcdn.com%2Feditorial%2Fimages%2F875175%2Ffedfunds-jun26-nochange1.png&w=384&op=resize)