Wake up to the latest market news, company insights, and a bit of Foolish fun -- all wrapped up in one quick, easy-to-read email, called Breakfast News. Delivered at 7:30 a.m. ET every single market day. See an example of our weekday Breakfast News email & sign-up below.

Loading image...

Loading raw_html...

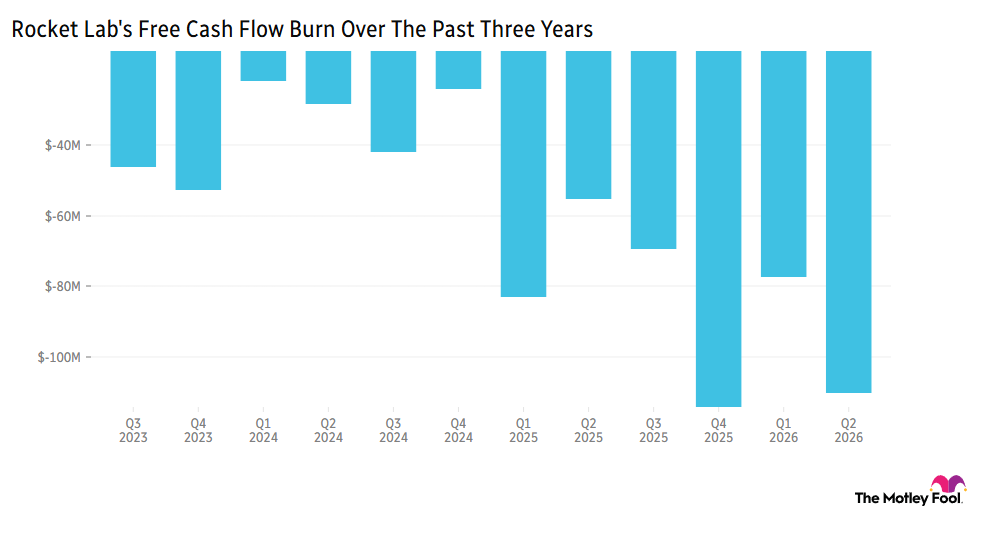

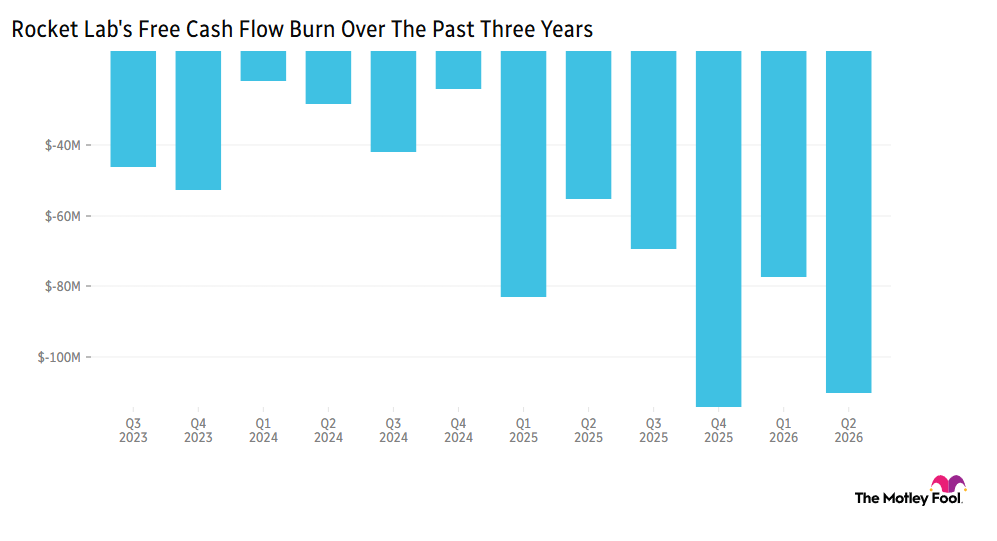

1) Rocket Lab: Up on Paper, Down 7%

Loading raw_html...

Loading paragraph...

2) BridgeBio Stalls, While Hims and On Fall Despite Good Quarters

Loading paragraph...

3) Who Lists First Sets the AI Price

Loading paragraph...

4) CrowdStrike and Palo Alto Jump 5% as AI Threats Grow

Loading paragraph...

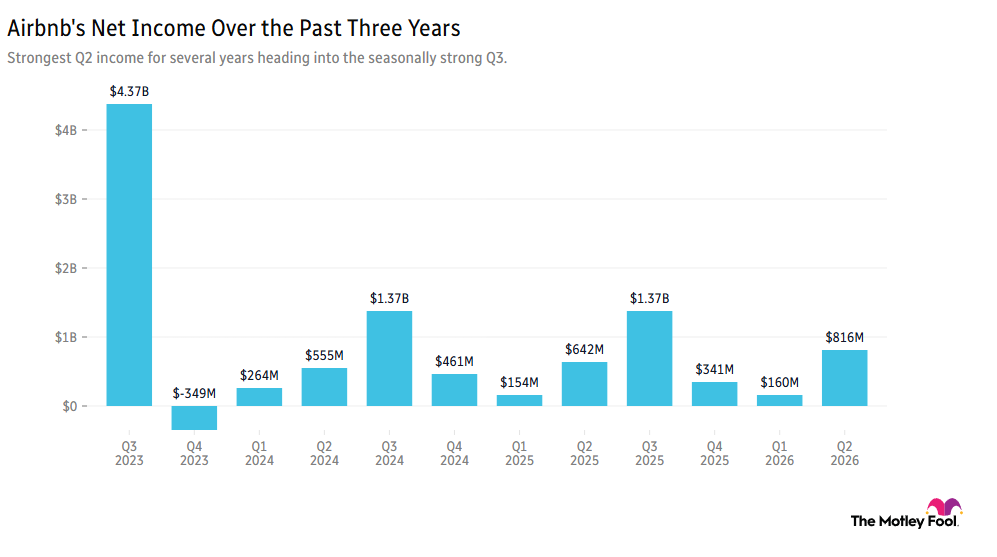

5) The Airbnb Experience

Loading paragraph...

6) Your Take

What's a stock in your portfolio that unites the growth crowd and the value crowd?

Share with friends and family, or become a member to hear what your fellow Fools are saying!