Wake up to the latest market news, company insights, and a bit of Foolish fun -- all wrapped up in one quick, easy-to-read email, called Breakfast News. Delivered at 7:30 a.m. ET every single market day. See an example of our weekday Breakfast News email & sign-up below.

Loading image...

Loading raw_html...

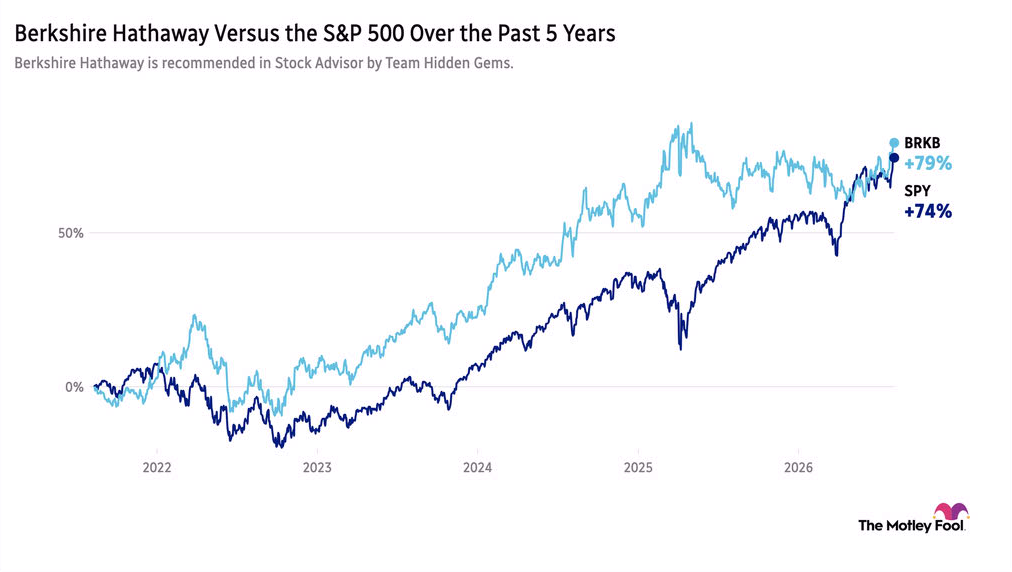

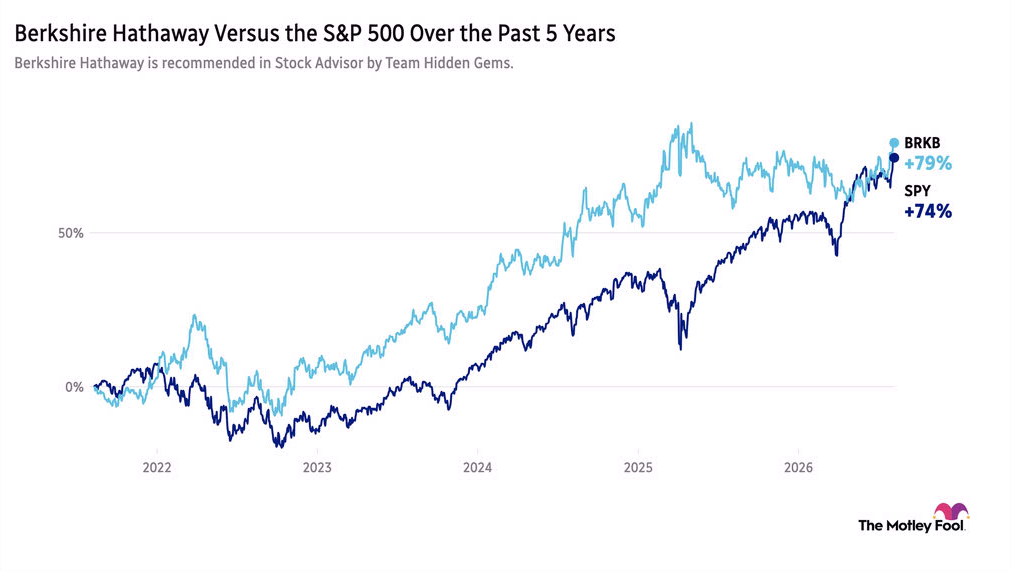

1) Berkshire Hathaway Ends Its Three-Year Buying Drought

Loading raw_html...

Loading paragraph...

2) Bad Jobs News, Best Week for Stocks in Months

Loading paragraph...

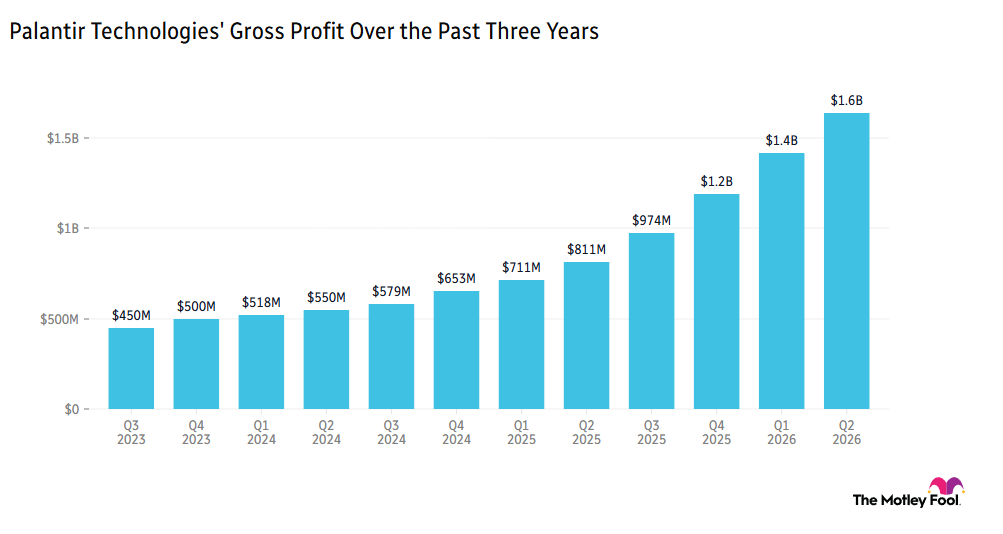

3) Hidden Gems With Something to Prove

Loading paragraph...

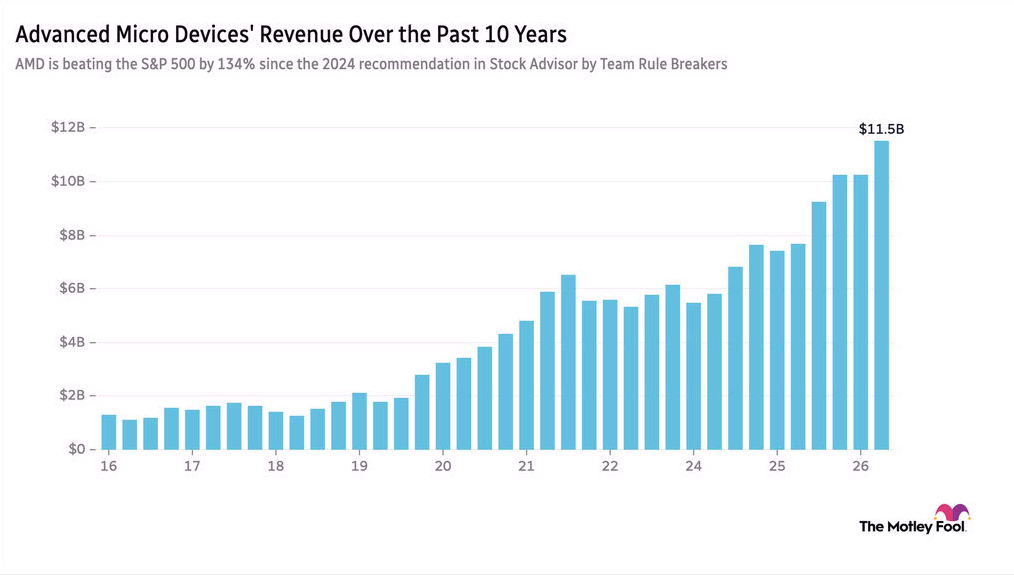

4) Guidance Will Matter More Than the Beat for These Rule Breakers

Loading paragraph...

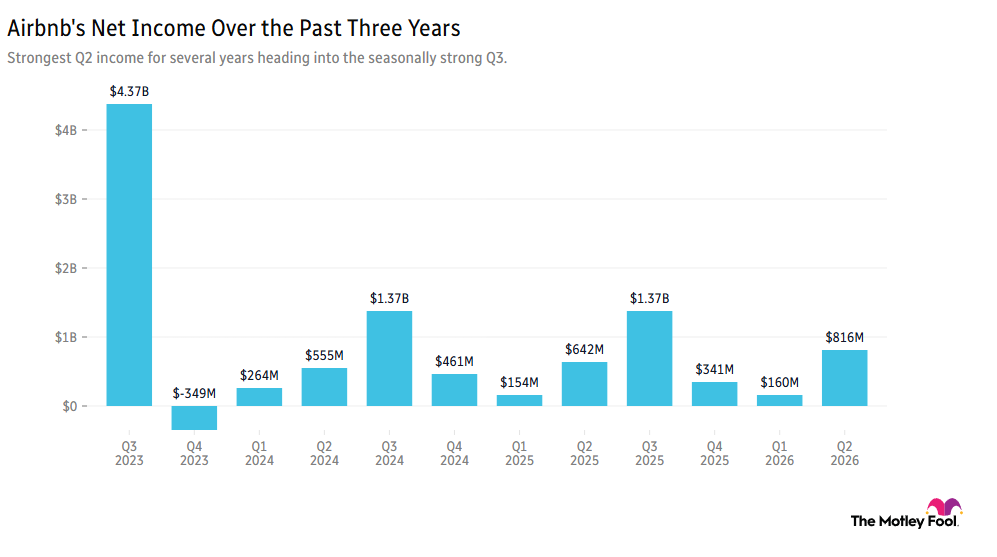

5) DoorDash's Drop Was Our Opening

Loading paragraph...

6) Your Take

Loading paragraph...