Wake up to the latest market news, company insights, and a bit of Foolish fun -- all wrapped up in one quick, easy-to-read email, called Breakfast News. Delivered at 7:30 a.m. ET every single market day. See an example of our weekday Breakfast News email & sign-up below.

Loading image...

Loading raw_html...

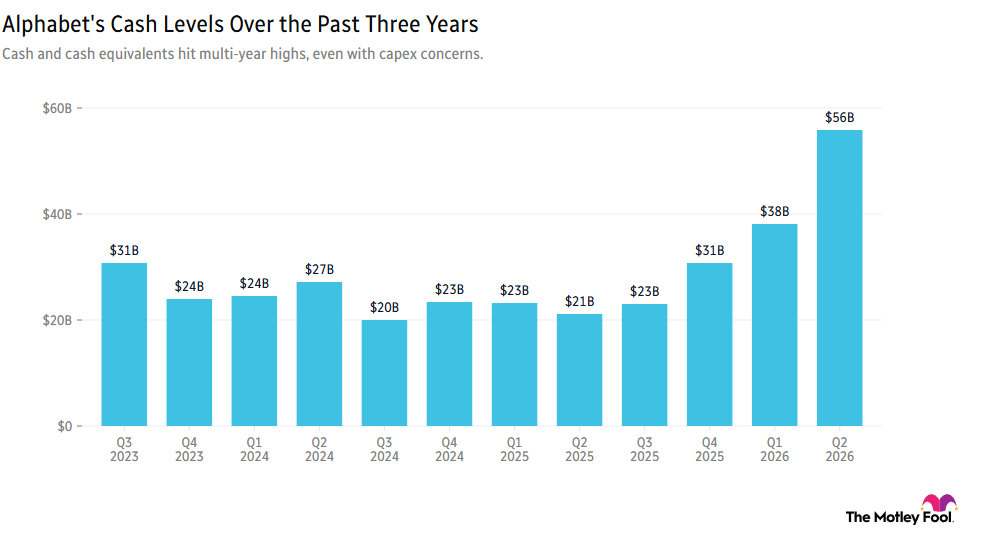

1) Alphabet Drops on Higher Capex Target

Loading paragraph...

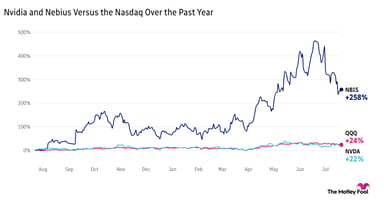

2) Notable After-Hours Movers and Shakers

Loading paragraph...

3) Intel, AMD Aim to Lock Down Long-Term Deals

Loading paragraph...

4) Next Up: TSCO & DGX Report Ahead of KNSL

Loading paragraph...

5) Today's Take: The Customer Is Always Right

Loading paragraph...

6) Your Take

What stocks have you added to your portfolio in the last few weeks, and why?

Share with friends and family, or become a member to hear what your fellow Fools are saying!