Individual retirement accounts (IRAs) have a clear purpose: to help you save for retirement. However, if you want to access your retirement savings early, you may wonder whether you can borrow from an IRA.

In general, borrowing from an IRA isn't allowed. But there is a way to take funds out of your IRA temporarily. There are also some situations where you can make a penalty-free withdrawal. In this guide, you'll learn all about the IRA rules for borrowing money.

Type-based

Type-based borrowing

Q: Can you borrow from an IRA?

While you can't borrow from an IRA in the traditional sense, there is a way to remove money from an IRA and then replace it within a specified period without incurring a penalty.

Under the 60-day rule, an IRA account owner can withdraw money as long as it is returned in full within 60 days, beginning with the original withdrawal date (more on that below). While this isn't technically borrowing in a principal-plus-interest sense, it serves a similar function -- with caveats.

Q: Can you borrow against a Roth IRA?

No. Like a traditional IRA, a Roth IRA is meant for long-term savings and investing. It's specifically intended to fund retirement expenses. But there are ways to circumvent this intent.

You're permitted to withdraw Roth IRA contributions at any time, regardless of your age, without owing taxes or a penalty. But once you've taken a Roth IRA withdrawal, you can't replace those funds. You can only deposit up to the Roth IRA annual contribution limits in any given year.

Q: Can you borrow from an inherited IRA?

No. An inherited IRA doesn't allow contributions or 60-day rollover transactions. The IRS rules for distributions of IRA funds inherited by non-spouses became stricter under the Secure Act of 2019.

The law eliminated the stretch IRA (which allowed beneficiaries to "stretch" distributions over their lifetimes) for most non-spouses. Under the current inherited IRA rules, non-spouse beneficiaries typically need to liquidate these accounts within 10 years.

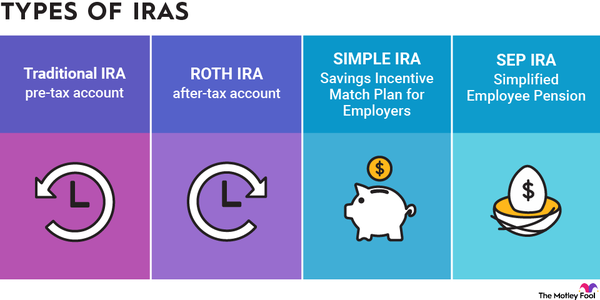

Q: Can you borrow against a SEP-IRA?

No, but once again, you can remove money and then replace it within 60 days. Much like the other IRAs on this list, a SEP-IRA is intended to help cover your retirement expenses, not fund short-term goals. If you do choose to remove money, you'll need to ensure all of it is paid back within a 60-day period to avoid taxes and penalties.

Q: Can you borrow against a traditional IRA?

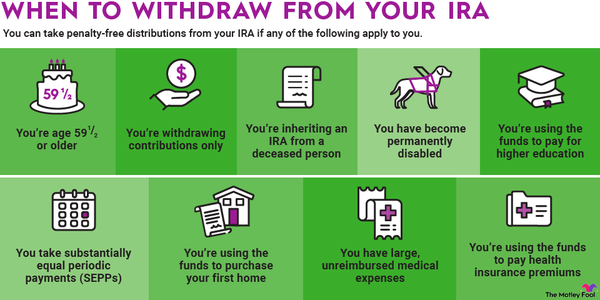

Not in the true sense, but there are several ways to access IRA funds without incurring a 10% penalty. The IRS will waive the 10% penalty on withdrawals from an IRA if you become completely and permanently disabled. You can also take limited penalty-free withdrawals in some cases, like if you're having a child or you meet the IRS definition of a first-time homebuyer.

Situation-based

Circumstance-based borrowing

Q: Can you borrow from an IRA to buy a house or do home improvements?

You can access certain IRA funds to help you buy your first home. Note that the IRS generally treats you as a first-time homebuyer if you haven't owned a primary residence within three years.

You can withdraw up to $10,000 without penalty from a traditional IRA or your Roth IRA earnings. (Remember, under Roth IRA rules, you can access your contributions but not your earnings at any time without tax or penalty.) The same provision doesn't exist for home improvements, though.

You could, in theory, remove money from a traditional IRA, pay for home improvements, and then return the full withdrawal amount to your account within 60 days without taxes or penalty. However, it would be rather unusual for this to be a recommended personal finance option.

Q: Can you borrow from an IRA to buy a car?

There is no specific provision that would allow for this. Still, as with the above example, it would be technically permissible to withdrawal money from your IRA, buy a car, and then return the full proceeds to your IRA within 60 days. This might work if you're expecting a large cash inflow during that 60-day period. But generally, using IRA funds to buy a car -- unless you're already retired -- is not the best idea.

Borrowing rules

Borrowing rules

Q: Can I borrow from my IRA for 60 days?

Many IRA types (specifically excluding the inherited IRA) allow for the 60-day rule. This means you can take money out of your IRA as long as it is returned in full within 60 days of the original withdrawal.

For example, if you take $10,000 from your IRA and 10% is withheld for federal tax, you'll receive $9,000 in cash, but you still must return $10,000 to your IRA within 60 days.

One wrinkle here is that you can only do this once within a 12-month period. It is also not "borrowing" in the traditional sense. It's really meant to allow for IRA rollovers, but it can accomplish the desired result.

Q: Can you borrow from an IRA without penalty?

You can't borrow from an IRA, but the IRS provides a loophole where you can temporarily access your funds as long as you replace the money in full within 60 days. The IRS says that if you borrow money from an IRA, the account is no longer considered an IRA, and its entire value would be included in your taxable income for the year.

Q: How much does it cost to borrow from your IRA?

While you won't pay any taxes, penalties, or interest if you withdraw money from your IRA and then return the funds in full within 60 days, you need to be extremely careful. If you fail to comply with any aspect of the 60-day rule, it can cost you quite a bit, including the opportunity cost of tax-advantaged growth in your retirement account. It also costs peace of mind to know that you're up against so many restrictive rules.

Q: How much can I borrow from an IRA?

You can withdraw the entire balance if you want, but your provider will withhold 10% for taxes. To avoid unnecessary costs, you'll still need to return the entire amount (pre-tax).

Related retirement topics

Key takeaways

Borrowing from your IRA is possible, but it is not recommended. There are also ways to qualify for an early distribution for qualified expenses, such as buying a home, but these IRA distributions fall under an exception and do not need to be returned to your IRA.

Keep in mind that they call it an individual retirement account for a reason. Your IRA is meant for retirement, and it's by far the best idea to use it for its intended purpose.

FAQ

FAQ

How can I borrow money from my IRA without penalty?

You can't borrow from your IRA without penalty unless you return the money in full within 60 days. If you take longer than that to repay the money, it's classified as a distribution, and you owe all applicable income taxes and an early withdrawal penalty.

How can I withdraw money from my IRA without penalty?

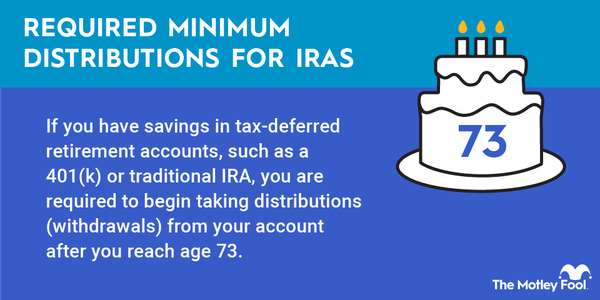

You must wait until age 59 1/2 to withdraw money from your IRA without penalty. If you have a Roth IRA, you can withdraw contributions at any time but not earnings on those contributions.

There are a small number of exceptions where you can withdraw from an IRA and avoid an early withdrawal penalty. Exceptions include qualified first-time home purchases, qualified higher education expenses, and unreimbursed medical expenses.

What is the 60-day IRA withdrawal rule?

The 60-day IRA withdrawal rule gives you 60 days after a distribution to roll it over to another IRA or the same one. You could effectively get a loan from your IRA, provided you pay the entire amount back within 60 days.

Is there a penalty for borrowing from an IRA?

If you withdraw money from an IRA before age 59 1/2, there's normally a 10% early withdrawal penalty. The penalty applies even if you're borrowing the money unless you pay it back in full within 60 days.