Now that the Wall Street Journal has run two articles on the cord-cutting trend in just four weeks, pay TV's dinosaur-like march to extinction is inevitable.

As pay TV wanes, will Netflix (NASDAQ:NFLX) lead the evolution?

DVD's Death March

DVD sales reached a peak in 2004 selling 1.2 billion discs for a record breaking $24.5 billion. Almost 70% of homes had DVD players in 2004.As existing customers bought fewer discs and disc player sales slowed, DVD sales began to drop every year.

In 2012 the seven-year slide in sales reversed slightly increasing 0.23% to $18 billion. That's still a 25% decline in seven years and a lot of lost revenue for content producers. Production companies looking for new ways to capitalize on content rolled out systems like UltraViolet -- a cloud-based way to own digital copies. However, consumers are becoming less interested in owning digital or physical programming and turning to streaming video on demand (VOD). Digital download sales increased an impressive 35% in 2012, but VOD was up by 48%

Disappearing cable customers

The other trend keeping Netflix investors on board are the net losses in cable/satellite subscribers in Q2 2013. Time Warner Cable (NYSE: TWC) had 573,000 fewer video subscribers in Q2 2013 (11.9 million) compared 12.5 million in 2012. Video revenue was also down.

DirecTV (DTV +0.00%) net disconnects rose year-over-year in the US (84,000 in 2013 vs. 52,000 in 2012) but managed to increase subscribers slightly to 20 million in the US.

Comcast (CMCSA 1.28%) also lost residential video customers—down 159,000 to 22 million. Overall, U.S. cable television subscriptions declined to 56.7 million in 2012, down 3% from 2011 according to information and analytics provider HIS.

The cable/satellite providers still command an impressive subscriber base, but it may have peaked and is now reversing. Younger consumers may be a big part of the trend either cord cutting or never buying cable, opting to buy streaming video on demand.

Netflix and the Golden Age of television

Television changes all the time and the programming of the 1950's looked nothing like the content available in the 1970's and that only faintly resembled the cable channels and original series that have sprung up like weeds after a monsoon in the past decade. New series and channels are an overwhelming flood of surprisingly high quality entertainment a long way from Father Knows Best and Rawhide.

One key philosophy Netflix embraces that other networks are not entirely on board with is the data dump of whole seasons of a series all at once. This is unwholesomely known as binge viewing. Binge eating and binge drinking are considered poor life style choices, but binge viewing has transcended the negative connotations and become something of a badge of honor and admission to the club of high tech TV viewing. Kevin Spacey had penetrating observations on the new TV and likened a 13-hour series to a luxuriously long movie. Why do movies have to wrap up everything in a neat two-hour format or a series be portioned out in one-hour bites? The speech is well-worth listening to.

Negatives

Viewers do not get sports and sports are a driving force behind a lot of subscriptions. There is also the absence of new seasons of hit shows and new movies that lag DVD and premium TV release Content providers are balancing the revenue they need from cable/satellite against the new revenue from streaming and most continue to give pay TV new season leverage.

Disney broke ranks last year and Netflix has the right to exclusively stream new Disney releases starting in 2016. Sources say Netflix will pay $350 million per year – a large premium to the $200 million per year Disney currently collects. Money talks and it seems unlikely content costs are going to moderate.

At present, margins are low and cash flow has shrunk as Netflix transforms its business. It's a matter of scale and as the base grows, the costs are spread over a larger number of subscribers improving margins. It's critical that Netflix keeps adding subscribers at record numbers. Each quarter that exceeds expectations in adds keeps the share price moving up

Is the streaming model profitable?

Right now it doesn't matter.

At present, margins are low and cash flow has shrunk as Netflix transforms its business. It's a matter of scale and as the base grows, the costs are spread over a larger number of subscribers improving margins. It's critical that Netflix keeps adding subscribers at record numbers. Each quarter that exceeds expectations in adds keeps the share price moving up.

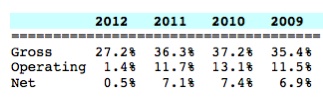

Annual combined GAAP margins

The $300 price per share was cracked back in July 2011 when margins were peaking and growth in revenue was 51% for Q2 2011. At that time investors were impressed both by growth and earnings/margins. Diluted earnings per share reached an all-time high in 2011 of $4.16 and cash flow was at $318 million. Impressive growth, high earnings and ample cash flow fueled record high share prices, but that's changed and the recent run is fed more by the technology and potential than spreadsheet numbers.

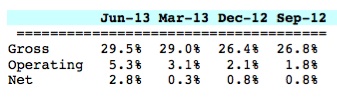

Quarterly combined GAAP margins

The last four quarters margins are far lower than the best years 2010-2011. They are improving as scale expands -- more subscribers.

Subscription growth

Revenue growth lags 2010-2011 levels -- subscribers paying $7.99 per month are not providing the same increases DVDs allowed. One drawback of the streaming model presently is lack of pricing power in a competitive space. Cash flow at $23 million in 2012 is at the lowest level in over 10 years.

A different way to look at margins that explains cash flow

Netflix doesn't use the cash cost of their content/inventory to calculate gross margins. Their GAAP costs are the amortization of content and that doesn't perfectly reflect what Netflix spends in a quarter. Until Q1 2013 there wasn't a way to calculate the cash margin-- now we can.

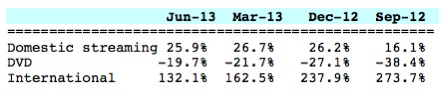

GAAP margins for total streaming (DVDs excluded)

Cash margins for total streaming

Operating margins include only marketing (as reported by Netflix) – Netflix does not provide other expenses by segment. If costs included administrative, R&D, interest, and taxes, operating and net cash margins would be negative. This helps to explain why cash flow is not approaching historic highs even as revenue sets record highs every quarter. The biggest operating segment on a cash basis is not turning a profit.

DVD cash gross margin in Q2 was 51% and the operating margin was 49%. The DVD business remains extremely profitable but subscriber numbers decrease every quarter and revenue was only 22% of total revenue.

What will binge viewing do to future margins?

There was a short disclosure in Q2 commenting on viewing patterns for new content and possible future changes in costs. If the original programming is viewed primarily in the first few weeks or months with a rapid tailing off, amortization will have to be front-loaded increasing the expense per period immediately tapering off with viewing over the period of the license. House of Cards would cost more in the first few quarters after its release and then decrease over the remainder of the license. The more original content they release, the greater the impact on margins.

In the end

Costs, earnings and cash flow are unimportant at this stage. These aren't the numbers that matter to investors –subscriber adds and exclusive content coups are paramount. With evidence that traditional pay TV subscribers and DVD sales are in decline, the market looks ready for a first mover and technically superior streaming service like Netflix to put itself in every household that has Internet access. With enough subscribers, they should see better margins and higher earnings. As of October 2012, 88 million US households had high speed Internet (72% penetration) suggesting that the current 27 million domestic streaming subscribers has room for enormous growth and international growth may be even higher. Netflix will need to translate the high growth into high profits.