Investing refers to the practice of allocating your money into an asset with the goal of generating a return. To name a few examples, buying stocks, investing in a rental property, and even putting money into a certificate of deposit at your bank are all forms of investing.

When done the right way, investing can be an extremely reliable way to build wealth over time. But how should you get started? What is the best way for you to put your money to work? Whether you're a new investor or an experienced one who wants to invest better, we're here for you. It's time to make your money work for you.

Before you put money into the stock market or other investments, you'll need a basic understanding of how to invest your money the right way. Unfortunately, there's no one-size-fits-all answer here.

The best way to invest your money is the way that works best for you. To determine this, you'll want to identify your investing style, budget, and risk tolerance. So, let's briefly take those one at a time.

Why is investing important?

There are more reasons why investing is important than we can realistically list here. But to name some of the most important:

- Build wealth: Investing, especially in the stock market, can be an extremely reliable way to grow your money over the long term.

- Achieve financial freedom: Investing can help you be prepared for whatever life throws your way and retire on your own terms.

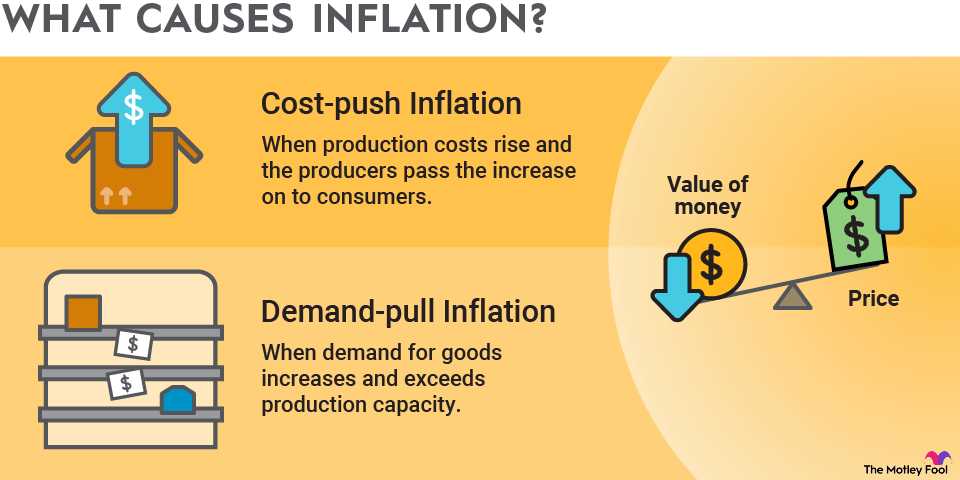

- Preserve spending power: If you put your money in a low-paying savings account, it will actually be worth less over time, thanks to inflation. There are low-risk investments that can reliably help you keep up with or even outpace inflation.

Common myths about investing

Before we go any further, let's take a moment and address some of the common misconceptions about investing:

- You need a lot of money to get started investing. With the emergence of zero-commission brokers and fractional shares, it is easier than ever to start investing with minimal capital. In fact, it's possible to construct a diversified investment portfolio with as little as $100 or even less. The key is adding to it consistently over time.

- Investing is too risky. Over short periods, investing can be volatile. But over the long term, investing can be a great way to build wealth without taking excessive risks.

- Day trading is the best way to make money. Short-term trading is best left to the pros. The most surefire way to produce strong returns is to buy great investments and hold them for as long as they remain great investments.

Now, let's get to the steps you'll need to take to invest money the right way.

How to invest money

- Identify your investing style.

- Determine your budget for investing.

- Assess your risk tolerance.

- Decide what to invest your money in.

1. Your investing style

How much time do you want to dedicate to investing your money?

The investing world is divided into two major camps when it comes to investing: active investing and passive investing. Neither is a clear winner.

Both can be great ways to build wealth as long as you focus on the long term and aren't just looking for short-term gains. However, your lifestyle, budget, risk tolerance, and interests might give you a preference for one type.

Active investing

Active investing involves taking the time to research your investments and constructing and maintaining your portfolio independently. In simple terms, if you plan to buy and sell individual stocks through an online broker, you're planning to be an active investor. To successfully be an active investor, you'll need three things:

- Time: You'll need to research stocks, perform some basic investment analysis, and keep up with your investments after you buy them.

- Knowledge: All the time in the world won't help if you don't know how to analyze investments and properly research stocks.

- Desire: Many people simply don't want to spend hours on their investments. And there's nothing wrong with that.

It's also important to understand what we don't mean by active investing.

- Active investing doesn't mean buying and selling stocks frequently.

- It certainly doesn't mean day trading.

- It doesn't mean buying stocks because you think they will go up over the next few weeks or months.

Passive investing

Passive investing is akin to an airplane on autopilot. You'll still achieve good results over the long run with minimal maintenance or adjustments. Passive investing involves putting your money to work in investments where someone else does the heavy lifting.

Mutual fund investing is an example of passive investing, as are exchange-traded funds (ETFs). Alternatively, you can hire an advisor or use a robo-advisor to design and implement an investment strategy on your behalf.

Passive investing

More simplicity, more stability, more predictability

- A hands-off approach.

- Moderate returns.

- Tax advantages.

Active investing

More work, more risk, more potential reward

- Investing yourself (or through a portfolio manager).

- Lots of research.

- Potential for huge, life-changing returns.

2. Your budget

How much money do you have to invest?

You may think you need a large sum of money to start a portfolio, but as we mentioned earlier, you can begin investing with $100 (or even less). We also have great ideas for investing $1,000. With that in mind, here are some key points to consider when it comes to your budget:

- The amount of money you're starting with isn't the most important thing. It's whether you're financially ready to invest and to continue investing over time.

- Establish an emergency fund before you begin investing. You never want to be forced to sell investments in a time of need.

- Get rid of any high-interest debt (like credit cards) before investing.

Divest

3. Your risk tolerance

How much financial risk are you willing to take?

Not all investments are successful. Each type of investment has its own level of risk, but this risk is often correlated with returns. Here are some key points to consider when evaluating your risk tolerance:

- It's essential to strike a balance between maximizing returns on your investment and finding a comfortable risk level.

- High-quality bonds, such as Treasury bonds, offer predictable returns with very low risk. By contrast, stock returns can vary widely depending on the company and time frame, but have historically averaged about 10% per year.

- There can be huge differences in risk, even within the broad categories of stocks and bonds.

- Savings accounts represent an even lower risk but offer less reward.

- One effective solution for beginners is to utilize a robo-advisor to create an investment plan tailored to your risk tolerance and financial objectives.

4. What should you invest your money in?

How do you decide where to invest your money?

This is a challenging question; unfortunately, there is no perfect answer. The best type of investment for you depends on your investment goals and risk tolerance. But with the guidelines discussed above in mind, you should be far better positioned to decide what to invest in.

For example, if you have a relatively high risk tolerance, along with the time and desire to research individual stocks (and learn how to do it effectively), that could be the best approach. If you have a low risk tolerance but want higher returns than you'd get from a savings account, bond investments (or bond funds) might be more appropriate.

If you're like most Americans and don't want to spend hours managing your portfolio, investing in passive assets like index funds or mutual funds can be a smart choice. And if you really want to take a hands-off approach, a robo-advisor could be right for you.

There are numerous other investment options available, in addition to stocks, bonds, index funds, and mutual funds. Just to name a few examples, you can choose to invest in:

- Savings accounts -- These can be a great way to invest your emergency savings or money that you might need at any given time.

- Certificates of deposit (CDs) -- A CD can allow you to lock in a certain yield for a period of time, with no risk of losing your principal.

- Treasury securities (Treasuries) -- Treasury securities come in maturity lengths ranging from one month to 30 years, and can be excellent fixed-income alternatives to corporate bonds or bond funds.

- Real estate -- If you're willing to be more hands-on, buying investment properties can be a great way to build wealth and generate income.

- Cryptocurrencies -- Digital assets like Bitcoin (BTC -8.68%) are a relatively new type of investment, but can be a wise addition to a diversified investment strategy.

How to track your investments

First, you don't need to check your investments every day. One of the biggest rookie mistakes is paying too much attention to your long-term investments and making emotional decisions based on short-term performance.

According to several studies, the average investor underperforms the market. A key reason is that they make knee-jerk reactions instead of just leaving investments alone.

Having said that, tracking your investments (reasonably often) is an important part of the journey. Your brokerage app or website should allow you to view your entire investment portfolio, and you may be able to set up alerts. For example, I get a push notification on my smartphone if any of my stocks move up or down by more than 5% in a single day.

There are also personal finance and investment apps that will allow you to build your own watch lists of stocks and/or import data from your brokerage account to track your portfolio. This can be especially useful if you have accounts at multiple brokerages.

Key mistakes first-time investors should avoid

As we've discussed, knowing how to invest money can be extremely important when it comes to building wealth and creating financial security. But it can be even more important to know how not to invest.

For one thing, avoid over-trading. I've mentioned this elsewhere in the article, but it's worth repeating. One of the most common reasons for poor investment performance is constantly moving in and out of stocks and funds.

There's a good reason for this. It's common knowledge that the goal of investing is to buy low and sell high, but our emotions tell us to do the exact opposite. When stocks rise, and we see others making money, that's when we want to buy. And when stocks drop, it's our instinct to sell before things get any worse.

Other common mistakes for first-timers to avoid:

- Don't try to day trade, meaning buying stocks that are going to go up over the next few hours or days. Leave that to professional traders.

- Don't invest with margin (borrowed money). Not only do you pay interest on the money you borrow, but using margin can also amplify your losses if things don't work out.

- Don't even touch options trading until you really know what you're doing.

- Don't confuse investing with speculating. There can be room for both, but it's important to know when you're taking a risk that could wipe out your entire investment.

Related investing topics

The bottom line on investing money

Investing money may seem intimidating, especially if you're new to it. However, if you figure out how you want to invest, how much money you should invest, and your risk tolerance, you'll be well-positioned to make smart decisions with your money that will serve you well for decades to come.

FAQ

How to invest money FAQ

About the Author