Learning a new language can open up doors: for travel, for work, even for love.

Yet many people who say they want to learn never do. Why is that? Often, it's because the process of learning a new language can be boring and challenging.

Duolingo (DUOL 3.64%) is out to change that. And if it can make language-learning engaging and fun, it can help more than just language learners. Shareholders will benefit too.

First reason to buy: The market for language learning software is growing -- fast

According to market research firm Facts and Factors, the demand is soaring for online language learning apps. A recent report estimates the total market size for online language learning was $14.1 billion in 2021. Moreover, the same report estimates the market will double in size to $28.5 billion by 2028.

It cites these key drivers behind the trend:

- Improving levels of worldwide education.

- Increasing rates of travel.

- Technological advancements.

All told, more and more people want to learn a new language, and they're increasingly willing to pay for a service that helps them.

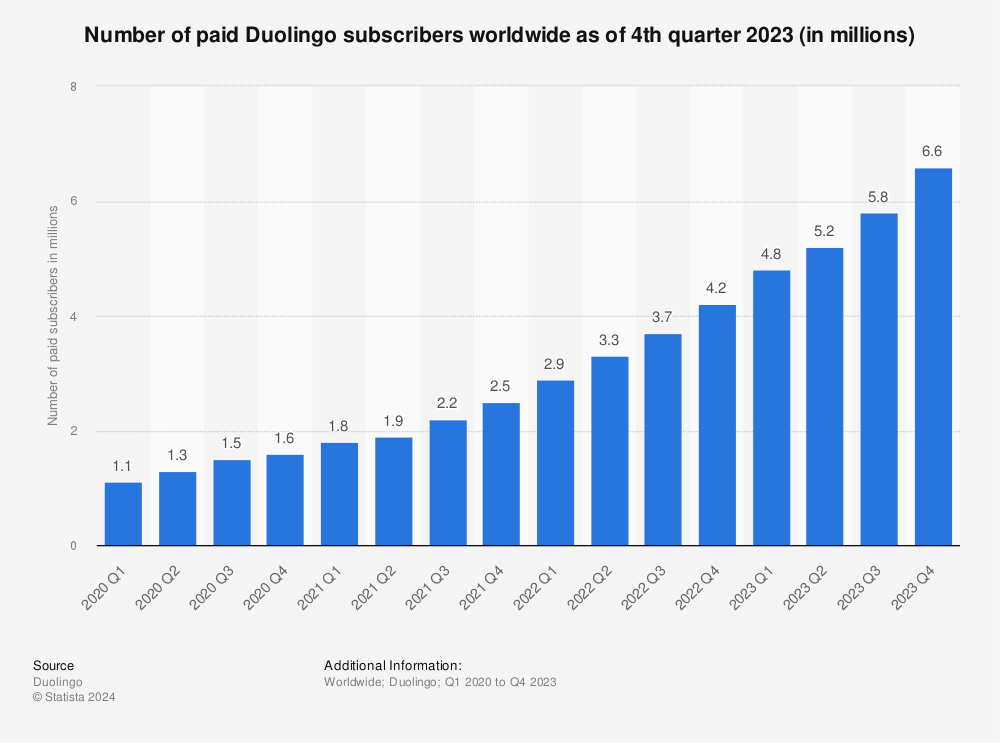

Second reason to buy: Paid subscriber growth

While Duolingo generates revenue from ads and other sources, most revenue comes from its subscription service, Super Duolingo (formerly known as Duolingo Plus). In the first quarter, subscription revenue was $58 million, up 45% year over year.

Meanwhile, paid subscribers grew to 2.9 million, up 60%. Duolingo credits product improvements and innovation for increasing customer conversion and retention. All told, the company has almost tripled its paid subscribers since the start of 2020.

Find more statistics at Statista.

One reason to hesitate: Lack of profit

Despite its impressive growth trajectory, Duolingo isn't without its challenges. The company is unprofitable with negative earnings before interest, taxes, depreciation, and amortization (EBITDA) of $55.5 million over the past year. Its operating margin in the first quarter stood at negative 14.6%.

Data by YCharts.

Moreover, analysts expect the company to lose money for at least several more years. Wall Street is forecasting losses per share of $1.76 and $1.50 in 2022 and 2023, respectively.

Those losses might not be a problem when the economy is humming along, but they could prove problematic now. Inflation is high; wages aren't keeping up; interest rates are soaring; and the cost of doing business is increasing across the board.

Thankfully, Duolingo's balance sheet appears well positioned to ride out a poor economy. The company has $577 million in cash and no debt.

Is Duolingo a buy now?

For me, the current state of the economy is no reason to shun Duolingo. The company is riding long-term trends in the language-learning market that may take years to fully play out. In the meantime, its balance sheet gives me confidence that it can survive any downturn while continuing to invest in the innovation necessary to grow its subscriber base for years to come.