The macroeconomic challenges that characterized much of the past two years are beginning to fade. After plunging 35% in 2022, the Nasdaq Composite bounced back in 2023, gaining 43%. While the market is currently regrouping, history suggests there could be more gains to come.

Reviewing data going back 51 years, in every year that followed a market recovery, the tech-centric index has gained again in a second year by an average of 19%. That gives us good reason to believe the current rally still has legs. The economy is still fragile, and conditions could erode, but another strong year may be ahead for the stock market.

Helping fuel the market's overall gains last year were a group of investor favorite stocks known collectively as the "Magnificent Seven," which outpaced the broader market in 2023 by a wide margin.

- Nvidia: Up 239%

- Meta Platforms: Up 194%

- Tesla: Up 102%

- Amazon (AMZN -1.06%): Up 81%

- Alphabet: Up 58%

- Microsoft: Up 57%

- Apple: Up 48%

Among these household names, one that represents a particularly compelling opportunity for investors today is Amazon. On the heels of its robust gains last year, the stage is set, and the company will likely deliver another standout performance.

Image source: Getty Images.

Lingering challenges

The macroeconomic headwinds of the past couple of years amounted to something of a perfect storm for Amazon. High inflation caused a slowdown in consumer discretionary spending, and online purchases were among the first casualties. This also prompted a commensurate decline in business spending.

Advertising is one area in the budget that companies can easily and rapidly dial down or scale up -- and a broad cutback on that front weighed on Amazon's digital advertising business. Furthermore, many companies put their digital transformations -- highlighted by the shift of workloads to the cloud -- on the back burner, which caused slowing growth for Amazon Web Services (AWS), the company's cloud infrastructure business.

While the effects of those issues linger, things are looking up for Amazon.

The undisputed leader in e-commerce

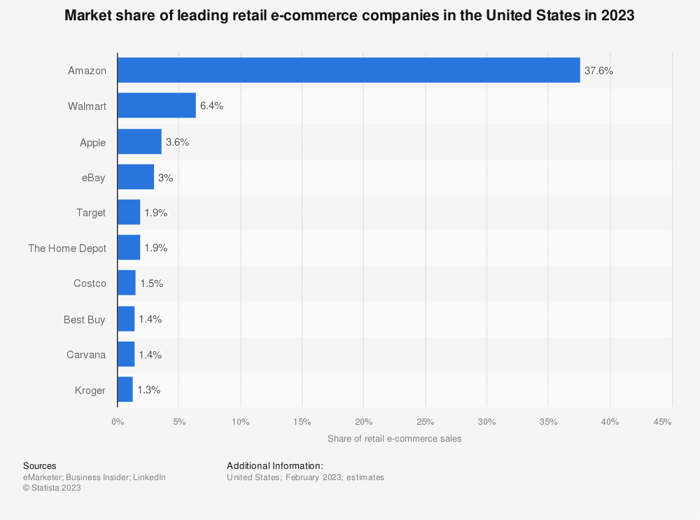

Despite persisting unease regarding the economy, there are reasons to remain optimistic. Amazon is synonymous with e-commerce, an industry it still dominates. While the figures for 2023 have yet to be tallied, Amazon accounted for roughly 38% of all online sales in the U.S. in 2022, more than the next 14 competitors combined, according to online data provider Statista. It's unlikely the company ceded its industry-leading position, though the competition might have made some inroads.

Image source: Statista.

Furthermore, e-commerce sales are expected to grow by more than 9% in 2024 to $6.3 trillion, representing more than 20% of all retail sales, according to estimates provided by Insider Intelligence. As the online sales leader, Amazon will benefit from this secular tailwind.

It all "ads" up

One of Amazon's biggest growth drivers in recent years has been digital advertising, owing to the company's captive audience. In the third quarter, Amazon's digital advertising revenue grew 26% year over year, outperforming its largest rivals, Alphabet and Meta Platforms, which grew their ad revenues by 9% and 24%, respectively.

Amazon is looking to boost its ad business by showing "limited advertising" on its Prime Video streaming service beginning this month. Subscribers will have the option to pay an additional $3 per month to keep their viewing experience ad-free, but Amazon wins either way.

Furthermore, digital advertising is expected to increase by 13.2% in 2024, after climbing more than 10% last year, according to Insider Intelligence. As the No. 3 digital ad platform in the U.S., Amazon will no doubt benefit from any acceleration in ad spending.

The clouds are lifting

In the face of economic challenges, AWS maintained its position as the world's leading provider of cloud infrastructure services, controlling 31% of the market in Q3, according to market analyst Canalys.

After a period of subdued growth over much of the past two years, cloud adoption is expected to reaccelerate in 2024. Research and consulting firm Gartner estimates that public cloud spending will jump 20% to $679 billion. An acceleration in cloud adoption will likely increase the fortunes of AWS.

You can't spell gains without AI

Last but certainly not least, Amazon has a long and storied history of using artificial intelligence (AI) to improve its operations, and has jumped into the generative AI ring with both feet. AWS Bedrock provides users with access to all the most common AI models, allowing them to build customized AI apps of their own. It also provides access to Nvidia's latest and greatest AI chips -- the H200 Tensor Core graphics processing units (GPUs) -- as well as Amazon's own Inferentia and Trainium AI chips. This lets customers strike a balance between speed and economy.

The company recently launched Amazon Q for enterprises, a generative AI-powered digital assistant designed to help automate and streamline time-consuming and mundane tasks, thereby making users more productive.

Amazon is also providing AI tools to the merchants that sell on its platform to help them succeed. The company introduced AI-powered image generation for digital advertisers while also using AI to improve search and product recommendations. Just this week, Amazon began testing a feature that lets customers ask questions about a product and receive an AI-generated response.

These most recent forays into AI provide a glimpse of Amazon's game plan.

A compelling opportunity

Despite the wealth of opportunity ahead for Amazon, its stock is still reasonably valued at 2 times next year's expected sales.

Given the rebound in online retail, the recovery of the ad market, the ongoing digital transformation, and the AI-inspired gold rush, now is the time to buy Amazon before the stock roars even higher.