Advertiser Disclosure

Many of the offers that appear on this site are from companies from which The Motley Fool receives compensation. This compensation may impact how and where products appear on this site (including, for example, the order in which they appear) and may influence which products we write about, but our product ratings are not influenced by compensation. We do not include all companies or offers available in the marketplace.

Currently Managing Director of Motley Fool Money, Brendan has worked full-time for The Motley Fool since 2011. He has written hundreds of articles for The Motley Fool and provided analysis on TV outlets including CNBC and Fox. He holds a degree in finance from Virginia Tech.

Nathan Alderman has been a full-time Motley Fool employee since 2005, making errors his arch-enemies in a variety of roles including a six-year stint as the dedicated fact-checker for The Motley Fool's premium newsletter services. As Motley Fool Money's Compliance Lead, he makes sure that all the site's information is accurate and up to date, which ensures we always steer readers right and keeps various financial partners happy. A graduate of Northwestern University's Medill School of Journalism, Nathan spends his spare time volunteering for civic causes, writing and podcasting for fun, adoring his wife, and wrangling his two very large young children.

Many or all of the products here are from our partners that compensate us. It’s how we make money. But our editorial integrity ensures that our product ratings are not influenced by compensation.

Picking the right stock broker can make a real difference in how smoothly -- and successfully -- you invest. Whether it's saving on fees, accessing in-depth research, or simply having an app that doesn't make you want to throw your phone, the right platform matters.

Our team spent hundreds of hours researching, testing, and comparing brokerage accounts -- drawing on personal experience and expert insight -- to bring you the best options.

Why trust our recommendations? Here at The Motley Fool, we've spent over 30 years helping investors make smarter financial decisions. And unlike many other finance websites, we do NOT let affiliate compensation influence our ratings. Our recommendations are based on what truly matters: helping you find the best brokerage account for your investing goals.

Short on time? Here are a few of our favorite picks:

SoFi® offers zero-commission trading, fractional shares, and a full suite of financial tools for easy diversification and management. For a limited time, get up to $1,000 in stock when you fund a new account with at least $50 in the first 30 days. Click here to open an account.

Robinhood offers $0 commission trading with instant deposits and fractional shares across stocks, options, and crypto. Click here to open an account.

Our team of experts assessed 45+ trading platforms

We evaluate all brokerage accounts across the same 4 key criteria: user experience, cost efficiency, product variety, and support and security

Our brokerage ratings are never influenced by our advertising partners

We strictly feature products that offer federal insurance and high customer satisfaction, keeping our recommendations unbiased

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Get up to $1,000 in stock when you open & fund a new Active Invest account.

Probability of Member receiving $1,000 is a probability of 0.026%; If you don’t make a selection in 30 days, you’ll no longer qualify for the promo. Customer must fund their account with a minimum of $50.00 to qualify.

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.0/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.0/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Best For:

Passive investing

Commission:

$0 online; $25 broker-assisted fee for some phone trades of stocks and ETFs from other companies (Less than $1 million)

4.0/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.0/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

5.0/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

5.0/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Best For:

Beginners learning how to invest

Commission:

$0 commission for online U.S. stock and ETFs*. No account fees****.

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Best For:

Low cost ETFs and index investing

Commission:

$0 stock, ETF, and Schwab Mutual Fund OneSource® trades. No fees to buy fractional shares.

At Motley Fool Money, brokerages are rated on a scale of one to five stars. We primarily focus on fees, available assets, and user experience; however, we also take into account features like research, education, tax-loss harvesting, and customer service. Our highest-rated brokerages generally include low fees, a diverse range of assets and account types, and useful platform features.

Our aim is to maintain a balanced best-of list featuring top-scoring brokerages from reputable brands. Ordering within lists is influenced by advertiser compensation, including featured placements at the top of a given list, but our product recommendations are NEVER influenced by advertisers. Learn more about how Motley Fool Money rates brokerage accounts.

At Motley Fool Money, brokerages are rated on a scale of one to five stars. We primarily focus on fees, available assets, and user experience; however, we also take into account features like research, education, tax-loss harvesting, and customer service. Our highest-rated brokerages generally include low fees, a diverse range of assets and account types, and useful platform features.

Our aim is to maintain a balanced best-of list featuring top-scoring brokerages from reputable brands. Ordering within lists is influenced by advertiser compensation, including featured placements at the top of a given list, but our product recommendations are NEVER influenced by advertisers. Learn more about how Motley Fool Money rates brokerage accounts.

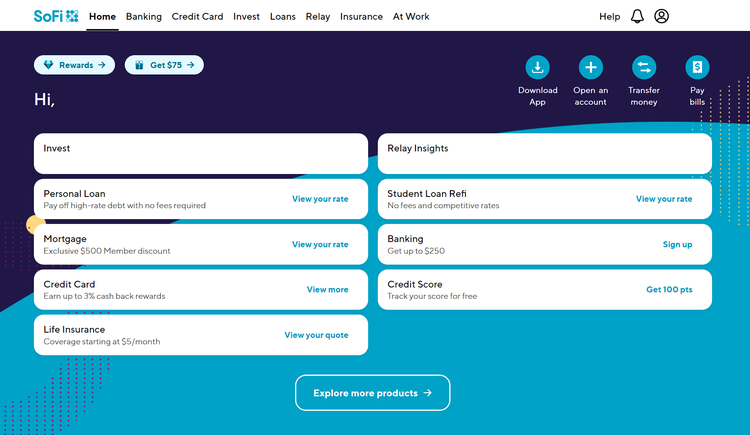

Best for all-in-one financial management: SoFi Active Investing

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

This brokerage is a clear standout for its well-rated mobile app and also has unique investment offerings like IPOs, options, and fractional shares.

Special Offer

Probability of Member receiving $1,000 is a probability of 0.026%; If you don’t make a selection in 30 days, you’ll no longer qualify for the promo. Customer must fund their account with a minimum of $50.00 to qualify.

Get up to $1,000 in stock when you open & fund a new Active Invest account.

Why it made our list: If you're looking for an easy way to invest and manage your money all in one place, SoFi Active Investing is a solid choice. You can trade stocks, invest for retirement, and even open bank accounts -- all without paying commission fees. Plus, if you use multiple SoFi® products, you might score perks like lower APRs on personal loans.

Getting started is simple, too. With fractional shares, you can buy into big-name stocks like Apple or Amazon for as little as $5. And for those who want more than just stocks and ETFs, SoFi® also offers access to mutual funds and IPOs.

Bottom line? If you want an investing platform with a slick mobile app and extra financial tools, SoFi® is worth a look.

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

A top pick for beginners, Robinhood combines $0 commission trades, an easy-to-use app, and a rare retirement deposit match.

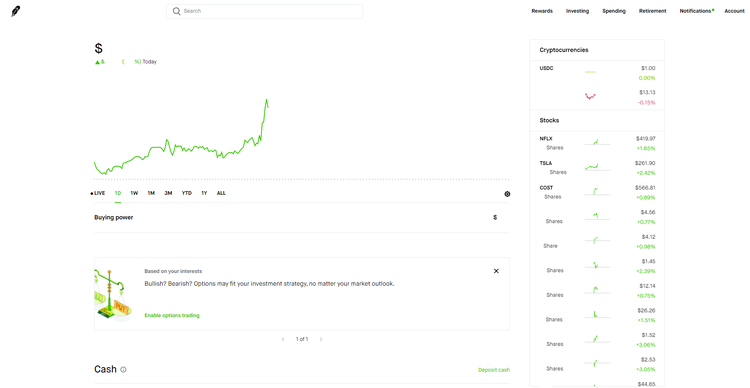

Why it made our list: Robinhood keeps investing simple and affordable, making it a great choice for anyone looking to trade stocks, ETFs, and options with low costs. One standout feature is its commission-free options trading, which eliminates per-contract fees -- something few brokers offer.

But what really sets Robinhood apart is its IRA match program. Like an employer 401(k) match, Robinhood adds a bonus to your retirement contributions -- 1% for all users and 3% for Robinhood Gold members. No other broker offers a match like this, making it an especially great option for self-employed investors.

Add in fractional share trading, which lets you start investing with as little as $1, and Robinhood is a solid pick for cost-conscious traders looking for a user-friendly platform.

Pros:

$0 commissions on stocks, ETFs, crypto, and options

Easy to use trading app

Fractional shares

IRA match

Cons:

No mutual funds

No bonds or CDs

First-hand review from one of our employees who usesRobinhoodpersonally:

"I've been using Robinhood since it launched. At the time, it was one of the only platforms to offer zero-fee trades. The platform was developed to be mobile-first, so the app is clean and easy to use. It also recently launched an IRA product, which is built in to the existing app. The account was easy to open, and since I was already familiar with the platform, it's intuitive to fund the IRA and buy stocks."

-Louis Feldsott, Data Analyst here at The Motley Fool

What it looks like:

Best for deep data analysis: E*TRADE from Morgan Stanley

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

E*TRADE offers low fees and tons of account types. If you need it, chances are, E*TRADE has it. You can access advanced features through its popular Power E*TRADE platform. Open an E*TRADE account to trade fee-free mutual funds and do all your investing in one place.

Special Offer

Open a new eligible E*TRADE brokerage account, fund your account within 60 days of opening, and earn a cash bonus of up to $1,000, depending on the size of your deposit. Offer good for one use per customer, on a single account. Please read full terms and conditions on our website.

Open and fund a brokerage account and get up to $1,000. Terms apply.

Why it made our list: E*TRADE from Morgan Stanley offers a wide range of investment options, including stocks, ETFs, options, and thousands of no-load mutual funds -- many of which can be traded commission-free. It's a strong choice for investors who want both variety and low-cost trading.

Where E*TRADE really shines is its powerful research and analysis tools. The platform lets you customize charts with up to 16 columns and 65 different metrics, giving data-driven investors the ability to sort, prioritize, and analyze the numbers that matter most.

Whether you're using the deeply featured desktop platform or the robust mobile app, E*TRADE is one of the best online brokers for investors who love digging into research and analytics.

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

A great low-cost option for small trade volume. While the interface isn't as clean or modern as that of other brokers, it gets the job done. Interactive Brokers is also a great choice for options investors, traders, and those trading on margin.

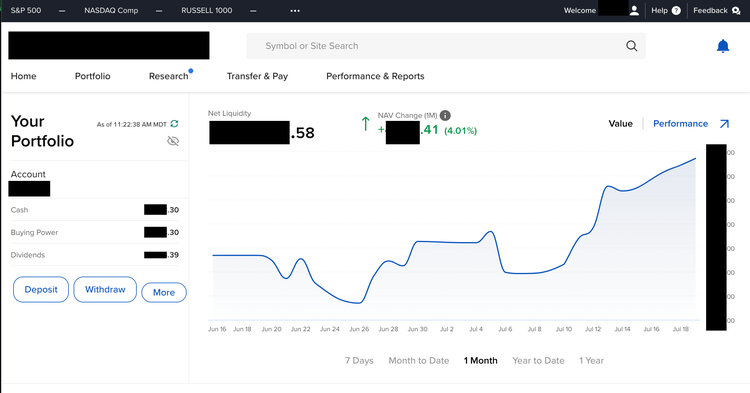

Why it made our list: If you're looking for unmatched market access, Interactive Brokers is tough to beat. With the ability to trade stocks, ETFs, options, futures, forex, cryptocurrencies, and mutual funds across 150-plus markets, it offers the widest range of tradable securities on this list. For investors who want global reach, this is the go-to platform.

Beyond its $0 stock and ETF commissions, Interactive Brokers stands out for its low margin rates, which are among the most competitive we've reviewed. That makes it a strong choice for margin traders looking to keep borrowing costs down.

For active traders, the desktop platform delivers advanced charting and technical analysis tools that few competitors can match. Whether you're a beginner opting for the Lite plan or a pro trader choosing the Pro plan, Interactive Brokers has a platform built to fit your needs.

Pros:

$0 online stock, mutual fund, and ETF commissions

Advanced trading platform

No minimum deposit

Access to global markets

Cons:

Complex platform may have a learning curve for beginners

Limited branch access

What it looks like:

Best for mutual funds: J.P. Morgan Self-Directed Investing

4.0/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

A no-frills platform with $0 mutual fund fees, J.P. Morgan Self-Directed Investing offers easy trading, an optional robo-advisor, and seamless Chase integration.

Earn a bonus up to $700 when you open and fund a J.P. Morgan Self-Directed Investing account (retirement or general) with qualifying new money by 7/22/2025.

On

J.P. Morgan Self-Directed Investing's

Secure Website.

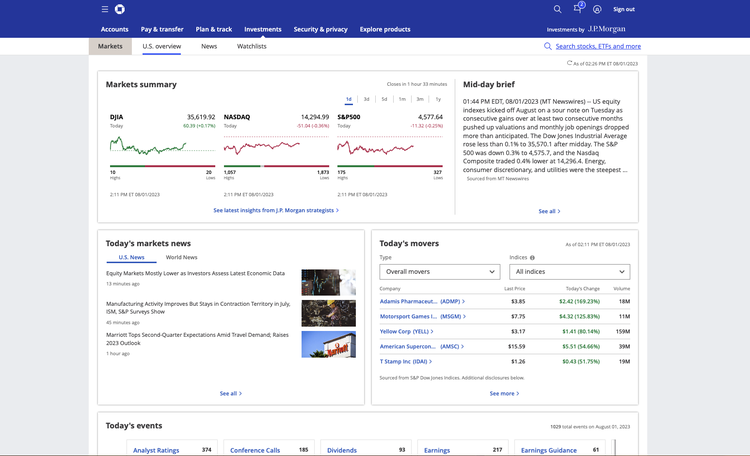

Why it made our list: J.P. Morgan Self-Directed Investing stands out with its $0 commission on all mutual funds -- a rarity in the brokerage world. Unlike many brokers that only offer commission-free trades on a limited selection of mutual funds, J.P. Morgan provides no-transaction-fee access across the board, making it one of the best brokers for mutual fund investors.

For Chase customers, the convenience factor is another key advantage. The platform integrates seamlessly with existing Chase accounts, allowing you to easily sign up for an investment account directly from the app. If you're already a Chase user, this integration makes getting started incredibly simple and efficient.

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

Vanguard is one of the best brokerages for passive investors who want to buy low-cost index fund ETFs. It also offers thousands of no-transaction-fee mutual funds, and excellent zero-commission options for buying stocks online, with no account minimums for brokerage accounts. Vanguard tries to keep its costs and expense ratios low so investors (like you) can keep more of your returns.

Why it made our list: Vanguard is a retirement-focused broker that's beloved by investors with a long-term, buy-and-hold strategy. If you're looking for a platform that aligns with this philosophy, Vanguard's simple and user-friendly interface makes it an excellent choice. However, it's not designed for active traders -- there are no real-time streaming news or advanced charting tools for those who prioritize short-term trading.

Where Vanguard truly shines is in its mutual funds. Vanguard's own suite of mutual funds is known for offering some of the lowest expense ratios in the industry, and it also gives you access to thousands of no-transaction-fee funds from other firms.

For investors who prefer a more passive investing approach and are focused on affordability and long-term growth, Vanguard is one of the best platforms to consider.

4.0/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

Public is an investing platform that simplifies trading stocks, bonds, ETFs, options, and crypto. With zero fees on many trades, Public stands out as a low-cost brokerage, while also providing yield-focused products to help you earn returns on your cash.

Why it made our list: Public stands out by offering a refreshing alternative to brokers like Robinhood that rely on payment for order flow (PFOF). Instead of relying on PFOF, Public charges customers upfront fees, eliminating any uncertainty around price execution.

But it's not just the pricing model that sets Public apart, it's the variety of investment options. While many brokers stick to the basics, Public goes beyond with access to stocks, ETFs, bonds, options, OTC stocks, and even cryptocurrencies. All of this is priced transparently and affordably.

If you're just getting started, Public makes it easy to invest with fractional shares, meaning you can begin investing at any price point -- perfect for beginners. If you want an investing platform that's clear, straightforward, and offers a diverse range of investments, Public is definitely worth checking out.

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

Webull is a standout mobile investing app. You can access advanced trading tools on desktop and mobile. Basic trades are commission-free, so it's competitive with similar apps. The mobile app offers Lite mode, a simpler interface for beginner investors. Consider opening a Webull account for its advanced toolset, more powerful than its closest competitors'.

Why it made our list: Webull is one of the best trading platforms for advanced traders on the go. It combines powerful charts, a customizable interface, and $0 commissions -- all within a mobile app. For those who want to get fancy with their trades from their phone, Webull is tough to beat.

One of its standout features is the lack of options contract fees -- a rarity in the industry, as most brokers charge per-contract fees for options. This makes Webull a great option for options traders looking to save on costs.

Additionally, Webull allows you to trade fractional shares, letting you buy stocks and ETFs for as little as $5, making it accessible for investors with smaller budgets. If you're looking for a feature-rich platform that doesn't break the bank, Webull is definitely worth a look.

Pros:

$0 stock and ETF commissions

No minimums

Advanced mobile platform

Competitive margin rates

Cons:

No mutual funds

Limited account types

First-hand review from one of our employees who usesWebullpersonally:

"I've had my Webull trading account for three years and primarily did my trading using my mobile device. I love that the app allows you to check your individual account's risk level based on your investments. Trading isn't too complicated on it, but beyond the risk assessment component, it was pretty similar to other platforms I've used. It could be worthwhile for people seeking to buy OTC and fractional shares."

5.0/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

Fidelity’s brokerage account offers free tools and $0 commission for online U.S. stock and ETF trades.* Investors can access a wide range of options, from stocks and mutual funds to crypto. Get an all-in-one view of live data and charts with the Fidelity Trading Dashboard, set up recurring investments, and enjoy 24/7 support from investing professionals. You can also potentially earn more on uninvested cash with a money market fund.**

Fees:

$0 commission for online U.S. stock and ETFs*. No account fees****.

Why it made our list: Fidelity has earned its place as one of the gold standards in the brokerage world, and for good reason. With decades of experience, millions of customers, and an undeniable reputation for reliability, it's easy to see why Fidelity is trusted by investors.

Fidelity offers a wide range of investment options, from stocks and ETFs to mutual funds, options, and even cryptocurrency. It matches the industry standard of $0 stock and ETF commissions but truly stands out with its 3,300-plus no-transaction-fee mutual funds, a feature only a select few brokers offer.

Beyond pricing, Fidelity shines with its extensive research tools -- more independent research than most discount brokers, making it ideal for investors who value data. Plus, it's packed with educational resources and offers fractional share trading, making it a great fit for beginners looking to grow their skills.

With its combination of low fees, comprehensive features, and stellar reputation, Fidelity checks all the boxes, especially for new investors who want to learn and build experience on one platform.

Pros:

Commission-free stock and ETF trades

Fractional share investing

Wide selection of mutual funds

Gold standard

Cons:

Uncompetitive options per-contract fees

First-hand review from one of our employees who usesFidelity personally:

"I've been using Fidelity for over a decade, and my experience has been excellent. I've found it to be an easy-to-use platform, has great customer service, and the fees are low or nonexistent. An underrated feature is the ability to change your core cash position to high-yielding options including a money market fund or a treasury fund. The yields on these funds are very attractive and it means you can feel comfortable keeping cash here that you're waiting to invest -- these funds currently earn a rate similar or higher than many high-yield savings account options. Note, you need to change your core cash position to one of these funds -- it is not automatic. These funds are not FDIC insured but I think they're pretty darn safe -- but if you want extra peace of mind, park your cash instead in an FDIC-insured high-yield savings account."

-Brendan Byrnes, Managing Director of Motley Fool Money

4.5/5

Our ratings are based on a 5 star scale.

5 stars equals Best.

4 stars equals Excellent.

3 stars equals Good.

2 stars equals Fair.

1 star equals Poor.

We want your money to work harder for you. Which is why our ratings are biased toward offers that deliver versatility while cutting out-of-pocket costs.

= Best

= Excellent

= Good

= Fair

= Poor

Bottom Line

Charles Schwab pioneered the low-cost brokerage model decades ago, and that legacy continues with its lineup of no-commission-fee offerings. The robust lineup of account types, investment vehicles, and high quality app round out the stacked feature set.

Fees:

$0 stock, ETF, and Schwab Mutual Fund OneSource® trades. No fees to buy fractional shares.

Why it made our list: Charles Schwab stands out as one of the best trading platforms due to its low-cost ETFs and index investing. Schwab's extensive marketplace includes its own line of branded ETFs, which rival the lowest-cost options from heavyweights like Vanguard and Fidelity -- making it a top choice for cost-conscious investors.

But Schwab offers more than just a trading platform. It's a comprehensive financial service provider, giving you access to a variety of account types, including the Schwab Bank Investor Checking™ account, CDs, and credit cards. For personalized help managing your accounts, Schwab also has over 300 branches across the country.

Whether you're looking to invest in low-cost funds or manage your banking and investment needs under one roof, Schwab offers a seamless experience for investors who want it all in one place.

Pros:

$0 commission trading

Many mutual funds

Investing and banking all in one

Nationwide branch network

Cons:

Uncompetitive margin rates

No cryptocurrency

First-hand review from one of our employees who usesCharles Schwabpersonally:

"I opened my Charles Schwab account as a brand-new investor who knew almost nothing about investing, and I've learned a lot through the educational resources available. While the website isn't the most modern, it's easy to use. I've spent a good amount of time using their customer service support as well as a Schwab Financial Consultant and both have been tremendously helpful. I like both the active trading experience but have also enjoyed using the robo-investing option, Schwab Intelligent Portfolios."

-Brooklyn Welch, Content Lead here at Motley Fool Money

Small deposits: To invest only a few hundred dollars at first, look for brokerage firms with no minimum deposit requirements.

Only the basics: To simply buy and hold stocks, you probably don't need a full-featured trading platform. Most discount brokers will meet your needs.

Mutual funds: To buy mutual funds, you should look for the best mutual fund brokers. These brokerage accounts make it cheap to buy and sell mutual funds.

Bonds and options: To trade bonds or options, or to make trades over the phone, look at what brokers charge for these activities. Compare the best investment brokers on our list to help you determine which platform has the features you're looking for.

One of the fastest ways to narrow down your options is to decide (1) what account type to open and (2) what investment types you'll need ahead of time. Many investors don't need bells and whistles, which can raise prices. But if you need it, you need it, and that's important.

Why brokerage size and growth matter for your investment decisions

Understanding the largest and fastest-growing brokerage firms is crucial when selecting the right platform for your investments. Firms like Charles Schwab, Vanguard, and Fidelity lead the market with trillions in assets and millions of active accounts, offering stability and a broad range of services. For investors seeking reliability, these well-established brokers provide a solid foundation.

On the other hand, newer platforms like Robinhood and Coinbase are revolutionizing the industry with low fees and access to cryptocurrencies, appealing to a more tech-savvy audience.

Opening an online brokerage account is usually quick and straightforward.

Determine what type of brokerage account you need (individual, IRA, etc.).

Compare brokers to find the best fit for you.

Fill out the new account application. Be ready to provide identifying information, such as your Social Security number.

Add funds to your account. Most brokers offer several ways to do this.

Start investing!

You can get started investing by opening a brokerage account, depositing money via the trading platform, and using your deposit to buy and sell stocks. Most online brokers let you open an account for free. Some require a deposit upon opening, and you can use this deposit to trade.

You can learn about stocks from brokers that offer educational articles and videos, or you can download financial literacy apps. The latter tend to offer bite-sized lessons on money. It's an easy way to learn without taking classes in-person. Plus, it's structured.

Online brokers typically let you buy stocks and ETFs. Beyond that, choices vary.

What you can buy:

Bonds: A bond is essentially a loan that an investor provides to a borrower, which can be a government, municipality, or corporation. They pay you fixed interest.

Mutual funds: A mutual fund is a type of investment that pools money from many investors to purchase a diverse portfolio of stocks, bonds, or other securities.

Stock options: Stock options are financial contracts that give the buyer the right, but not the obligation, to buy (call options) or sell (put options) a specific stock at a predetermined price (strike price) within a set time frame (expiration date).

Some brokers let you trade alternative investments, a catch-all category for niche categories. Investments under this umbrella might include music royalties and venture funds open to non-accredited investors.

You can start trading with as little as $1. Most brokers on this list will let you open an account without depositing any money. To buy a stock, you'll need at least $1. Brokerages that offer fractional shares let you buy pieces of stocks for $1 or $5, minimum.

If your broker only offers full shares, you'll need enough deposited to buy your desired stock at full price. Stock prices range widely, from under $1 to over $1,000 per share.

Yes, your online broker is safe from collapse. If your brokerage firm is a member of the Securities Investor Protection Corporation (SIPC), then cash and securities in your account are protected from loss due to broker failure, up to $500,000 ($250,000 for cash).

The SIPC doesn't cover risks like unauthorized trading activity, but most of the best brokerage accounts have fraud protection that covers you if your account is hacked. The trick is letting your brokerage know ASAP.

Your money is not insured against investments losing value. Losing money to stock values going down is a risk inherent to stock trading. Day trading is especially risky.

An online broker helps you buy and sell stocks. Typically, you do this through the broker's online trading platform.

You can think of an online stock broker as a direct line to stock exchanges. In exchange for a tiny commission on every trade, the broker sends your orders on to stock exchanges and market makers. These market makers do the heavy lifting of matching your buy orders with someone who wants to sell, or vice versa.

Your online broker tracks what stocks you own and at what prices you trade them. Mostly, this is done through discount brokers.

Discount brokers

Online brokerages are discount brokers. They aren't in the business of giving you advice or suggesting stock picks. Instead, discount brokers focus on the very basic service of helping you buy or sell a stock (or other type of investment) from the convenience of your own home.

Discount brokers, or online brokers, are popular because they're more affordable than full-service brokers.

Full-service brokers

Brokerage firms we label "full-service brokers" are more closely related to the stock brokers of the olden days. Full-service brokers employ human brokers who help you trade, choose mutual funds, or create a retirement plan.

Full-service brokers are costly, since people are more expensive than computers. A popular full-service broker charges at least $75 to place a stock trade, and that can jump to as high as $500 or more to buy a large amount of stock.

TIP

Buying your first stocks: Do it the smart way

Once you’ve chosen one of our top-rated brokers, you need to make sure you’re buying the right stocks. We think there’s no better place to start than with Stock Advisor, the flagship stock-picking service of our company, The Motley Fool. You’ll get two new stock picks every month, plus 10 starter stocks and best buys now. The average stock pick inside Stock Advisor is up 1002% — more than 5x that of the S&P 500! (as of 6/9/2025). Learn more and get started today with a special new member discount.

Brokerages we monitor

Brokerages we evaluated for consideration on this page:

Acorns, Ally Invest, Axos Self-Directed Trading, Betterment, Cash App Investing, Charles Schwab, Delphia, Domain Money, Ellevest, Empower, eToro Brokerage, E*TRADE Core Portfolios from Morgan Stanley, E*TRADE from Morgan Stanley, Fidelity, Fidelity Cash Management, Fidelity Go®, Firstrade, FOREX.com, Interactive Brokers, J.P. Morgan Self-Directed Investing, M1 Finance, Magnifi, Marcus Invest, Merrill Edge® Self-Directed, Moomoo, NinjaTrader, Personal Capital, Plynk, Prosperi Academy, Public, Robinhood, Rocket Dollar, Schwab Intelligent Portfolios, SoFi Active Investing, SoFi Robo Investing, Stash, Stockpile, tastytrade, Titan, Tornado App, TradeStation, Tradier, Vanguard, Vanguard Digital Advisor®, Wealthfront, Webull, Zacks Trade.

FAQs

Most online brokers don't charge commissions for online stock trades. However, there may be commissions for other types of investments like mutual funds and options, and brokers have their own fee schedules for various other services. The best pick for you depends on what services and investments you anticipate using the most.

Thanks to zero-commission online stock trading and many brokerage firms offering fractional shares, it's easier than ever to diversify your investments. If your goal is to create a diverse portfolio of individual stocks without a large upfront capital commitment, be sure the broker you choose has both of these features.

Yes. If your account is with a brokerage firm that is a member of the Securities Investor Protection Corporation (SIPC), cash and securities in your account are protected from loss due to broker failure, up to $500,000 ($250,000 for cash). However, your money is not insured against losses that result from declines in value of the investments in your account.

This depends on your goals. If you simply want the best platform to buy and sell stocks, a standard (taxable) brokerage account could be the best choice for you. If you want to save for retirement and/or reduce your taxes, a retirement account like a traditional or Roth IRA might be better. There are other specialized brokerage account types as well, and you can usually find a list of the types offered on your broker's website.

There's no broker that is inherently safer than all the rest, but there are some important things to look for. First, make sure your broker is covered by SIPC protection, which insures the cash and securities in your account in the event of a broker's failure. Second, make sure your broker has a fraud protection guarantee, which will make you whole in the event that someone hacks into your account and makes unauthorized trades or withdrawals.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. Motley Fool Money does not cover all offers on the market. Motley Fool Money is 100% owned and operated by The Motley Fool. Our knowledgeable team of personal finance editors and analysts are employed by The Motley Fool and held to the same set of publishing standards and editorial integrity while maintaining professional separation from the analysts and editors on other Motley Fool brands.

Terms may apply to offers listed on this page.

SoFi IRA disclosure:

Terms and conditions apply. Roll over a minimum of $20K to receive the 1% match offer. Matches on contributions are made up to the annual limits.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Bank of America is an advertising partner of Motley Fool Money. JPMorgan Chase is an advertising partner of Motley Fool Money. Charles Schwab is an advertising partner of Motley Fool Money. Ally is an advertising partner of Motley Fool Money. Brendan Byrnes has positions in Amazon and Apple. The Motley Fool has positions in and recommends Amazon, Apple, Axos Financial, Bank of America, Best Buy, Interactive Brokers Group, Intuit, JPMorgan Chase, Maker, Target, and XRP. The Motley Fool recommends Charles Schwab and Flow and recommends the following options: long January 2027 $175 calls on Interactive Brokers Group, short January 2027 $185 calls on Interactive Brokers Group, and short June 2025 $85 calls on Charles Schwab. The Motley Fool has a disclosure policy.

Robinhood Disclosure:

Robinhood disclosure

All investments involve risk and loss of principal is possible.

Securities are offered through Robinhood Financial LLC, member FINRA/SIPC. Cryptocurrency services are offered through an account with Robinhood Crypto, LLC (NMLS ID 1702840). Robinhood Crypto is licensed to engage in virtual currency business activity by the New York State Department of Financial Services. Cryptocurrency held through Robinhood Crypto is not FDIC insured or SIPC protected. For more information see the Robinhood Crypto Risk Disclosure.

Trades of stocks, ETFs and options are commission-free at Robinhood Financial LLC. Other fees may apply. Please see Robinhood Financial’s Fee Schedule to learn more.

Fractional shares are illiquid outside of Robinhood and are not transferable. Not all securities available through Robinhood are eligible for fractional share orders. For a complete explanation of conditions, restrictions and limitations associated with fractional shares, see the Fractional Shares section of our Customer Agreement.

Robinhood Gold is an account offering premium services available for a $5 monthly fee. Not all investors will be eligible to trade on Margin. Margin investing involves the risk of greater investment losses. Additional interest charges may apply depending on the amount of margin used. Bigger Instant Deposits are only available if your Instant Deposits status is in good standing.

Investing is risky. Bonus offers subject to terms and conditions, visit robinhood.com/hoodweek for more information. Margin is not suitable for all investors. Robinhood Gold is offered through Robinhood Gold LLC and is a subscription offering services for a fee. Brokerage services offered through Robinhood Financial LLC (member SIPC), a registered broker dealer.

E*TRADE from Morgan Stanley Disclosure:

E*TRADE services are available just to U.S. residents.

Interactive Brokers Disclosure:

Interactive Brokers disclosure: The inclusion of Interactive Brokers’ (IBKR) name, logo or weblinks is present pursuant to an advertising arrangement only. IBKR is not a contributor, reviewer, provider or sponsor of content published on this site, and is not responsible for the accuracy of any products or services discussed.

J.P. Morgan Self-Directed Investing Disclosure:

J.P Morgan Disclosure INVESTMENT AND INSURANCE PRODUCTS ARE: NOT A DEPOSIT • NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

Vanguard Disclosure:

Vanguard disclosures

Visit vanguard.com to obtain a prospectus or, if available, a summary prospectus, for Vanguard and non-Vanguard funds offered through Vanguard Brokerage Services. The prospectus contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

Commission-free trading of Vanguard ETFs applies to trades placed both online and by phone. All ETFs are subject to management fees and expenses; refer to each ETF's prospectus for more information. Account service fees may also apply. All ETF sales are subject to a securities transaction fee. See the Vanguard Brokerage Services commission and fee schedules for full details.

Vanguard funds not held in a brokerage account are held by The Vanguard Group, Inc., and are not protected by SIPC. Brokerage assets are held by Vanguard Brokerage Services, a division of Vanguard Marketing Corporation, member FINRA and SIPC.

Vanguard Marketing Corporation, Distributor of the Vanguard Funds

Fidelity Disclosure:

Fidelity disclosure Investing involves risk, including risk of loss

* - $0.00 commission applies to online U.S. equity trades and exchange-traded funds (ETFs) in a Fidelity retail account only for Fidelity Brokerage Services LLC retail clients. Sell orders are subject to an activity assessment fee (historically from $0.01 to $0.03 per $1,000 of principal). Other exclusions and conditions may apply. A limited number of ETFs are subject to a transaction-based service fee of $100. See full list at (https://www.fidelity.com/trading/commissions-margin-rates). Employee equity compensation transactions and accounts managed by advisors or intermediaries through Fidelity Institutional® are subject to different commission schedules.

Fidelity Crypto® is offered by Fidelity Digital Assets®. Investing involves risk, including risk of total loss. Crypto as an asset class is highly volatile, can become illiquid at any time, and is for investors with a high risk tolerance. Crypto may also be more susceptible to market manipulation than securities. Crypto is not insured by the Federal Deposit Insurance Corporation or the Securities Investor Protection Corporation. Investors in crypto do not benefit from the same regulatory protections applicable to registered securities. Fidelity Crypto® accounts and custody and trading of crypto in such accounts are provided by Fidelity Digital Asset Services, LLC, which is chartered as a limited purpose trust company by the New York State Department of Financial Services to engage in virtual currency business (NMLS ID 1773897). Brokerage services in support of securities trading are provided by Fidelity Brokerage Services LLC (“FBS”), and related custody services are provided by National Financial Services LLC (“NFS”), each a registered broker-dealer and member NYSE and SIPC. Neither FBS nor NFS offer crypto as a direct investment nor provide trading or custody services for such assets. Fidelity Crypto and Fidelity Digital Assets are registered service marks of FMR LLC.

***Options trading entails significant risk and is not appropriate for all investors. Certain complex options strategies carry additional risk. Before trading options, please read (https://www.theocc.com/Company-Information/Documents-and-Archives/Options-Disclosure-Document). Supporting documentation for any claims, if applicable, will be furnished upon request. ****Zero account minimums and zero account fees apply to retail brokerage accounts only. Expenses charged by investments (e.g., funds, managed accounts, and certain HSAs) and commissions, interest charges, or other expenses for transactions may still apply. See (https://www.fidelity.com/trading/commissions-margin-rates) for further details.

Motley Fool Money is a Motley Fool service that rates and reviews essential products for your everyday money matters.