Corporate profits are on many investors' minds as we enter the final weeks of the fiscal year. Whether it's sector-specific bad news or a general warning that profits have peaked, it's hard to escape bearish oracles predicting an imminent earnings recession. Let's not panic just yet. Corporate profits are one of the most important macroeconomic indicators we have, but there are so many moving parts inside the countrywide "corporate profits" data point that a deeper dive is almost required if we're to understand it. You might find, once you get under the water, that things aren't quite as scary as you thought.

Defining profits

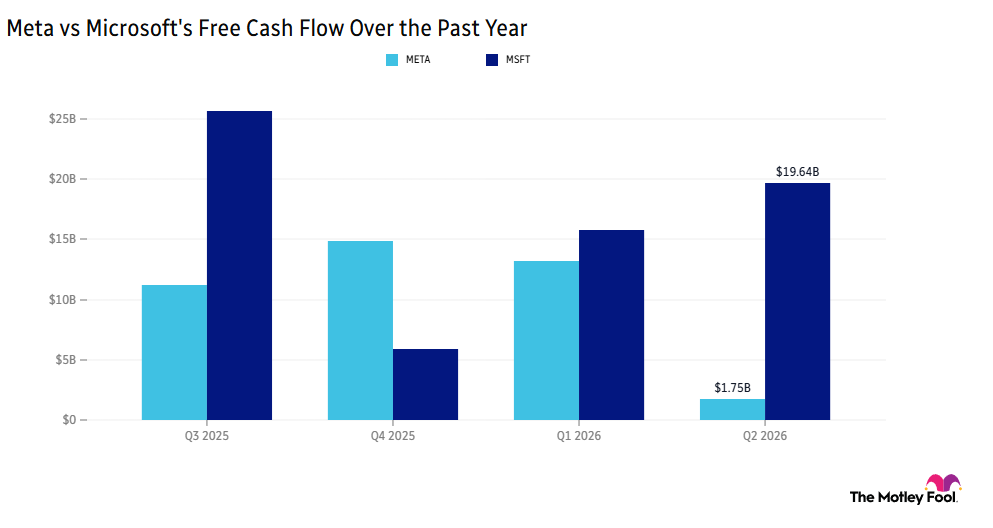

Any investor who has spent time digging through more than a few earnings reports knows just how much variety there is in a typical income statement. All you have to do is examine some recent high-profile filings.

Microsoft (MSFT -0.71%) had a multibillion-dollar write-off in its second quarter and a year-over-year drop in its latest quarter thanks to deferred revenue. Chipotle (CMG +2.18%) and McDonald's (MCD -0.55%) both led off the fast-food sector with unexpectedly weak reports, both of which are largely the result of macroeconomic forces beyond their control. A smaller company with significant revenue from government contracting revenue, such as iRobot (IRBT +0.00%), can have significant quarter-to-quarter earnings volatility as it handles the contrasting needs of the military and the moms who use its robotic vacuums. Each of these companies has its own unique way of handling standard accounting practices to arrive at a final profit total.

Government economic agencies are no different, but we can hope that a greater breadth of data will help smooth out the variability that crops up in individual companies' earnings. The Federal Reserve Bank of St. Louis prefers to use after-tax corporate profits in its data service, while the Bureau of Economic Analysis offers profits before taxes, with inventory valuation adjustments. Examining both on the same scale allows us to get a rough idea of the taxes paid by American corporations:

Source: Federal Reserve of St. Louis; Bureau of Economic Analysis.

Both pre-tax and after-tax profits have moved in tandem since 1980, but as the profit pool grows larger, companies are keeping more and more of their earnings. Subtracting FRED's (the St. Louis Fed's nickname for its online economic-data repository) post-tax statistics from the BEA's pre-tax figure gives us a very rough idea of the tax burden borne by American businesses. After peaking in the mid-80's, corporate tax payments as a percentage of profits steadily declined for more than two decades from a peak of nearly 50% for one quarter in 1986 to a 22% tax rate today. Of course, this isn't a definitive explanation of corporate tax rates, but simply a back-of-the-envelope calculation based on these two statistics.

Where does the money come from?

For most of our dive, we'll be using the BEA's pre-tax number, which it claims is "the best available measure of industry profits." Now that we've seen the difference between pre- and post-tax profit, let's take a look at where those profits come from. We've got three primary options: domestic nonfinancial businesses, the financial industry, and overseas profits.

Source: Bureau of Economic Analysis.

The financial sector and international sales take up a progressively larger amount of the total profit pie as we move closer to the present. In 1980, financial and international sources contributed 16% and 18% to the total U.S. corporate profit pool, respectively. That amount has grown, but perhaps not as much as you might think: Financial and international profits made up 21% each of all profit earned by American businesses in the most recent quarter.

Both have been responsible for much larger pieces of the pie at various points. The financial industry earned as much as 35% of all corporate profits in the first two years years after the dot-com bubble burst, and international sources contributed more than 30% of the profit during the early stages of the housing crash. The American economy's ability to activate other profit engines when its main domestic motor needs repair has helped fend off the worst of all possible outcomes more than once.

For further proof of this, let's look at how domestic and international profits have risen and fallen through several recessions.

Source: Bureau of Economic Analysis.

This graph is a bit busy, but you can see several instances where international profits remained stronger through recessions than domestic profits. It's particularly interesting to note a major spike in overseas profits right as the housing bust triggered a recession. Domestic profits had already been falling for some time before the official start of the recession, which seems to be the case for all previous recessions on this graph as well. While the existence of a domestic profit spike doesn't preclude a recession (especially if Washington remains dysfunctional), the jagged rise in domestic profits heading into the current quarter makes it seem far less likely than the bears would have you believe.

Business cycles

The way we measure growth can affect our results. Using a year-over-year calculation might show an economy roaring ahead, while sequential changes could more accurately show the subtle peaks and valleys of the business cycle. Let's take a look:

Source: Bureau of Economic Analysis.

Quarter-to-quarter changes in corporate profit certainly suffer far less volatility than the wildly erratic year-over-year measures. However, it does appear that expansions and contractions follow the same pattern, whether it's sequential or year-over-year. It's worth pointing out that large drops in year-over-year profitability tend to be easier to identify as lead-ins to a contraction, but that's not always the case. The U.S. economy had its fair share of problems in the mid-'80s, but weak corporate profitability around the time of 1987's Black Monday didn't herald the onset of a recession the same way that it did in 1990. Unfortunately, declining corporate profits aren't always obvious warning signs that investors should make a profitable exit.

We've looked at corporate profits in isolation. Now let's take a look at the bigger picture. How much do corporate profits contribute to the overall U.S. economy?

Source: Federal Reserve of St. Louis.

Corporate profits, whether before or after taxes, are a smaller part of the American economy than many people think. Wages and salaries for millions of American workers have always been a far larger part of GDP. The size of the economy in this chart can mask what's really happening, though. Over the last 32 years, the American worker has taken home less of the economic pie, and the American corporation has taken more:

Source: Federal Reserve of St. Louis.

The trend is subtle but unmistakable. If wages were still as large a percentage of the economy as they were in 1980, American workers would be taking home $755 billion more each year. That makes most tax-cut proposals look positively puny by comparison; a recent proposal to extend the Bush tax cuts for one year was estimated to reduce government revenue (and thus increase the cash available to American citizens) by $210 billion. On the other hand, reverting corporate profits back to 1980's level would reduce the overall profit pool by $620 billion.

Nothing can continue upward in a straight line forever, so it's natural to expect record-high levels of corporate profitability to eventually decline. It's more important to ponder what will happen after corporate profits recover from this hypothetical drop somewhere down the line. Will the rebound look like the sudden booms of the past, or are American businesses starting to reach the limits of their profitability? Let me know your thoughts with a comment.