Lockheed Martin's F-35 program could boost revenue over the next few years. Source: Lockheed Martin.

Lockheed Martin (LMT 0.48%) investors were apprehensive heading into the first-quarter-earnings report, as the Pentagon's top supplier was looking at declining revenue amid extensive government defense budget cuts. While revenue did indeed decline, Lockheed Martin's net earnings jumped 23% in the first quarter. Let's dig deeper to see if the increase in profitability is as good as it seems.

By the numbers

Starting from the top line, Lockheed Martin's first-quarter net sales declined 4% to $10.7 billion, year over year, but net earnings bucked the trend and jumped 23% to $933 million, or $2.87 per diluted share. That compares to first-quarter 2013 net earnings of $761 million, or $2.33 per diluted share.

A big reason for the earnings increase was the swing in Lockheed Martin's pension fund, which posted income of $86 million that increased first-quarter earnings by $53 million, or $0.16 per share. The corresponding quarter last year recorded a pension expense of $121 million, which reduced earnings by $75 million, or $0.23 per diluted share. That's a $0.39 per share swing between the comparable first quarters.

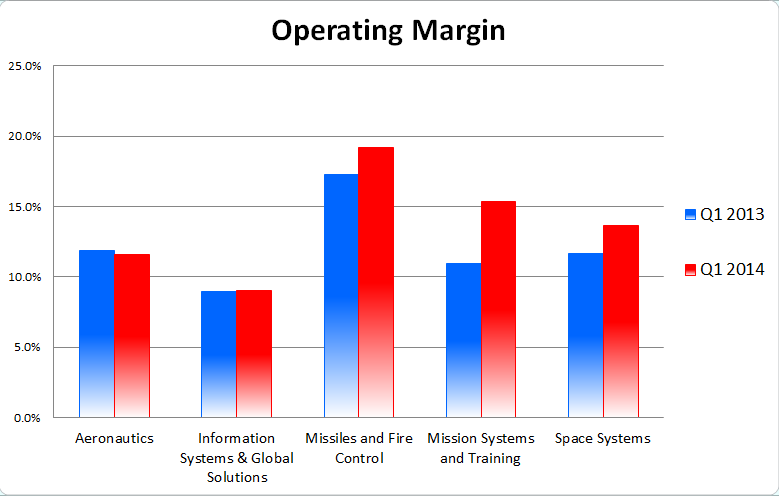

While the rise in discount rates caused its pension fund to inflate earnings this quarter, there's still good news in Lockheed Martin's core business. Consider that while revenue declined, operating margins improved in four out of its five business segments, and some increased significantly.

Graph by author. Source: Lockheed Martin Corporation's Q1 press release

Looking ahead

Lockheed Martin expects income from its pension fund to continue to be positive throughout the year. With margins improving, it also raised its earnings guidance for 2014. It projects earnings per share for the full year to come in between $10.50 and $10.80, which is a $0.25 increase from its January forecast. Sales are expected to remain flat, and the contractor confirmed its earlier forecast for $44 billion-$45.5 billion in sales for 2014.

Some short-term catalysts could boost revenue. Lockheed Martin expects international sales to help offset the revenue decline in the U.S. Also, the defense contractor expects to close some large deals for its F-35 fighter jet, though it isn't likely to happen in 2014. The F-35, which has become the company's largest program, is projected in 2014 to account for roughly 16% of Lockheed's revenue; it's expected to represent about 25% by 2018 or 2019. As a bonus for Lockheed Martin investors, the Pentagon has previously said it will strive to shield the F-35 from budget cuts.

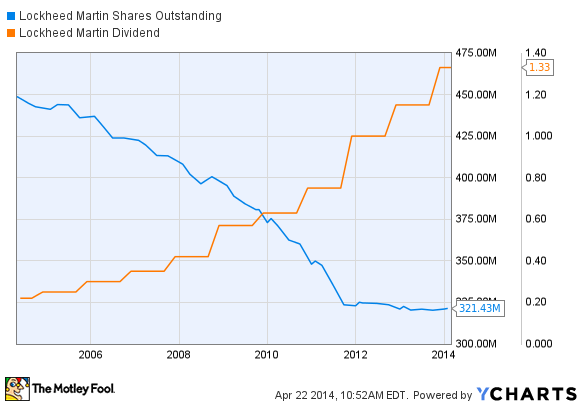

While investors will have to be patient to see revenue increases from the F-35 program, Lockheed Martin is poised to return value to shareholders in other ways.

Source: YCharts

As you can see above, the company has proven it can consistently return value to shareholders by growing its dividend and reducing shares outstanding. That held true in the first quarter as Lockheed Martin repurchased 7 million shares for $1.1 billion, which compares favorably to the 5.1 million shares bought for $461 million in last year's first quarter. It also paid cash dividends of $444 million in the quarter, compared to $371 million last year.