El Paso Pipeline Partners (EPB +0.00%) is a limited partnership. That means that it distributes most of its cash to shareholders and thus must issue shares and debt to fund growth. The January announcement that distribution growth would stall in 2014 led to a unit price drop and made growth more expensive.

Double-edged sword

In the investing world, there aren't too many options where shareholders get to vote on a company's investments. Limited partnerships (LPs), like real estate investment trusts (REITs), are one of those rare breeds. That's good news on one hand, because there's a very public review of a company's prospects. However, the market can be more popularity contest than weighing machine over short periods of time. That can put solid LPs, REITs, and similarly distribution focused companies in a bind when prices decline.

Why is this? Because the cost of funding expansion and acquisition efforts goes up. For example, Linn Energy (NASDAQ: LINE) was in the process of buying Berry Petroleum last year when the company's accounting was publicly questioned by a prominent financial publication. That helped lead to regulators taking an informal look at the company.

The market doesn't like uncertainty, and Linn Energy and its sibling LinnCo (NASDAQ: LNCO) sold off. But the company was in the midst of a deal. To get it done, LinnCo had to up the number of shares it issued in the transaction by 34%. That's a huge increase in cost and turned a really good price into, well, a less good price.

The deal has been consummated, but Linn and LinnCo's shares have yet to fully recover. Although the company continues to expand, the cost of this expansion is higher now than it was a year ago. The added dilution from upping the unit count in the Berry acquisition is clear evidence of that. Although Linn and LinnCo are technically limited liability companies, they function in much the same way as an LP, and because of the timing of this deal they offer a striking example of the problem that distribution-focused companies face.

Situational

If a unit price decline is related to a broad market sell-off, you understand. Every industry player has to deal with it. However, when it's just one company facing company-specific issues, then it becomes a problem. That's the case at Linn and LinnCo. It's also the case at El Paso Pipeline Partners.

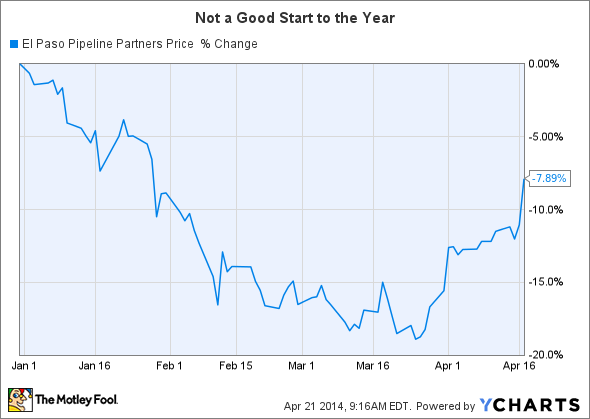

El Paso Pipeline Partners had been regularly increasing its distribution each quarter since 2008. That stopped in the first quarter of 2014 when the company kept the payout at $0.65 a unit. It announced that the distribution would remain at that level for the entire year. While that will still mean a 2% year-over-year increase, the decision to stop increasing each quarter wasn't taken well by investors.

The shares are down around 8% so far this year, and more than 20% over the trailing 12 months. Worse, El Paso is buying several assets from its general partner this year. Shares issued to the general partner (GP) will account for about $97.2 million of the $2 billion price tag. A year ago that would have meant 20% fewer shares.

And, even more shares are likely to be sold to the public to help pay for this deal, which will require nearly $1 billion in funds to get done (roughly half of the deal's value is debt that El Paso is assuming from its GP). With 20% more units needed to pay for this deal, it will be that much more expensive to increase the distribution. The problem, of course, is that investors are likely to be concerned about El Paso Pipeline Partners' prospects until distribution growth resumes. You see the quagmire.

When growth resumes...

Still, El Paso is far from a bad company. And with the new drop downs expected it's still growing its portfolio of assets. So, it's highly likely that this is a pause and not the precursor of a distribution cut. That's particularly true since El Paso is a part of the Kinder Morgan family of companies—one of the largest players in the midstream space.

More aggressive investors willing to take a chance on a turnaround should consider El Paso Pipeline and its 8% yield. The same is true of Linn (10% yield) and LinnCo (10.4%) in the drilling space. But keep a close eye on growth plans and, just as importantly, share issuance plans.