The Dow Jones Industrials (^DJI +1.03%) celebrated another milestone this week, climbing above the 17,000 level for the first time ever. When you consider that the Dow was well below 7,000 when the bull market began in March 2009, the Dow's 10,000-point ascent carries even more weight. Yet shockingly, this huge recovery in the Dow's fortunes has come without dividend investors having had to pay the price of lower yields. The reason: dividend payments among Dow stocks have amazingly kept pace with the stock market's gains.

The Dow's dividend strength

The Dow has always been well-known for rewarding dividend investors with dependable quarterly payments from its components. Although it hasn't always been the case, the current slate of 30 Dow components all pay quarterly dividends, and all but half a dozen of them pay respectable yields of 2% or more. When you take the average yield of all 30 Dow components -- weighted not by their respective share prices but merely as an overall mean -- the Dow currently sports a 2.56% yield.

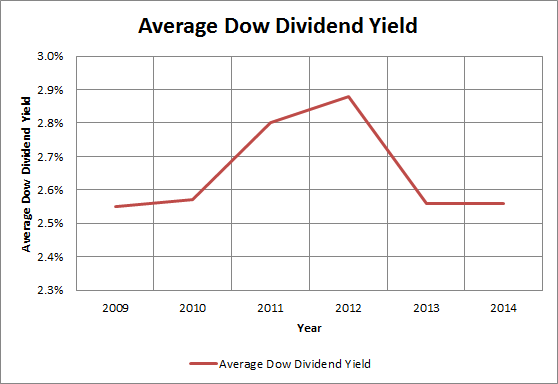

With the Dow having soared so far in recent years, you'd think that this yield would be far below past levels. But as you can see below, the Dow's average dividend yield has stayed remarkably constant over the past five years:

Data source: Dogs of the Dow.

The obvious question is how the Dow Jones Industrials have been so successful at sustaining a strong dividend yield. Two contributing factors have played the biggest role in keeping Dow dividend yields high.

How the Dow kept dividend investors happy

First, most of the Dow's component stocks have done a good job of boosting their dividends since the end of the financial crisis. Disney (DIS +2.33%) isn't the perfect example of an ideal Dow dividend stock, as its yield has been stubbornly stuck at the 1% level for years. But given that the stock has jumped 150% since the end of 2009, even holding its dividend yield steady means an equal jump in its annual dividend payment over that timeframe.

Other Dow stocks have managed to increase their dividend yields over the past five years. Cisco Systems (CSCO +0.88%) just started paying a dividend in 2011, but it now yields a healthy 3%. Oil giant ExxonMobil (XOM -0.87%) has historically rewarded shareholders with both high dividends and big share buybacks, and its yield has increased by a quarter percentage point in five years despite seeing impressive share-price gains.

But the other aspect that has helped the Dow's average dividend yield rise has been smart replacements of stocks that weren't making the dividend grade. The replacement of Citigroup and General Motors in 2009 eliminated two stocks that weren't paying any dividends at all, and Alcoa's and Bank of America's (BAC +0.77%) removal from the Dow last year also took out stocks with subpar yields. Their replacements haven't always been big dividend payers, but as Cisco's experience shows, the new Dow components have plenty of potential for future dividend growth.

Yield isn't the end-all be-all for dividend investors, but it's still impressive that despite its huge rise, the Dow Jones Industrials have still managed to sustain their average dividend yields. That experience should give Dow investors confidence that even if the Dow's gains start to slow, dividends will continue to play a vital role in the total return investors earn from their portfolios.