The painting and coatings sector is an interesting sector in 2016, not least because there is a large amount of differentiation between the end-market exposure of the leading companies. Let's look at the leading U.S.-listed companies and shed some light on which is the most attractive for 2016.

Valuations

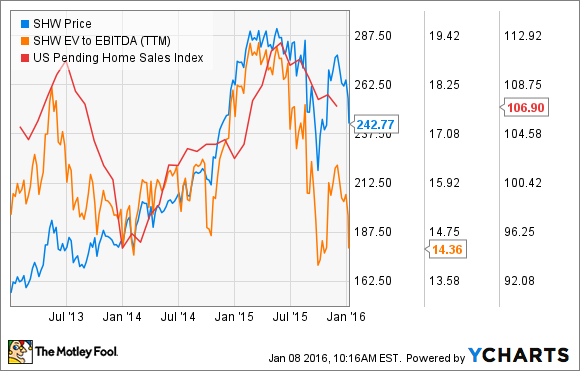

Before delving into end-market details, let's start with a look at past performance and valuations for the four stocks we'll look at. A chart of stock price movements in the past two years shows how The Sherwin-Williams Company (SHW 0.54%) and, to a lesser extent, The Valspar Corporation (VAL) have outperformed the stagnating PPG Industries, Inc. (PPG 0.72%) and RPM International Inc. (RPM 0.46%).

A look at valuations shows that Sherwin-Williams remains the most expensive, but the valuation gap has closed. Incidentally, I'm using enterprise value (market cap plus net debt) over earnings before interest, tax, depreciation, and amortization, or EBITDA, because it's a good way to compare companies with different debt levels.

SHW EV to EBITDA (Forward) data by YCharts.

Sherwin-Williams and PPG Industries

Sherwin-Williams is often seen as a play on U.S. housing in particular. For example, the company generated 72% of its segmental profit (before administrative costs) from its Paint Stores Group in the first nine months of 2015, with its Consumer Group (wood finishes, water sealants, and such) contributing 17%. The U.S housing market has been a pretty good investment theme in recent years, and it's no surprise that Sherwin-Williams commands a premium in the sector.

However, as soon as leading indicators of the housing market started to fall -- in this case, pending home sales -- the stock price and valuation came under pressure.

In contrast, PPG Industries is more of a global play on a few key industries, most notably construction and automotive.

DATA SOURCE: PPG INDUSTRIES PRESENTATIONS.

While U.S. construction looks like a good place to be in 2016, and the global automotive industry remains in good shape -- albeit with fears concerning the sustainability of China's car sales growth -- there are potential headwinds for PPG for two main reasons:

- PPG generates only 44% of its revenue from the U.S. and Canada, and 26% from Asia-Pacific and Latin America, giving it significant exposure to emerging markets that have disappointed with growth recently.

- 50% of its coatings revenue (responsible for 93% of its total revenue) comes from the original equipment manufacturer marketplace, giving it significant cyclical exposure.

In other words, if the global industrial economy turns down, then PPG industries is likely to be hit disproportionately.

Valspar and RPM International

Vaspar generates around 57% of its revenue from coatings and around 38% from paints. Valspar is interesting because of its relatively high packaging exposure -- a relatively safe industry that makes up nearly 20% of total company revenue -- but it also has around 17% of its revenue coming from General Industrial.

A quick look at its full-year earnings reveals flat sales (excluding currency effects) for packaging, but General Industrial sales rose by mid-single digits. Given that General Industrial sales go into end markets such as heavy machinery, transportation, and infrastructure -- all industries under pressure -- it's hard to see how this kind of growth can continue.

Turning to paints, 21% of total company revenue comes from paints in the U.S., and the company struggled with the volume declines at Lowe's following the latter's decision in late 2014 to sell Sherwin-Williams house paint.

IMAGE SOURCE: PPG INDUSTRIES PRESENTATIONS.

RPM International is the smallest but most interesting company on the list. Generating 70% of its 2015 revenue from repairs and maintenance means it's less cyclically exposed than PPG Industries, while its valuation is at a discount to Sherwin-Williams. It's also primarily a U.S. company, with around 70% of its revenue coming domestically and only a combined 8.1% coming from Latin America and Asia-Pacific.

Moreover, the company recently reported a solid set of second-quarter results, with management forecasting growth in all three segments for the remainder of its fiscal year.

| Segment | Share of Q2 Growth | Outlook for Rest of Year |

|---|---|---|

| Industrial | 52.7% | flat to up slightly |

| Consumer | 31.6% | up mid-single digits |

| Specialty | 16.1% | mid-to-upper single digits |

DATA SOURCE: RPM INTERNATIONAL PRESENTATIONS.

The takeaway

All told, if you want cyclical exposure, then PPG Industries is the pick, while Sherwin-Williams is the play if you want exposure to U.S. housing, but it comes with a premium. Valspar has potential challenges with its industrial end markets, and its paint sales need to recover. Given the current economic environment, RPM International looks best placed in terms of valuation and end-market exposure.