There's no way around the obvious: Investors weren't pleased with Alcoa's (NYSE: AA) fourth-quarter earnings, sending the shares down roughly 26% in January. A good portion of the monthly decline led up to and following directly after the Jan. 11 earnings release. But was it as bad as all that? The company's top brass doesn't think so.

Alcoa Logo. Source: Alcoa.

OK, it wasn't the best quarter

CFO William Oplinger's lead-off statement summed up a part of what spooked investors:

Fourth-quarter 2015 revenue totaled $5.2 billion, down approximately 18% year over year. Growth from the recent acquisitions and aerospace volume was offset by lower alumina and metal pricing, unfavorable currency, and the impact of divested and closed businesses.

That's the big picture. The more worrisome problem was underneath that number. Alcoa's crown jewel, its Value Add business which makes high-end parts out of aluminum and other metals, saw revenues decline 3% sequentially from the third quarter. After-tax operating income at the group was down 16% and adjusted EBITDA was lower by nearly 12%.

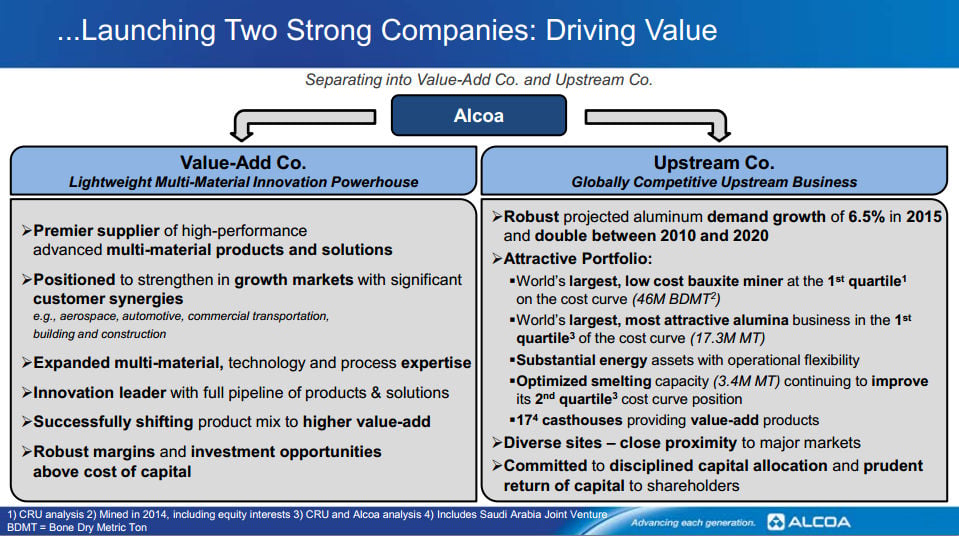

By the end of 2016, this business is supposed to be broken off from the the Upstream segment. Upstream has to deal with a tough commodity market, so investors anticipated weakness there and got it. But Value Add is expected to be a higher-growth business -- only the fourth quarter didn't show that. No wonder sentiment soured.

It's all about the aerospace

While investors might have grown concerned about Value Add's future, that's probably shortsighted. In fact, giant businesses such as Boeing and General Electric don't seem too concerned about the aluminum giant and have entered into long-term contracts with its Value Add division.CEO Klaus Kleinfeld happily reported:

We've seen three major multi-year aero contracts in the fourth quarter alone, roughly a value of $4 billion, but in the whole year it's been $9 billion of long-term contracts in aerospace. That's more than twice the volume of the year before.

Boeing and GE were two of the three deals, the other was Airbus. Products ranged from fasteners to engine parts, and the deals suggest a bright future for Value Add's largest business at around 40% of the segment's revenues. So things may not be as bad as investors fear based on a single quarter in what remains a transition period.

Upstream is healing

The upstream business actually had some positives, too. For example, Kleinfeld explained that, "Upstream business in total $2.4 billion of revenues and $239 million of adjusted EBITDA. It's been profitable despite lower alumina." With aluminum prices off nearly 30% and alumina prices down over 40%, that's a pretty impressive showing.

The EBITDA strength in the face of a weak aluminum market is the result of the company's massive restructuring efforts. Essentially, Alcoa has been shutting plants down and cutting back on production in others to align the business with the market environment. If the solid quarter in Upstream is any indication, Alcoa's made a huge amount of progress.

Aluminum's got legs

And while the Value Add business is seen as the company's best operation, the CEO made sure to point out that, "We are also projecting robust aluminum demand growth for this year of 6%, and we [believe] that alumina and aluminum deficits are going to happen in this year." In other words, the downturn in aluminum that's taken a hefty toll on the company's Upstream business could stabilize this year.

That's a far cry from having Upstream turn into a robust growth engine, like aerospace, which is expected to see industry growth of 9% this year. But it suggests that the darkest days may be behind the company as it gets set to break in two.

Alcoa's breakup plan. Source: Alcoa.

How about that divorce?

But, of course, the biggest moving part for Alcoa is really the pending breakup. Here the CEO noted, "We built a separation program office to manage the separation." That's so the operations guys can focus on running the businesses without having to get sidetracked by the corporate action. "We've also announced the executive teams for both of the firms," he added. In other words, everyone knows who's got to do what today and after the split.

It's a complicated process, and it will take time to sort out sticky issues like the supply relationship between the two companies. The process, however, is still moving ahead on plan. And, perhaps less important but no less exciting, investors can expect to hear Value Add's new name some time in the first half of the year.

In summation, there were some things to be worried about in the quarterly numbers. There's no way around that fact, but that's history. The future still appears relatively bright for the Value Add business, and Upstream's business looks like it's starting to stabilize after years of hard work. So not a great quarter from a backward-looking perspective, but a much better one from a forward-looking one.