How to Calculate Your True Balance Transfer Savings -- Fees and All

Getty Images

A friend of mine almost didn't do a balance transfer because of the $300 fee. He was nervous about paying that much up front -- totally fair.

But once he ran the numbers and saw he'd save over $1,400 in interest, the fee suddenly looked like a bargain.

That's the thing about balance transfer cards… The math can be way more favorable than you'd expect.

Even with a 3% or 5% fee, the interest savings are usually way bigger -- especially if you're currently stuck with a 20%+ APR credit card.

Here's how to calculate your true balance transfer savings, including the fee.

First, ballpark your current interest costs

If you're carrying a credit card balance, you're probably losing a lot of money to interest. You might not feel it month to month, but it adds up fast.

To ballpark your current interest, here's a quick formula:

Annual interest = APR × current balance

So if you owe $7,000 on a card with 21% APR, you're looking at around $1,470 per year in interest (assuming you're carrying the full balance month to month).

That's money you're handing to the bank -- without shrinking the balance that you owe.

Next, factor in the balance transfer fee

Most balance transfer cards charge a one-time fee of 3% to 5% of the amount you move over.

If you transfer a $7,000 balance:

- A 3% fee would cost you $210

- A 5% fee would be $350

That fee gets added to your new balance right away when you transfer. So instead of owing $7,000 on your new card, you'll now owe $7,210 (or $7,350).

But remember, you're going from 21% interest to 0% for the balance transfer period. So the fee is small in comparison to the interest you could save.

If you're curious which cards offer the longest 0% intro APR periods (and the lowest fees), it's worth comparing a few side by side. See today's best balance transfer cards and find the right fit for your payoff plan.

Compare the fee vs. interest saved

So far we've used rough math to estimate the interest you'd pay over 12 months, and how much you'd pay in fees for a balance transfer.

Here's what it looks like added up using a $7,000 debt:

- Estimated interest saved in 12 months: ~$1,470

- Balance transfer fee (3%): $210

- Total savings: ~$1,260

Even with a 5% fee ($350), you'd still likely save well over $1,000. Not bad for a quick credit card move.

Keep in mind, this is just rough math based on a 12-month timeline. And it assumes you're carrying the full balance the whole time and not fully paying off your debt.

Your actual savings might be a little lower or higher depending on your specific payoff plan.

Some cards offer 0% intro APR periods of 15, 18, or even 21 months -- which can give you a much bigger runway to pay down your debt completely.

That's where a balance transfer calculator really comes in handy. Just plug in your balance, the APR you're avoiding, your monthly payment, and the transfer fee of the card you're considering.

It'll show you a personalized snapshot of how much interest you could skip, and how fast you could be debt-free.

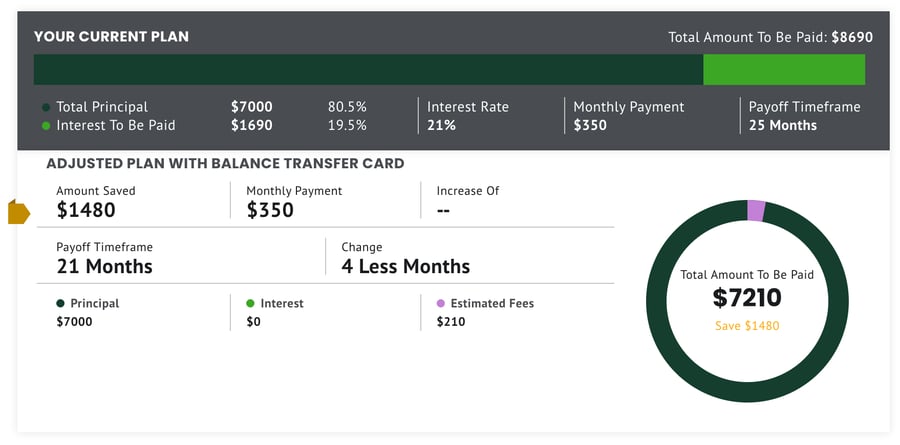

Here's a snapshot of potential savings based on that same $7,000 starting balance, a 0% intro APR period for 21 months, a 3% balance transfer fee, and monthly payments of $350.

Image source: Author input, MFM balance transfer calculator.

Tips to maximize your balance transfer savings

I've helped countless people get out of debt (and stay out!) using balance transfer cards. Here's my advice to get the most out of the 0% intro APR window:

- Pick a long intro APR period. More time means lower payments needed and more flexibility. Here's my top pick balance transfer card with a super long intro APR.

- Pay more than the minimum. This helps knock out the balance before interest returns.

- Don't use the card for new purchases. That can create a mess with payments and new interest charges.

- Set up autopay. Never miss a payment on your new card. Missed payments can cancel your intro APR -- don't risk it.

- Don't transfer more than you can pay off. The goal is to pay off your entire balance within the intro APR period.

If you follow these tips, you can save serious money on interest -- even with a transfer fee.

Balance transfers aren't "free." But they can still be a great deal.

If you're paying 20%+ interest currently, having 12 or more months of 0% intro APR can be a lifesaver. Run the numbers for yourself and see if it's worth using a balance transfer card.

Compare today's top 0% intro APR cards here for both balance transfers and new purchases.

Our Research Expert

Joel O’Leary is a full-time Personal Finance Writer at Motley Fool Money, covering credit cards, bank accounts, investing, mortgages, and other personal finance topics. Joel has been writing about personal finance since 2018, previously leading editorial content for the How To Money podcast and serving as a resident writer at Budgets Are Sexy. He bought his first rental property at age 18, funding the down payment with savings from his high school job at McDonald’s -- a testament to his lifelong passion for smart money decisions. His work aims to make personal finance accessible and actionable for everyday readers. When he’s not writing, Joel enjoys surfing and spending time with his family.