Average American Household Debt in 2026: Facts and Figures

KEY POINTS

- Total Household Debt: As of Q1 2026, total consumer debt is $18.8 trillion, with an average household debt of $105,444.

- Credit Card Balances: The average credit card debt stands at $6,715, with a total debt of $1.252 trillion as of Q1 2026.

- Mortgage Debt Overview: Americans collectively owe $13.191 trillion in mortgage debt, averaging $269,562 per household.

Drawing on data from Experian, the Federal Reserve, TransUnion, and the U.S. Census Bureau, Motley Fool Money breaks down the most common types of debt, including mortgages, auto loans, credit cards, and personal loans.

Key household debt statistics

| Figure | Amount |

|---|---|

| Total household debt, Q1 2026 | $18.794 trillion |

| Average household debt, 2025 | $105,444 |

| Total credit card debt, Q1 2026 | $1.252 trillion |

| Average credit card debt, Q4 2025 | $6,715 |

| Total mortgage debt, Q1 2026 | $13.191 trillion |

| Average mortgage debt, Q4 2025 | $269,562 |

| Median mortgage payment, March 2026 | $2,131 |

| Total home equity revolving debt, Q4 2025 | $446 billion |

| Average HELOC value, 2025 | $49,517 |

| Total auto loan debt, Q1 2026 | $1.685 trillion |

| Average auto loan debt, Q4 2025 | $24,822 |

| Average monthly new car payment, 2025 | $767 |

| Average monthly used car payment, 2025 | $537 |

| Average personal loan debt, Q4 2025 | $11,699 |

| Total student loan debt, Q1 2026 | $1.658 trillion |

| Other debt, Q1 2026 | $0.562 trillion |

Average consumer household debt in 2026: $105,444

| Debt Type | Total, Q4 2025, unless otherwise specified |

|---|---|

| Total consumer debt (including types not listed below) | $18.794 trillion |

| Average household debt, 2025 | $105,444 |

| Total mortgage debt | $13.191 trillion |

| Total revolving home equity debt | $446 billion |

| Total auto loan debt | $1.685 trillion |

| Total credit card debt | $1.252 trillion |

| Total student loan debt | $1.658 trillion |

| Other debt | $0.562 trillion |

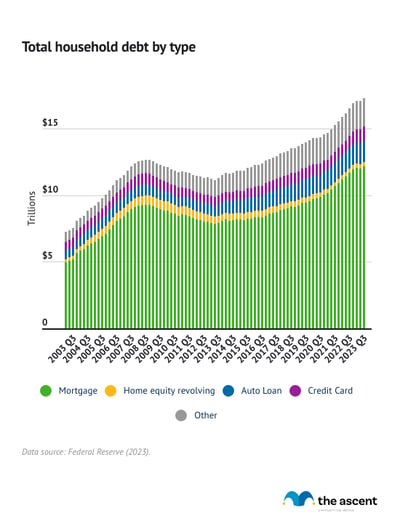

The New York Fed's quarterly Household Debt and Credit Survey (HHDC) shows that total consumer debt stands at $18.8 trillion as of the first quarter of 2026. That's a record high.

How much debt does the average American have?

The average American carries $105,444 in total debt as of September 2025, according to Experian. Excluding mortgage debt, the average balance is $21,603, down 3.3% from the prior year, suggesting consumers are paying down non-housing debt faster than they're adding it.

Credit cards, auto loans, and personal loans account for the bulk of non-mortgage debt.

Average debt by age

Debt balances vary significantly by generation, driven largely by where each cohort is in its financial life cycle, according to Experian data from September 2025.

| Generation | Auto Loan | Credit Card | Mortgage | Non-Mortgage Balance |

|---|---|---|---|---|

| Gen Z (18–28) | $21,027 | $3,553 | $267,157 | $14,987 |

| Millennials (29–44) | $25,471 | $7,068 | $324,272 | $26,304 |

| Gen X (45–60) | $27,956 | $9,684 | $287,928 | $30,069 |

| Baby boomers (61–79) | $22,734 | $6,766 | $197,090 | $18,044 |

| Silent Generation (80+) | $17,276 | $3,400 | $149,458 | $6,663 |

Generation X carries the highest average balance across auto loans, credit cards, and total non-mortgage debt. Gen X credit card balances are at least 24% higher than millennials' and 35% higher than baby boomers', per Experian. Millennials carry the largest average mortgage balance at $324,272, reflecting peak homebuying years at today's elevated home prices.

Average credit card debt: $6,715

| Figure | Amount |

|---|---|

| Total credit card debt, Q1 2026 | $1.252 trillion |

| Average credit card debt, Q4 2025 | $6,715 |

| Delinquency rate of all credit card loans from commercial banks, Q4 2025 | 2.94% |

| Flow into early delinquency, Q1 2026 | 8.61% |

| Flow into serious delinquency, Q1 2026 | 7.10% |

According to the latest Household Debt and Credit survey results from the Fed, Americans owe a record $1.3 trillion in credit card debt.

The average credit card balance was $6,715 as of the fourth quarter of 2025, according to TransUnion. That's up from $6,580 a year prior.

Based on Experian data from the second quarter of 2025, Gen X has the highest average credit card balance, $9,600, while Gen Z has the lowest, $3,493.

Credit card balance by generation

| Generation | 2023 | 2024 | 2025 |

|---|---|---|---|

| Generation Z (18-25) | $3,148 | $3,266 | $3,493 |

| Millennials (26-41) | $6,274 | $6,642 | $6,961 |

| Generation X (42-57) | $8,870 | $9,255 | $9,600 |

| Baby boomers (58-76) | $6,601 | $6,648 | $6,795 |

| Silent generation (77+) | $3,434 | $3,375 | $3,445 |

Credit card delinquency rate: 8.6%

In the first quarter of 2026, 8.61% of credit card balances had become delinquent by 30 days or more over the past year. That's down from 8.69% last quarter and 8.75% a year ago.

Average mortgage debt: $269,562

| Figure | Amount |

|---|---|

| Total mortgage debt, Q1 2026 | $13.191 trillion |

| Average mortgage debt, Q4 2025 | $269,562 |

| Median mortgage payment, March 2026 | $2,131 |

| Average mortgage rate, Q1 2026 (30-year fixed) | 6.11% |

| Total home equity revolving debt, Q4 2025 | $446 billion |

| Average HELOC value, 2025 | $49,517 |

Mortgages make up 70% of American consumer debt. That number has risen consistently since mid-2013 and has recently accelerated as home prices hit record levels. Total mortgage debt stands at $13.2 trillion.

How much mortgage debt does the average American have? The average mortgage debt among Americans is $269,562, per TransUnion. That's up from

$261,631 a year ago.

Average mortgage rate: 6.11%

The average 30-year fixed mortgage rate for the first quarter of 2026 is 6.11%, down from 6.23% in the third quarter.

Mortgage rates rose through 2023 after hitting lows in 2020 and 2021. They started to decline in the second half of 2024.

Median mortgage payment: $2,131

The median mortgage payment in March 2026 was $2,131, according to the Mortgage Brokers Association. The median mortgage payment has fallen slightly in recent months as mortgage rates have decreased.

Average HELOC amount: $49,517

Based on data from Experian, the average value of a home equity line of credit in 2025 was $49,517.

Average auto loan debt: $24,822

| Figure | Amount |

|---|---|

| Total auto loan debt, Q1 2026 | $1.685 trillion |

| Average auto loan debt, Q4 2025 | $24,822 |

| Average monthly new car payment, 2025 | $767 |

| Average monthly used car payment, 2025 | $537 |

Auto loan debt slightly increased to $1.69 trillion in the first quarter of 2026 from $1.67 trillion in the previous quarter.

The average auto loan debt is $24,822 as of the fourth quarter of 2025.

The average car payment for both new and used vehicles has stabilized over the course of the year, with little change in recent quarters, according to Experian data.

Average new car payment: $767

The average monthly payment on a new-car loan was $767 in 2025, according to Experian. Monthly payments on loans for new cars, by credit score, are as follows:

- Deep subprime (300-500): $767

- Subprime (501-600): $792

- Nonprime (601-660): $819

- Prime (661-780): $773

- Super prime (781-850): $748

Average used car payment: $537

The average monthly payment on a loan for a used car was $537 in 2025, according to Experian. Monthly payments on loans for used cars, by credit score, are as follows:

- Deep subprime (300-500): $558

- Subprime (501-600): $557

- Nonprime (601-660): $545

- Prime (661-780): $523

- Super prime (781-850): $535

Auto loans in delinquency: 1.5%

According to TransUnion, 1.5% of auto loans were 60 days or more past due in the fourth quarter of 2025, up from 1.47% a year prior.

Rising vehicle prices and overall inflation through 2022 and the start of 2023 may be responsible for a higher percentage of auto loans being in hardship compared to previous years.

Average personal loan debt: $11,274

| Figure | Amount | Prior Year |

|---|---|---|

| Average personal loan debt, Q4 2025 | $11,699 | $11,607 |

| Average unsecured personal loan balance, Q4 2025 | $8,421 | $8,469 |

| Average finance rate on 24-month personal loans from commercial banks, February 2026 | 11.40% | 11.66% |

| Personal loans in hardship, 60-days plus past due, Q3 2025 | 3.99% | 3.57% |

Personal loans are versatile financial products. They can be used for a variety of financial needs, including weddings, home renovations, vacations, or debt consolidation.

According to TransUnion, the average unsecured personal loan amount in the fourth quarter of 2025 was $8,421, down from $8,469 in the previous year.

The average personal loan debt per consumer is $11,699, indicating that many people with one unsecured personal loan have at least one more or are accruing interest faster than they can pay it off. That's higher than the level recorded a year prior, which was $11,607.

Average personal loan interest rate: 11.4%

In February 2026, the average interest rate for a 24-month personal loan was 11.4%, more than a quarter of a percentage point down from the previous year, according to the Federal Reserve.

Personal loans in delinquency: 3.99%

In the fourth quarter of 2025, 3.99% of unsecured personal loans were delinquent and in hardship, 60 days or more past due. That's up from the same quarter in 2024, when 3.57% of unsecured personal loans were in hardship.

Charge-offs and foreclosures

When Americans can't handle their debts, foreclosures, bankruptcies, delinquencies, and charge-offs occur. When those numbers go up, it's clear that Americans' personal finances are in trouble.

So what happened this year?

Charge-off and delinquency rates on consumer loans in 2025: 2.62%

The Federal Reserve Board collects statistics on charge-offs and delinquencies by loan type. Here's how they've changed since 2010:

Charge-offs and delinquencies for consumer loans decreased in the fourth quarter of 2025 compared to the previous quarter. Charge-offs and delinquencies for credit cards fell slightly.

The delinquency and charge-off rate for consumer loans (which includes credit cards) was 2.62%, while the overall rate, which includes real estate and commercial loans, was 1.48%.

Paying off debt

Total household debt has hit record levels, but the debt payment-to-income ratio at 11.3% remains lower than it was for most of the 2000s. That gap suggests most households are managing their debt loads, even as balances grow.

For those carrying high-interest balances, a balance transfer card can reduce the cost of credit card debt, and a balance transfer calculator can show how much interest a transfer would save. Building a savings buffer in a high-yield savings account reduces reliance on credit when unexpected expenses come up. For those consolidating multiple debts, personal loans with competitive rates can lower the total interest paid and simplify repayment.

-

Sources

- Experian (2026). "Experian Study: Average U.S. Consumer Debt and Statistics."

- Experian (2026). "Experian 2025 Consumer Credit Review."

- Experian (2026). "Experian State of Automotive Finance Market."

- Experian (2024). "State of Retail Cards and Buy Now, Pay Later in 2024."

- Federal Reserve (2026). "Household Debt and Credit."

- Federal Reserve (2026). "30-Year Fixed Rate Mortgage Average in the United States."

- Federal Reserve (2026). "Delinquency Rate on Credit Card Loans, All Commercial Banks."

- Federal Reserve (2026). "Finance Rate on Personal Loans at Commercial Banks, 24 Month Loan."

- Federal Reserve (2026). "Household Debt Service Payments as a Percent of Disposable Personal Income."

- Federal Reserve (2026). "Charge-Off and Delinquency Rates on Loans and Leases at Commercial Banks."

- Mortgage Bankers Association (2026). "Mortgage Application Payments Increased in March."

- TransUnion (2026). "Credit Industry Snapshot."

- TransUnion (2026). "TransUnion 2026 Originations Forecast Shows Continued Positive Momentum Amidst Moderate Expansion."

Our Research Expert

Jack Caporal is the Research Director for The Motley Fool and Motley Fool Money and has worked full-time for the company since 2021. Jack leads efforts to identify and analyze trends shaping investing and personal financial decisions across the United States. His research has appeared in thousands of media outlets including Harvard Business Review, The New York Times, Bloomberg, and CNBC, and has been cited in congressional testimony. He previously covered business and economic trends as a reporter and policy analyst in Washington, D.C. He serves as Chair of the Trade Policy Committee at the World Trade Center in Denver, Colorado. He holds a B.A. degree in International Relations with a concentration in International Economics from Michigan State University.

Motley Fool Stock Disclosures

The Motley Fool has a disclosure policy.