What is the federal funds rate?

We said earlier that the federal funds rate is the overnight interest rate that banks charge when they lend each other money. From a consumer perspective, it impacts the rates lenders offer on things like credit cards, loans, and mortgages. For savers, it affects how much we can earn on savings accounts, money market accounts, and CDs.

You might be wondering why banks and financial institutions have to lend each other money. Banks have to keep a percentage of their deposits in reserve -- it helps to avoid things like bank runs. But the amount of money each bank has fluctuates depending on the day's activities. Banks borrow from one another to make sure they have enough cash on hand to function and meet the reserve requirements.

How the Fed sets interest rates

The Fed sets interest rates through regular meetings of the Federal Open Market Committee (FOMC). It uses a range of indicators to take the pulse of the economy. These include jobs data, the consumer price index, GDP, stock market performance, and more.

The FOMC meets eight times a year -- more if needed -- to evaluate the latest economic data. The 12 board members vote to decide if they need to make any shifts in policy, including any changes to the federal funds rate.

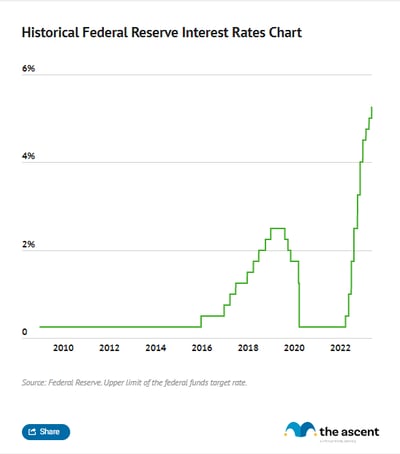

Federal funds target rate

The federal funds target rate is also known as the federal funds rate or Fed interest rate. The word "target" is used because banks decide the interest rate between themselves when they lend and borrow from each other. The Fed can't tell them exactly what rate to use.

If you're wondering what the actual rate gets called, it's the "effective federal funds rate." This is the average overnight rate at which banks lend money to one another. It's usually pretty close to the target rate.

Why the Fed raises interest rates

The Fed raises interest rates when it wants to slow the economy down. It may do this because inflation is too high or because it thinks the economy is overheated.

Why the Federal Reserve lowers interest rates

The Fed lowers interest rates when it wants to stimulate the economy. It may do this because of rising unemployment or to try to avoid a recession.

How are other interest rates impacted by the Fed rate?

As a consumer, we come across many interest rates in our financial lives. The Fed rate impacts all of them to a greater or lesser extent. For example, many lenders use something called the Prime rate as a basis for their APRs. This is the rate that lenders give to their most creditworthy customers, and it's usually about 3% higher than the federal funds rate.

Credit card interest rates

Credit card APRs are loosely based on the Prime rate, so they will drop slightly if the Fed rate falls. However, the Fed is cutting rates at a fraction of a percent at a time. As such, Fed rate cuts won't make a lot of difference to your monthly payments.

The average credit card APR was 23.37% in October, per the Fed. You may get better rates on the best credit cards, but interest payments can still add up. Let's say you carry a balance of $6,000:

- If your APR is 24%, you'd owe almost $120 in monthly interest.

- If your APR is 22%, you'd owe almost $110 in monthly interest.

Not only that, the Fed rate is only one factor that goes into calculating how much credit card interest you'll pay. According to Consumer Reports, the gap between the Prime rate and average credit card APRs has increased steadily for the past decade.

Savings account interest rates

Banks use the federal funds rate as a guide when setting savings accounts interest rates. As rates fall, so will savings APYs. And, unlike CDs, which lock in a rate for the length of the CD, savings account rates are variable. That means the rate can change at any time.

To maximize the interest you earn on your savings, pick a top high-yield savings account. The rates on these -- often online-only -- accounts are significantly higher than the average. If you want to earn inflation-beating returns, shop around for accounts with high APYs, low fees, and achievable minimum deposit requirements.

Mortgage loan interest rates

The federal funds rate is one of many factors that influence mortgage rates. Rates are also impacted by inflation, the housing market, economic expectations, the bond market -- specifically the 10-year Treasury yield -- and more.

The majority of home buyers opt for 30-year fixed-rate loans. The 10-year Treasury yield is the rate the U.S. government pays on what are essentially decade-long loans. These Treasuries hold more sway over mortgage APRs than the very short-term federal funds rate.

Auto loan interest rates

The Federal Reserve rate influences auto loan APRs, but it's only part of the story and it can take time for rate cuts to filter down. Cox Automotive says, "The Fed does not directly control the rates consumers see, and auto loan rates may end up being the slowest to move."

Like mortgages, these are longer-term loans. Auto lenders have to factor in other considerations, including the delinquency rates on existing loans. To qualify for the best auto loan rate, take steps to improve your credit score and try to make a down payment of at least 20%.

Personal loan interest rates

The federal funds rate influences personal loan rates, but it's not the be-all and end-all. Lenders also take broader factors into account like inflation, loan delinquencies, Treasury yields, and more. Your situation will play a big part too -- you can get a lower rate if lenders are confident you will repay the loan.

Personal loan rates are likely to fall as the Fed cuts its rates. This will only impact new loans or adjustable-rate loans. If you have a fixed-rate personal loan, Federal Reserve rate cuts will not impact your APR unless you refinance.

If you're applying for a personal loan, you can take steps to lower your rate. Work to improve your credit score, pay down existing debt, and shop around to find the best personal loan.