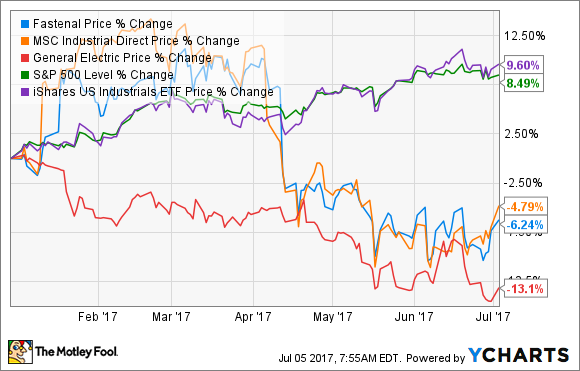

It's always useful to look for stocks that have underperformed the market and their sector because it can illuminate some great investing ideas. In this regard, General Electric Company (GE -1.19%), MSC Industrial Direct Co (MSM -0.80%) and Fastenal Company (FAST +2.05%) are all stocks investors should be taking a closer look at, and here's why.

General Electric Company

With a market cap of nearly $240 billion, GE's size dictates that its stock performance is a large determinant of how the industrial sector performs in general -- a fact that makes its significant under-performance even more notable. So, what's gone wrong with GE's stock in 2017? As ever, it's a matter of conjecture, but it's clear that analysts don't think the company will hit its earnings targets.

Moreover, the company missed revenue targets in 2016 and disappointed with weak free cash flow in the first quarter, while questions have been asked about its core power segment and oil & gas operations. It's not been a happy time for GE investors.

However, what matters now is the investment proposition going forward, and despite disappointing the investment community in recent times, GE's underlying growth prospects still look good. A combination of cost cuts -- structural and unit cost production reductions -- earnings-enhancing deals with Baker Hughes and Alstom, digital initiatives, and the potential for significant restructuring when new CEO John Flannery completes his review are all potentially positive catalysts for GE.

Meanwhile, the stock's valuation stands at a discount to its peers.

GE PE Ratio (Forward) data by YCharts.

MSC Industrial Direct Co and Fastenal end markets improving

One of the reasons the industrial sector has done well in 2017 is the return to growth of U.S. industrial production. That's good news for U.S. manufacturing, and it's good news for industrial supply companies like MSC Industrial and Fastenal.

Indeed, both companies have reported a significant uptick in end market conditions. Readers already know that Fastenal's first quarter saw the company reporting mid single-digit growth in daily sales growth in both of its end markets (manufacturing and non-residential construction) for the first time since the spring of 2015.

Meanwhile, the following chart of average daily sales growth at MSC Industrial demonstrates the improvement in end markets.

Data source: MSC Industrial Direct Co. presentations.

Pricing and margin remain challenging

The improvement in sales is one thing, but unfortunately, it hasn't been accompanied by a significant improvement in both companies' pricing power, and consequently, margin growth has been challenged. This is somewhat disappointing since during many cyclical recoveries, companies see revenue and margin expanding leading to a significant pick-up in earnings. Both companies have generated less-than-stellar performance on margin.

FAST Gross Profit Margin (Quarterly) data by YCharts.

Essentially, the recovery hasn't been strong enough to allow any of the industrial supply companies to have any pricing power as yet.

For example, here is MSC Industrial Erik Gershwind on the earnings call: "To be clear, even if things pick up, competition remains fierce, and the pricing environment remains challenging." The company did implement a small price increase in February, but according to Gershwind, "it is not material to our overall results, nor do we expect it to be so for our fiscal third quarter." For the record, MSC's gross margin in the second quarter was 44.7%, a decline of 40 basis points (where 100 basis points is 1%) compared to the same period last year.

Image source: Getty Images.

By coincidence, Fastenal's gross margin was also down 40 basis points to 49.4% in its first quarter. Around 30 basis points of the decline was due to an unfavorable customer and sales mix. Relatively more sales to large customers dilute margin -- MSC Industrial tends to see a similar dynamic -- and relatively more non-fastener sales. As CEO Dan Florness pointed out in the earnings call when talking about gross margin, "fastener product line runs in the 50s, our non-fastener products as a group run in the 40s."

While some of Fastenal's gross margin issues are structural -- the company is deliberately growing national accounts and non-fastener sales -- it's still not in a position to increase pricing. Here is CFO Holden Lewis on the earnings call: "Pricing was not a meaningful factor in the quarter. Price is something that we just continue to review at this point."

However, if the recovery continues -- as you can see below, leading industrial indicators indicate ongoing strength -- then it's reasonable to expect that Fastenal and MSC Industrial will be able to increase pricing in due course, which could be good news for stock holders.

US Industrial Production Index data by YCharts.

Looking ahead

The aim of GE's new CEO will surely be to regain investor confidence, and he has a good opportunity to do this as GE has solid underlying growth prospects. Meanwhile, Fastenal and MSC Industrial are likely to see a better pricing environment in the future provided the industrial recovery continues.